Etsy Inc. (NASDAQ: ETSY) posted their earnings report for Q4 2019. Revenue was $269.99 million which beat analysts’ expectations of $264.92 million and EBITDA of $54.62 million beat analysts’ estimates of $52.28 million.

The stock has been through a volatile year, and is trading over 30% lower now than it was a year ago. Much of Etsy’s problems can be described as a decline in EBITDA margin which the company announced last quarter that they were going to cut the guidance for EBIDTA margin to a range of 22% to 23% from a prior view of 22% to 24%. This guidance cut caused the stock to plunge 5% despite the company having beat earnings estimates.

But First, the Etsy Story

Etsy is an ecommerce platform that allows individuals or small businesses to sell their handcrafted or homemade goods. Unlike other sites like eBay, Etsy attempts to differentiate itself by being known as having higher quality products, or products that are unique rather than mass produced. Etsy also has a vintage section of products on their website which stipulates that the product must be at least 20 years old to be listed as “vintage”.

Etsy seeks to replicate the experience of going to a market fair sale rather than shopping in a department store. Etsy charges the seller a small fee for listing their product and also takes a small cut of the sale price once the product is sold.

Etsy has attracted a niche group of buyers and sellers. The sticker prices of items on Etsy tend to be higher since they are often artisan or handcrafted items, and the buyers who purchase them tend to emphasize quality or design aesthetics rather than getting the cheapest price possible. In other words, Etsy is the one-stop shop for hipsters.

