If monetary tightening remains the main risk for global stock markets, the threat of a trade war continues to dominate the headlines.

The Donald’s Dealmaking

The question raised by Donald Trump’s trade agenda with China remains, in essence, extremely simple. It is whether The Donald is engaged in a typical ‘Art of the Deal’ negotiation, where he can suddenly turn on a dime and declare a ‘win’, or whether he is really seriously trying to stop China upgrading its economy by targeting ‘Made in China 2025’.

Such a stance would amount to an act of economic warfare. On this point, it should be understood that some of those in Washington pushing this policy view of China as some kind of strategic rival for global leadership. For such people this is about far more than just tariffs.

The markets had been assuming that the American president would not take this too far. But, as discussed here before, concerns have grown as it has increasingly looked like Trump is supporting Robert Lighthizer’s (US Trade Representative) and Peter Navarro’s (White House Economic Adviser) agenda.

How Likely is Economic Warfare?

On July 6, first the US and then Chinese 25% tariffs on US$34 billion worth of goods are due to go into effect. If bilateral negotiations do not resume before that date, then the chances of the US and China entering a so-called trade war grow significantly.

If the above is the state of play, market action has now become critical. The more that the US stock market freaks out about these policies in terms of declining share prices, the more likely becomes The Donald to perform a U-turn. This is because Trump is a market-focused guy even if it is also the case that much of his electoral base are not invested in stocks because they do not have the requisite savings.

There has already been more than a hint of this market dynamic at work last week when the S&P500 recovered some of its losses ‘intraday’ on Monday after Navarro was presumably ordered to issue a less combative statement. His comments came after news reports over the weekend that the US could block companies with at least 25% Chinese ownership from buying companies involved in so-called “industrially significant technology”.

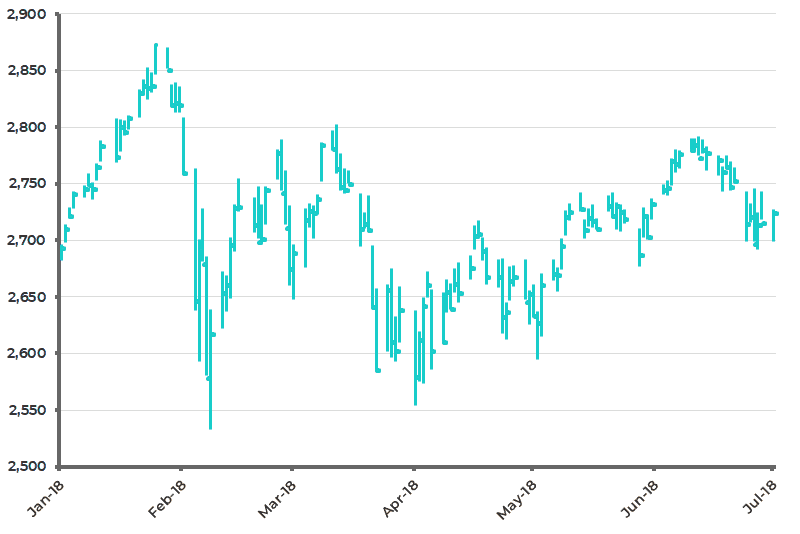

S&P500

Similarly, on Wednesday last week, the S&P500 reversed a pre-market opening decline when Trump made some more conciliatory comments on the nature of the coming investment restrictions. Trump said he will now use a strengthened existing agency and national security review process to scrutinize Chinese acquisitions of American technologies. He said: “Congress has made significant progress toward passing legislation that will modernize our tools for protecting the nation’s critical technologies from harmful foreign acquisitions”.

Meanwhile, if the American president does remain committed to the combative agenda as regards China, Congressional review could prove more destructive of the bilateral relationship over the longer term than tariff hikes. It is also the case that Congress involvement will be via the so-called Committee on Foreign Investment in the United States (CFIUS) whose authority will be enhanced, as Trump referred to above, by new legislation in Congress called the Foreign Investment Risk Review Modernization Act (FIRRMA).

The Congressional involvement will probably make the process harder to unwind once the restrictions are imposed. It is certainly the case that Congress has its own share of enthusiastic China bashers, as is clear from those in Congress who have been seeking to reverse Trump’s decision to overturn the ban on ZTE buying American goods. The US Senate voted last week by 85-10 to reinstate the ZTE sales ban.

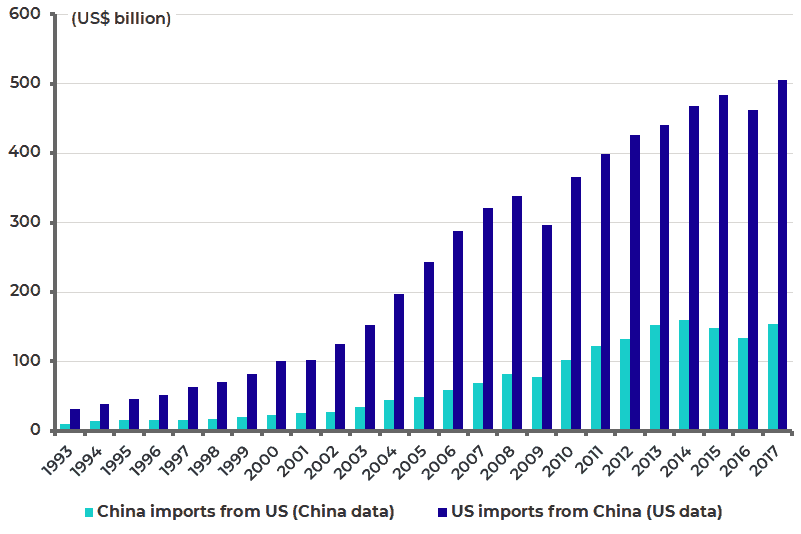

US Imports from China and China Imports from the US

Now it is true, technically, that the pending investment restrictions will not just be aimed at China. The Treasury Secretary has stated that the restrictions will apply “to all countries that are trying to steal our technology”. But the political reality is that all this activity in Washington has a China focus. So, the danger is that once these sorts of actions are announced, they will turn out to have a life of their own.

Events in North Korea are Pleasing to China

Meanwhile, amidst all this focus on deteriorating Sino-US relations, there is one potential positive that should not be completely ignored. That is that events are unfolding in the Korean peninsula in a manner which should please China and a lot of this, intentionally or not, seems to be due to the American president.

China would certainly welcome a North Korean economy that is pursuing a more China-style reform-oriented course in terms of the management of its economy, though the first priority may not be Trump-style beachfront condos. Second, Beijing will also want to maintain North Korea as an independent state, and Trump does not appear to be pushing for unification. Third, China will welcome Trump’s proposal, made at the Singapore summit on June 12, to end American “war games” on the Korean peninsula.

The hope from the above must be that there has been some constructive ‘behind the scenes’ dialogue between Washington and Beijing on North Korea which would infer that the relationship is not as antagonistic as current headlines on the trade issue would suggest.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.