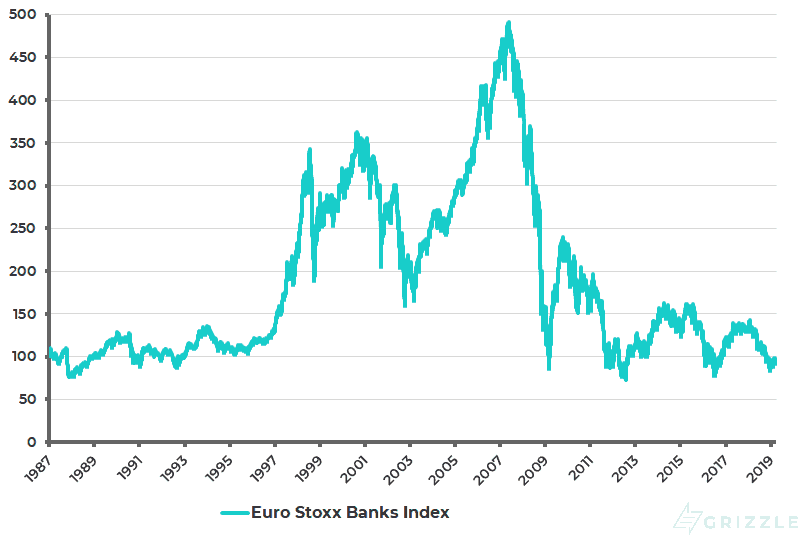

It is easy for investors to dismiss the Eurozone as a sideshow because of its anemic growth and complicated politics. But it still has the potential to be the catalyst of a global financial crisis, triggered by its dysfunctional banks. Eurozone bank stocks have declined by 81% in the past 12 years since peaking in May 2007 (see following chart).

Euro Stoxx Banks Index

Certainly, renewed focus on Europe has now become timely. And I am not talking about Brexit. Following the “Powell pivot”, G7 central banks’ further retreat from a normalization agenda was marked by the ECB’s announcement on March 7 that it was effectively commencing renewed easing.

The only surprise in the announcement is that it came a month earlier than expected. This was driven by the ECB’s realization that it made sense to move before political noise comes back into the Eurozone with the commencement of the European parliamentary election campaign, which has now effectively kicked off with the election due to be held in the 28 countries between May 23-26.

This campaign is likely to generate much more media coverage than normal because of a likely alliance of populist parties on the right campaigning against the fiscal constraints of the Maastricht Treaty and, of course, the free movement of people.

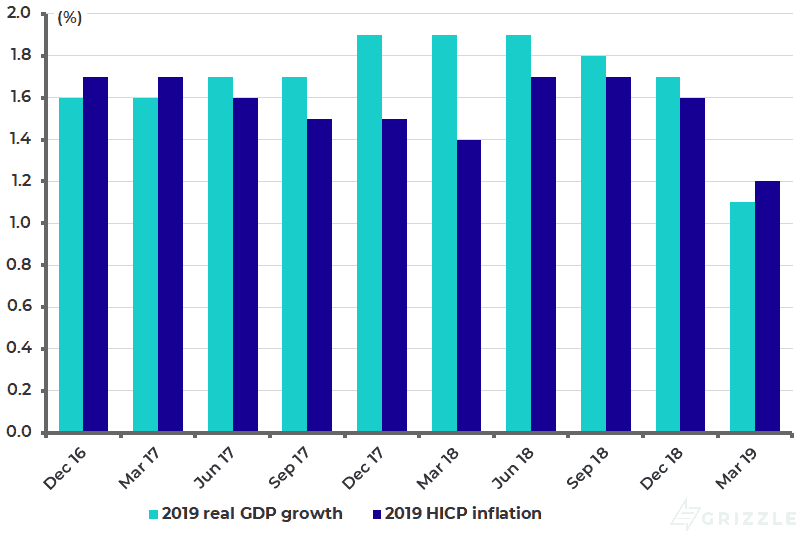

In terms of the actual details of the ECB announcement, the stated rationale for the move was a downgrading in the ECB’s growth and inflation forecast. The forecast for real GDP growth in the Eurozone this year has been cut from 1.7% in December to 1.1% while the inflation forecast was downgraded from 1.6% to 1.2% (see following chart).