Etsy Compared

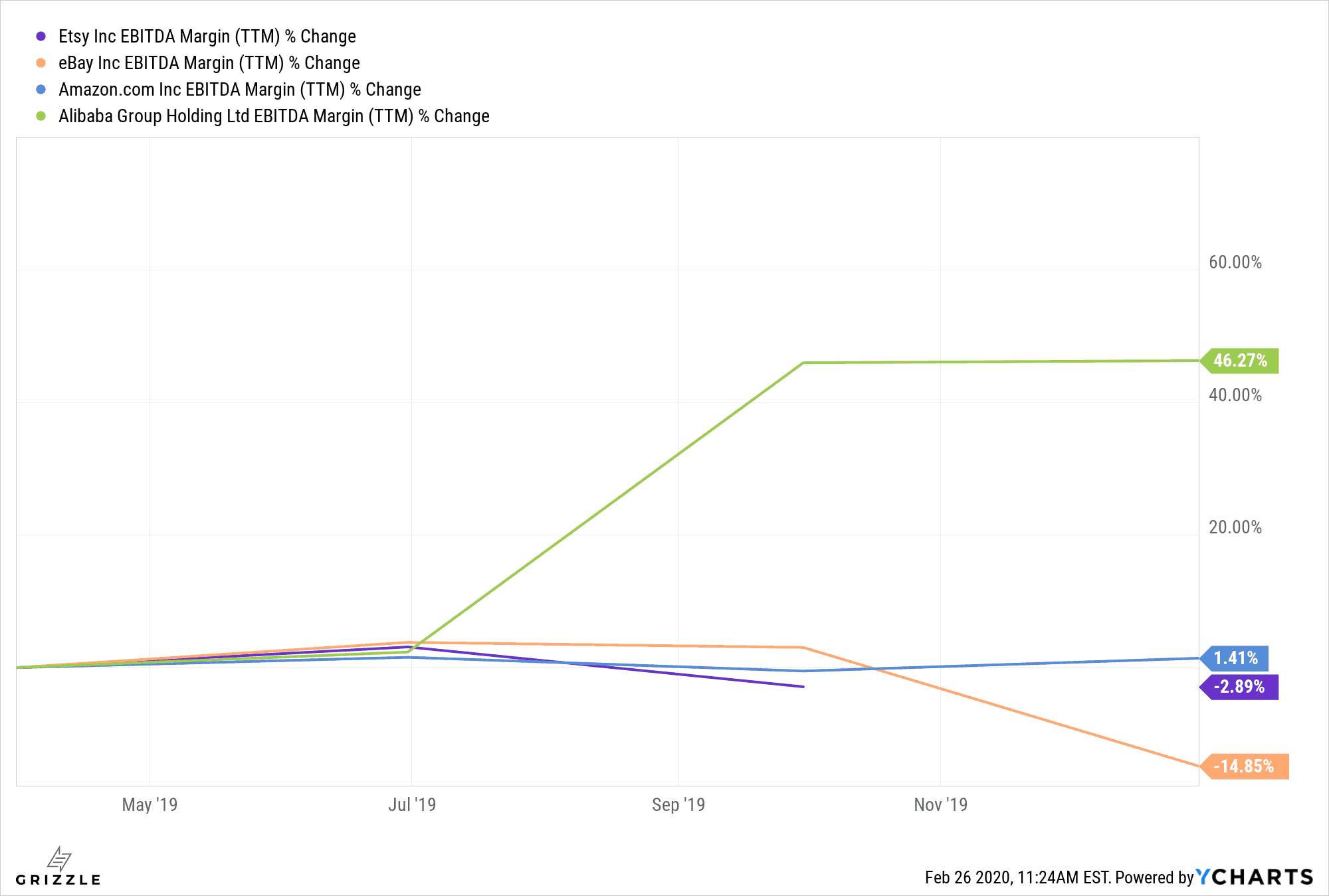

Etsy’s EBITDA margin has been downtrending recently, which is concerning. This puts Etsy behind other ecommerce giants like Amazon and Alibaba, both of whom have posted a positive change in EBITDA margin.

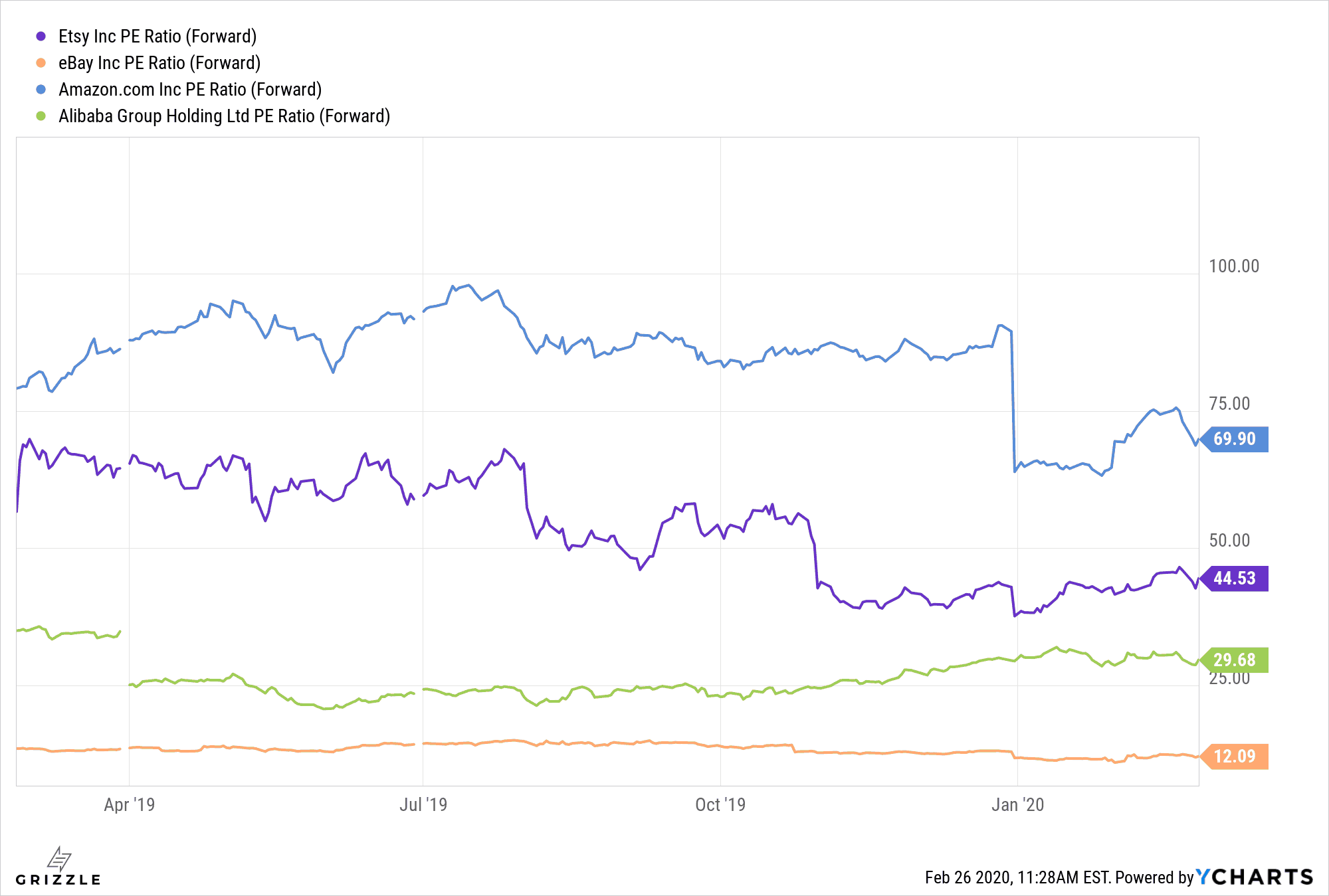

Taking a look at valuations, we see that Etsy’s forward P/E is still rather high, currently at over 40. This puts them ahead of Alibaba’s forward P/E which tells us that Wall Street still puts Etsy in high regard and has high expectations for it in the future.

