Video game publisher Electronic Arts (NASDAQ:EA) announced earnings that handily beat expectations.

Revenue came in at $1.59 billion, an 18% miss to consensus of $1.95 billion but earnings per share of $1.18 beat the consensus estimate of $0.92 by a full 28% and was up 36% from the same quarter in 2018.

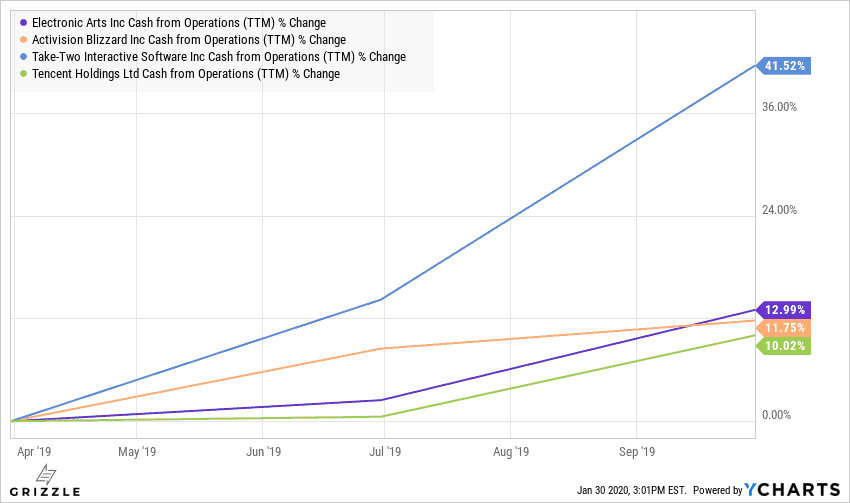

Cashflow from operations was $1.1 billion in the quarter and set a record for the last 12 months hitting $1.9 billion.

Results were driven by a strong showing from the live services and game downloads segments.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]With the next generation of both Microsoft’s and Sony’s consoles slated to hit in 2020, gaming stocks are being bid up in anticipation. EA should perform well through 2020 as we see a spike in-game sales with the new console generation. [/su_panel]EA Stock Underperforming Last 3 Years but Second Best in 2019

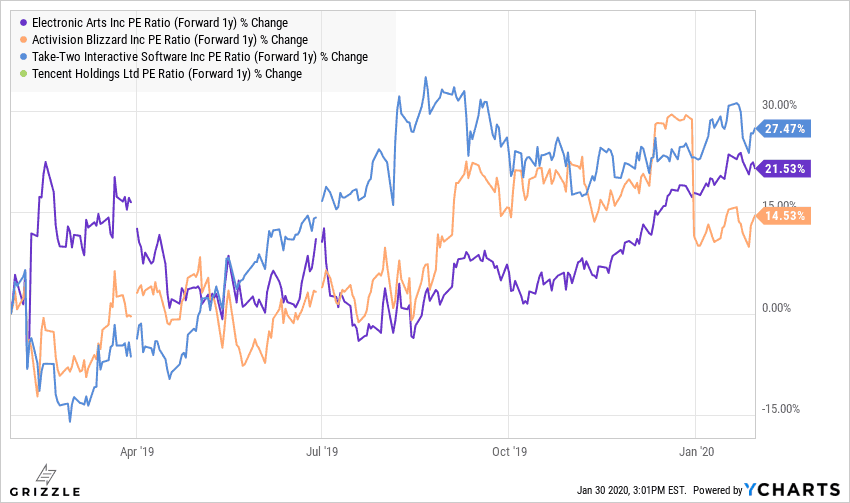

Forward multiples of EA and the other publishers are up 14%-30% in the last year due to investor excitement about the next generation of consoles.

P/E ratios are still lower than they were a few years ago, however, so EA and others are not particularly expensive.

P/E Ratio on the Rise for EA and Others

EA grew EBITDA 13% over the last year, but that was nothing next to Take-Two who grew EBITDA by a whopping 40%.

With new consoles on the horizon EA along with other publishers should see an uptick in game sales and EBITDA.

Increase in EBITDA

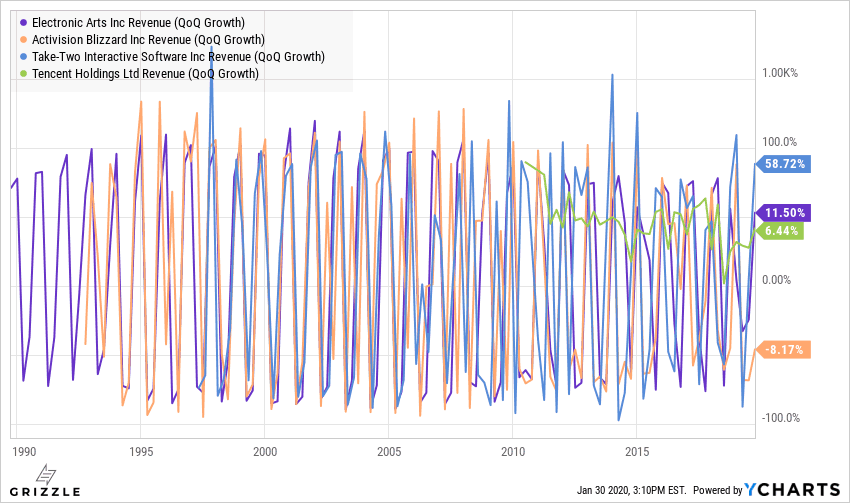

Publishers are transitioning away from their reliance on individual games to drive revenue and focusing on continuous monetization through “always on” online-driven games.