The ECB will now hold interest rates at the current level of a negative 40bp on the deposit facility rate at least through to the end of 2019, and doubtless much longer, while the size of the ECB balance sheet will remain at the current €4.7 trillion as maturing bonds will continue to be reinvested.

ECB forecasts for Eurozone real GDP growth and inflation in 2019

TLTROs Are Back for a Third Round

But the most important measure, in terms of amounting to an effective new easing, was the announcement of the ECB’s third round of its Targeted Longer-Term Refinancing Operations, otherwise known as TLTROs. This offers cheap two-year loans to banks linked to lending to businesses and households.

The central aim of the TLTROs has been to help out the problem areas of Eurozone banking, in particular Italian banks, while maintaining the official line that monetary policy in the Eurozone was not being conducted around the needs of any one specific country. This has been a particularly sensitive issue politically since the ECB president, Mario Draghi, is an Italian.

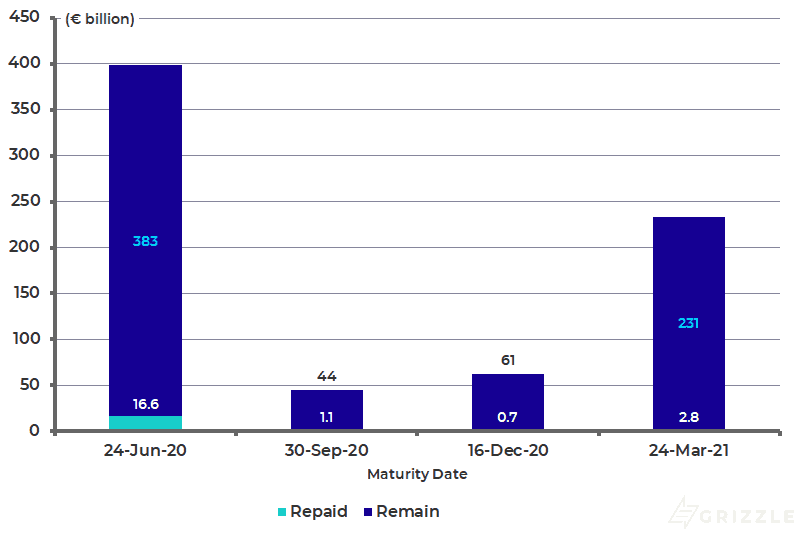

The need for a new TLTRO announcement, and the need for another “fix” for the Italian banks, stems from the reality that €719 billion of TLTRO loans are still outstanding and due to be repaid starting in June 2020, down only €21 billion from the peak of €740 billion that has been borrowed from the second TLTRO round (see following chart). (All of the €432 billion borrowed from the first round has matured and been repaid.)

Italian banks have reportedly taken up more than 30% of TLTRO funding while TLTROs account for 17% of their loans compared with a Eurozone bank average of 7%.

ECB TLTRO-II loans outstanding and repayments

Election Season is a Good Time to Fund Italian Banks

The above means it clearly makes sense, tactically, to underwrite the Italian banks prior to the European parliamentary election campaign which has the potential to trigger a renewed surge in Italian borrowing costs as the League and the Five Star Movement renew their attacks on the Brussels establishment.

