There is growing potential for market focus to switch back to the Eurozone in coming weeks. This writer’s base case, namely that the Eurozone is on course for de facto fiscal union funded by Northern European taxpayers, remains intact following an historic meeting of the ECB in July.

The reason this meeting was historic was that it marked the commencement of an ever more direct involvement of the ECB into domestic politics and the fiscal policy of individual economies.

This is because of the unveiling of the awkwardly named Transmission Protection Instrument (TPI), the ECB’s much-anticipated anti-fragmentation tool.

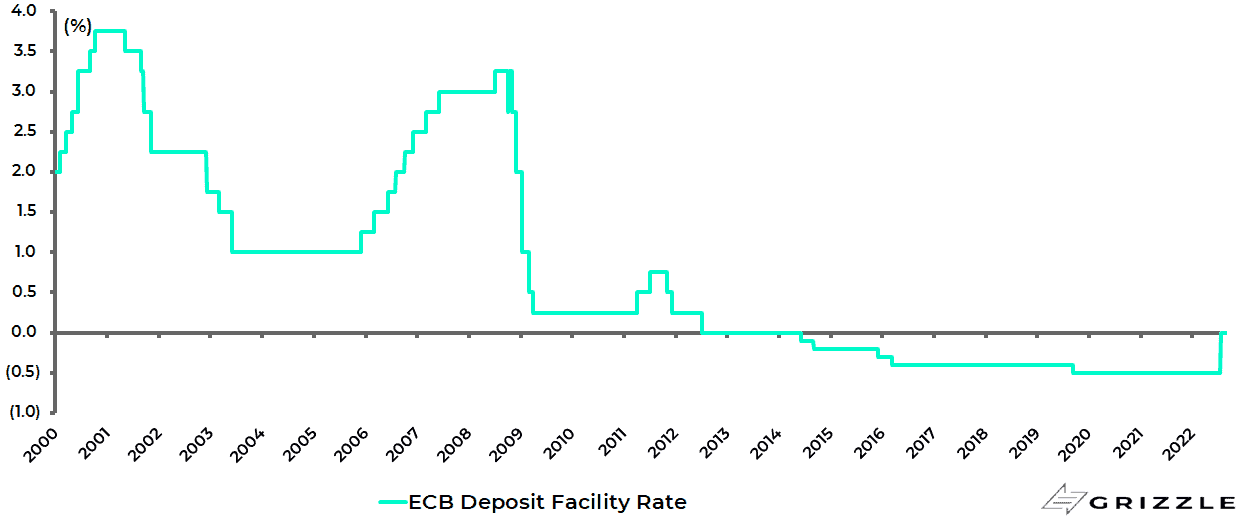

The TPI, perhaps better known as the “To Protect Italy” vehicle, is the latest instrument for ECB bond buying even though it was announced at the same time as the ECB ended negative rates for the first time in eight years with a 50bp rate hike to 0% on the deposit facility rate, and also abandoned the always questionable practice of “forward guidance”.

ECB deposit facility rate

Maintaining the Euro and Integrity of Monetary Policy is an Impossible Task For the ECB