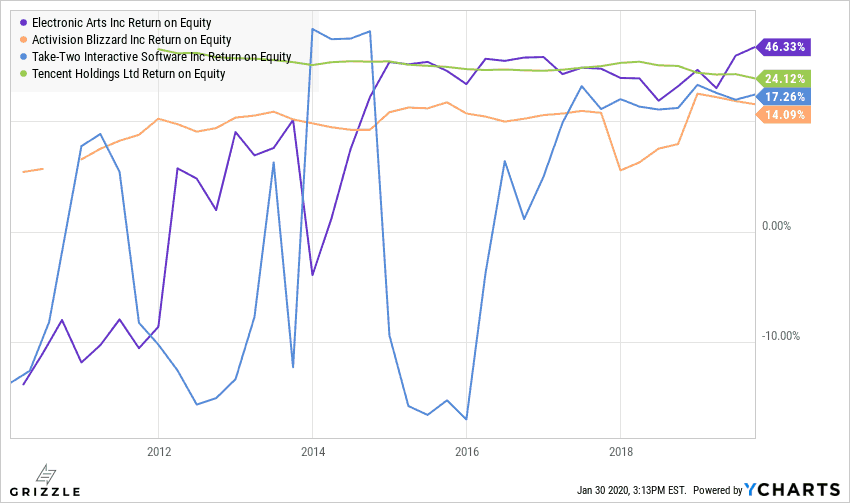

This trend is smoothing revenue volatility and making it easier for management to allocate capital and has increased the return on equity of the game publishing businesses.

Revenue Volatility is Decreasing with the Growth in Online Games

ROE (Return on Equity) of Gaming Business Going Up Thanks to Online Gaming

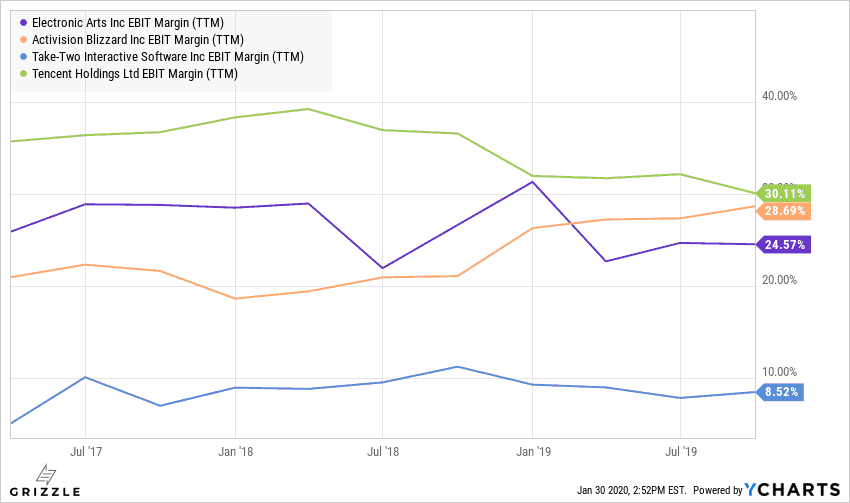

EA has the third-best margin profile after Tencent and Activision Blizzard.

EA’s margins have declined slightly in the last three years vs Activision who has actually grown margins and Take Two whose margins are flat.

EA Margins

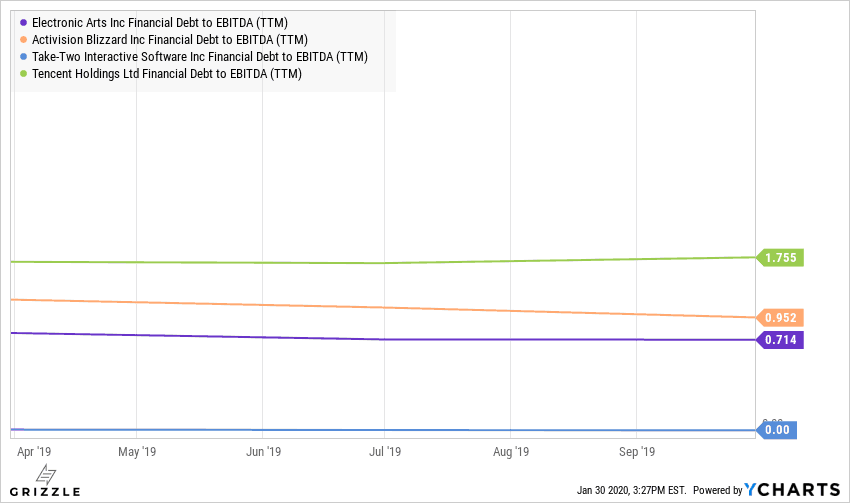

Debt levels for all the gaming companies are very conservative which makes sense given the industry’s earnings volatility.

Investors in EA will not have to worry about any upcoming liquidity concerns.

Debt to Cashflow Among the Lowest in the Group

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.