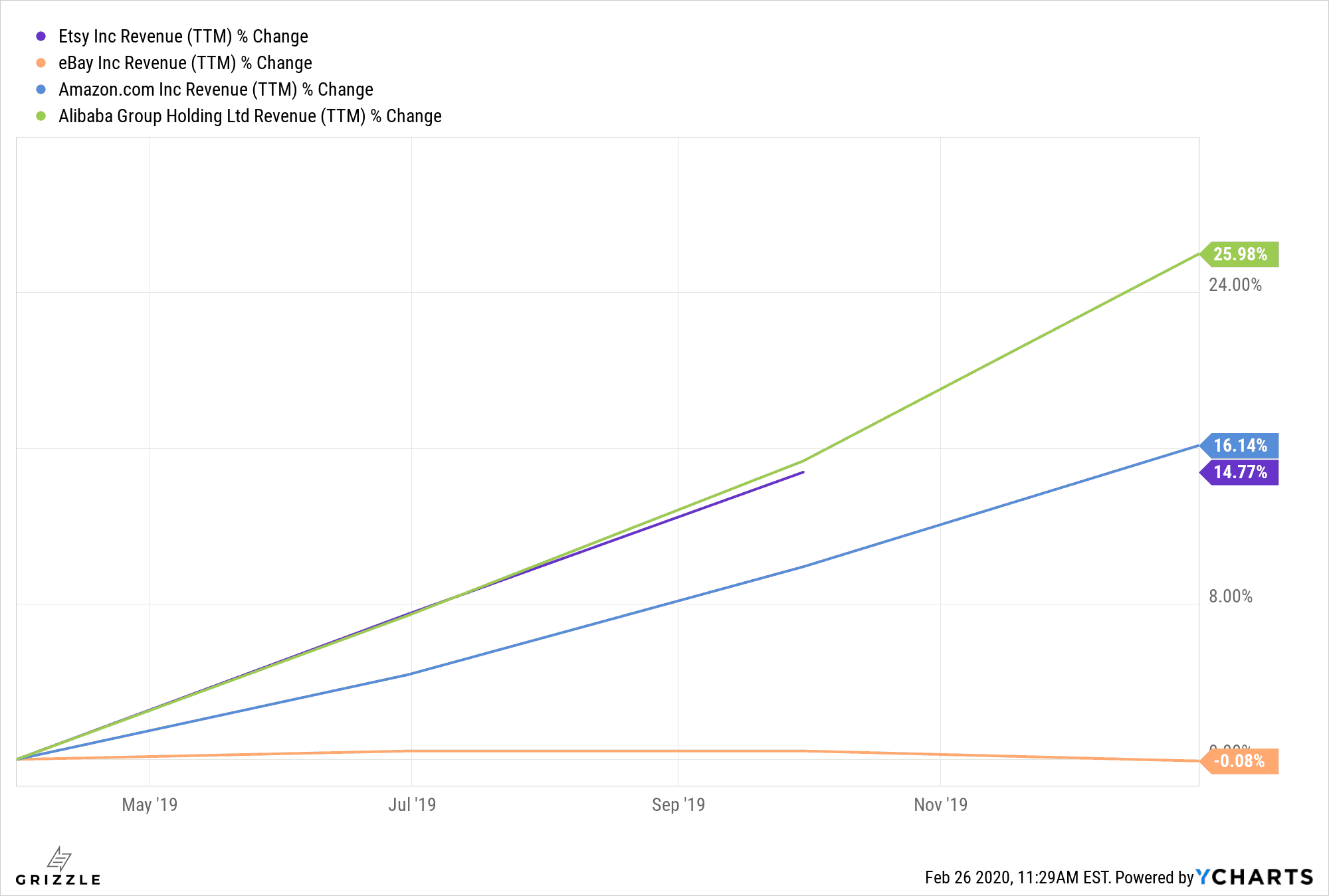

Looking at revenue growth it is easy to see why Etsy is trading at such a rich valuation. For the past 12 months Etsy has grown their revenues almost as much as Amazon percentage-wise. Compare this to eBay which has posted pretty much no growth during the same time period.

Still, the valuation on Etsy seems a bit high considering that Alibaba is beating them on both EBITDA margin and revenue growth and trades at a lower valuation. So Alibaba seems like a better bet on the surface.

However, investing in Chinese companies comes with its own set of risks and Alibaba’s business will no doubt be affected by the current outbreak of the COVID-19 coronavirus. For investors who want to avoid potentially dealing with politics and trade disputes and other macroeconomic factors surrounding Chinese companies, Etsy seems like a decent buy all things considered (although at these levels it’s certainly not the best deal on the stock market). It remains to be seen whether management can continue to grow the business in the future.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.