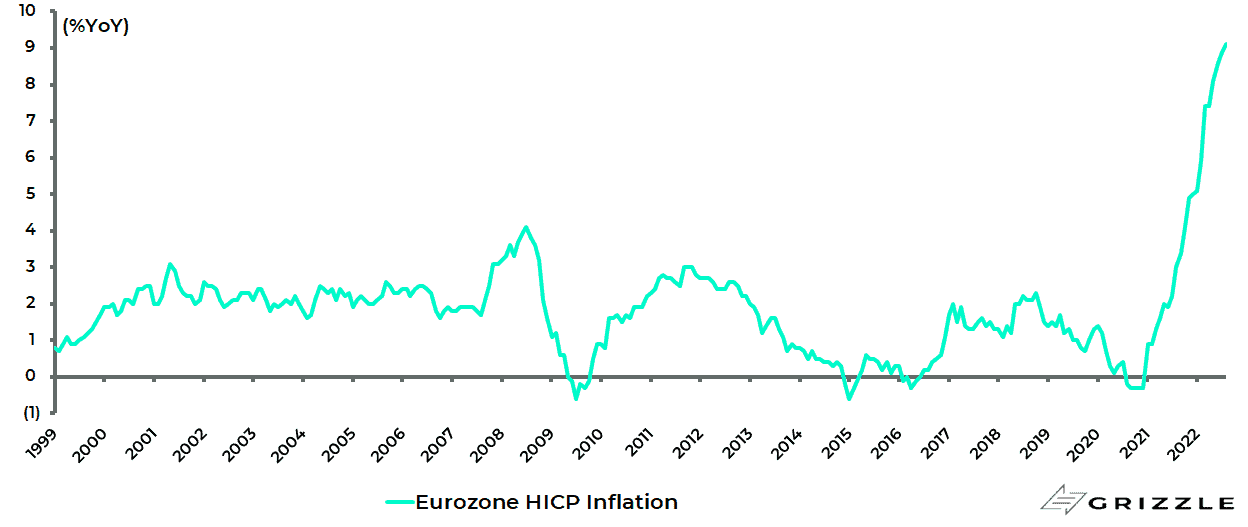

Eurozone inflation

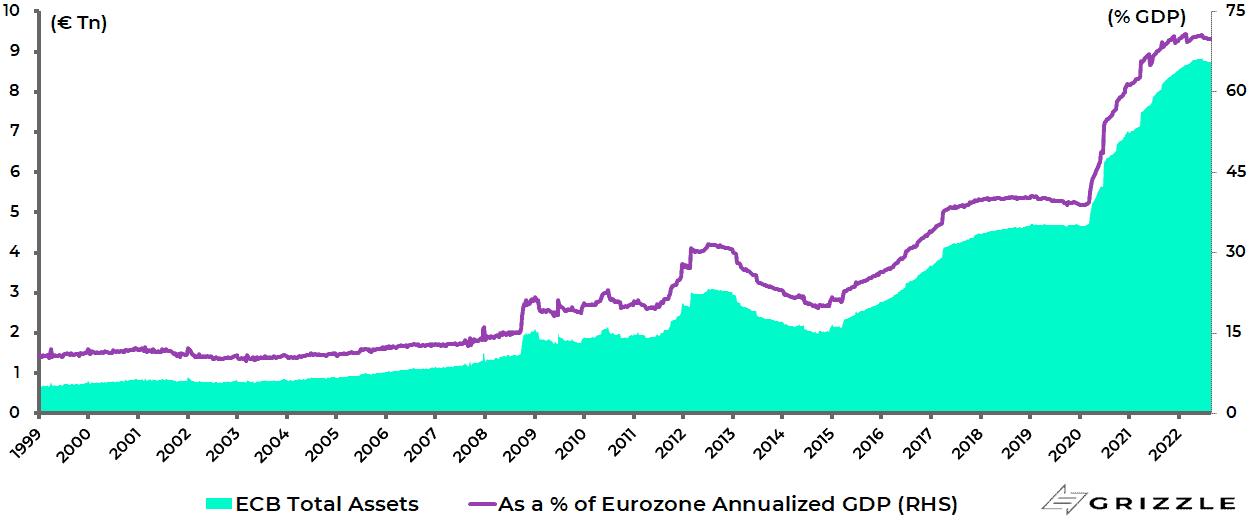

It is also symbolic that the ECB meeting occurred almost exactly ten years after Mario Draghi had his “whatever it takes” moment on 26 July 2012 since when the ECB balance sheet has grown from €3.1tn to €8.8tn as a result of aggressive quanto easing-driven bond buying.

ECB balance sheet

Draghi’s dramatically successful bluff a decade ago bought the ECB some time since the central bank’s bond buying did not start in earnest until October 2014.

But ECB President Christine Lagarde lacks entirely the Italian’s manipulative skills when it comes to talking to financial markets.

She is also much less comfortable with the technical details than the financially sophisticated Draghi, who once worked as an investment banker.

This is why it is only a matter of time before the TPI is tested by the markets.

The politically significant aspect of the TPI is that the bond-buying can be launched by the ECB itself and does not require the approval of EU finance ministers, as has been the case with the ECB’s previous bond-buying programmes, be it the Outright Monetary Transactions (OMT), the Asset Purchase Programme (APP) or the Covid-triggered Pandemic Emergency Purchase Programme (PEPP).

The “bazooka” aspect of the TPI is that it allows the ECB to buy government bonds in unlimited quantities “to counter unwarranted, disorderly market dynamics” in Eurozone member countries.

Technically, the eligibility of the TPI is subject to four general criteria, of which one is an absence of severe macroeconomic imbalances and a second is compliance with fiscal rules.

Still, such criteria will in practice be smokescreens and the real trigger for activation of the TPI will be periphery bond spread widening.

As a result, this is a re-run of the closet yield curve control policy the ECB has already been implementing during the pandemic when its balance sheet soared by €4.1tn or 87% to €8.8tn.

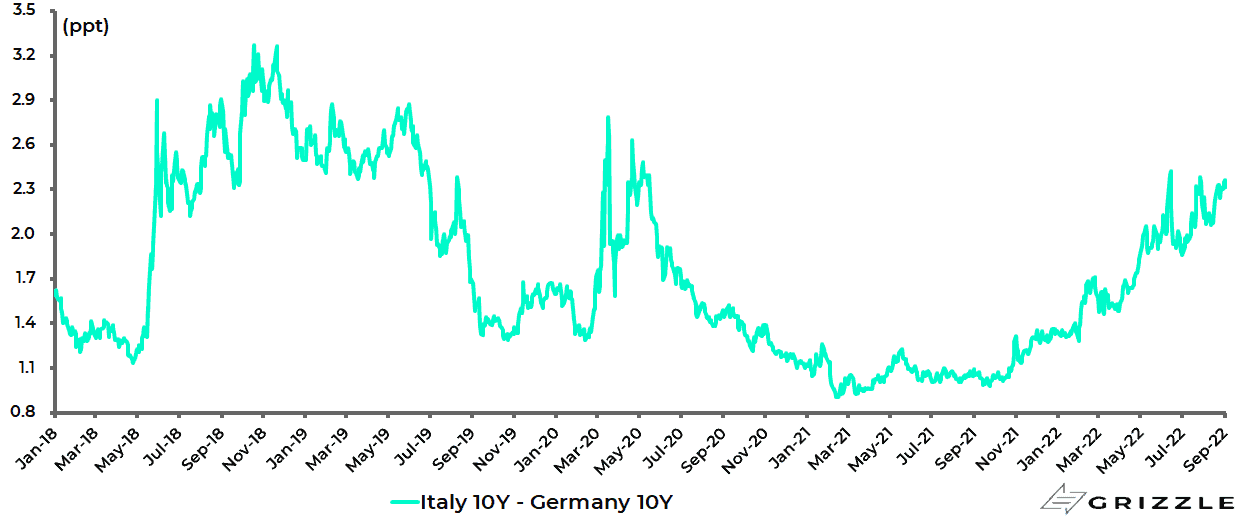

That is not so far away since the current spread is 232bp.

Spread between Italian and German 10-year government bond yields

Source: Bloomberg

Is Italy the Poster Child for “Backdoor Fiscal Integration”?

The July ECB meeting was also scarred the same day by the unexpected, and from an ECB and Brussels’ standpoint, extremely unfortunate resignation of the 75-year-old Draghi as Italian prime minister after 17 months in office.

The trigger was three parties from his ruling coalition, Lega, Forza Italia and Five Star Movement (M5S), not supporting his confidence vote in the parliament.

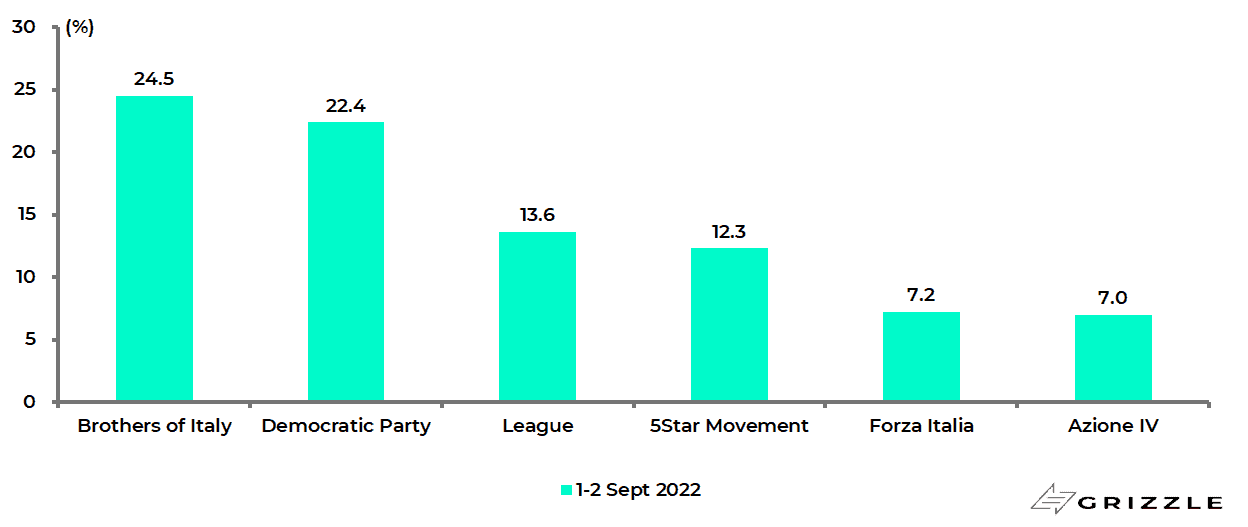

The result is that Italian politics is now back in play with an election due to be held on 25 September and with the right-wing party Brothers of Italy leading the polls with 24.5% support compared with 22.4% for the Democratic Party (PD) and 13.6% for Lega.

Opinion polls for the 2022 Italian general election

This party is not a fan of Brussels.

The reason it is leading in the polls is that, unlike the League or Silvio Berlusconi’s Forza Italia, two other parties on the political right, Brothers of Italy stayed out of the Draghi coalition government.

Its leader Giorgia Meloni is somewhat controversial because of her far-right past.

There is an additional complication.

Italy is due to be paid €19bn by the end of this year, subject to certain conditions being met, as part of payments it is due to receive from the so-called Next Generation EU Fund.

Rome has so far received €46bn from the fund with a request for another tranche of €21bn already submitted in late June.

This is in addition to the abovementioned €19bn.

In a government led by Draghi the assumption was that these funds would be wisely spent in line with the plan submitted by the Draghi government and approved by Brussels in July 2021.

There may be much less confidence about such an outcome now in terms of whatever Italian government emerges out of the September election.

It is also the case that the practicalities of forming a new government make it much harder to meet the timetable for the conditions to be in place for the next €19bn payment while, it should be noted, that €19bn is equivalent to 1% of Italian GDP.

Whatever the stresses triggered by Italian politics, and whatever the noises about the need for “conditionality” coming recently from the likes of the current Bundesbank president Joachim Nagel, the final outcome is likely to be increased ECB buying of periphery bonds sooner or later.

In this respect, this writer came across recently an interview by the Berliner Zeitung with former Bundesbank president Jens Weidmann published at the end of April 2021 (see Berliner Zeitung article: “Bundesbanker Weidmann remains critical of the ECB’s direction”, 30 April 2021).

In that interview, when discussing the so-called joint debt issuance as envisaged in the Next Generation EU reconstruction fund which was being discussed at the time, Weidmann stated that “A fiscal union must not be allowed to be introduced through the back door.”

But that is precisely what appears to be happening.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.