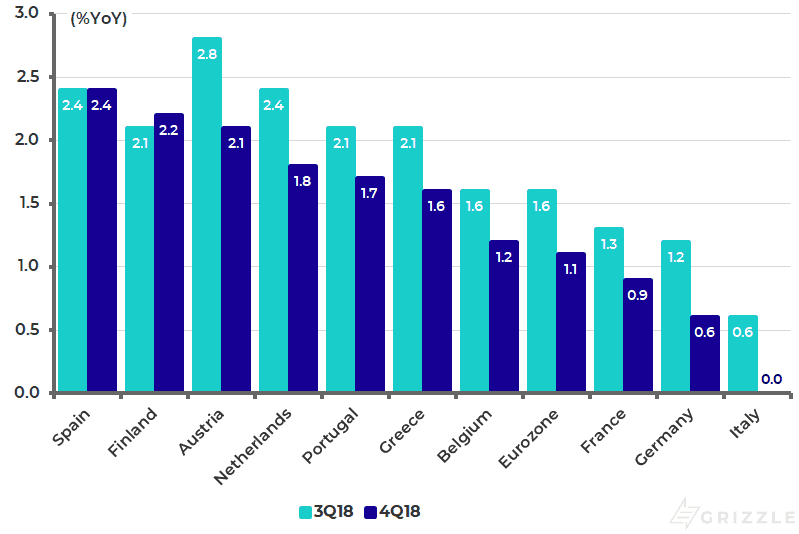

Fundamentally, however, the TLTROs have only at best bought time while the Italian economy is slowing again and indeed remains the worst performer in the Eurozone. Italian real GDP growth slowed from 0.6% YoY in 3Q18 to zero in 4Q18, while Eurozone and German real GDP growth slowed from 1.6% and 1.2% YoY respectively to 1.1% and 0.6% YoY (see following chart).

Major Eurozone countries’ real GDP growth

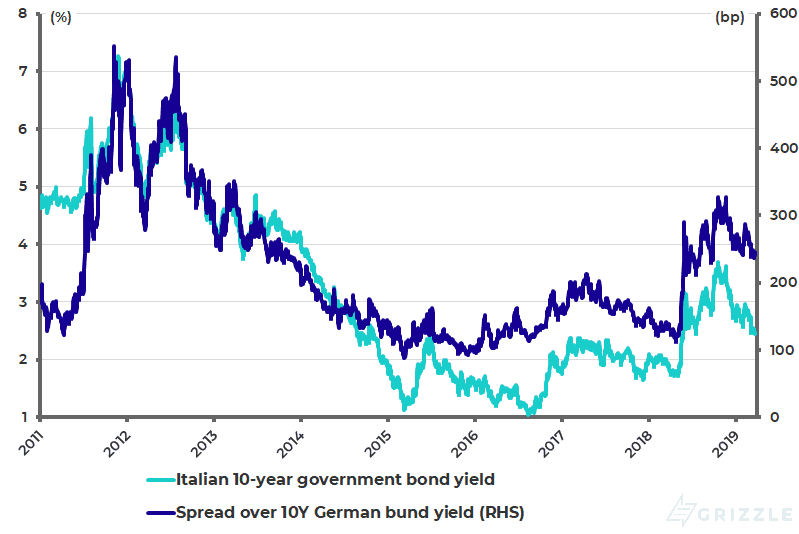

All this probably means that it is only a matter of time before markets refocus on Italian risk. With the Italian 10-year government bond yield having declined 124bp from a recent high of 3.69% reached in October 2018 to 2.45%, there is room for a sell-off (see following chart).

Italy’s most popular politician, right-wing populist and Interior Minister Matteo Salvini, will probably aim to call another general election later this year as a result of which he will hope to form a government independent of his current coalition partner, the essentially left-wing Five Star. In the meantime, Salvini will be looking to entrench his leading position in the polls with a good performance for the League in the European parliamentary elections.

Italian 10-year government bond yield and spread over 10-year German bund yield

The Italian case against Brussels, and the Maastricht Treaty in particular, has also improved of late given that French President Emmanuel Macron has been forced to deviate from the path of fiscal rectitude as a result of concessions made to the rioting gilets jaunes, the consequence of Macron’s foolish decision to blow political capital on “green” diesel taxes when 95% of light trucks in France run on diesel.

Italy’s “Doom Loop” Weighing it Down

From a fiscal standpoint, Italy has been running a primary surplus since 2010. The problem for Italy is the size of the stock of its government debt, and the so-called “doom loop” created by the Italian banks’ large holdings of Italian government bonds, in a fiscal context where debt servicing accounts for 8% of the government budget.

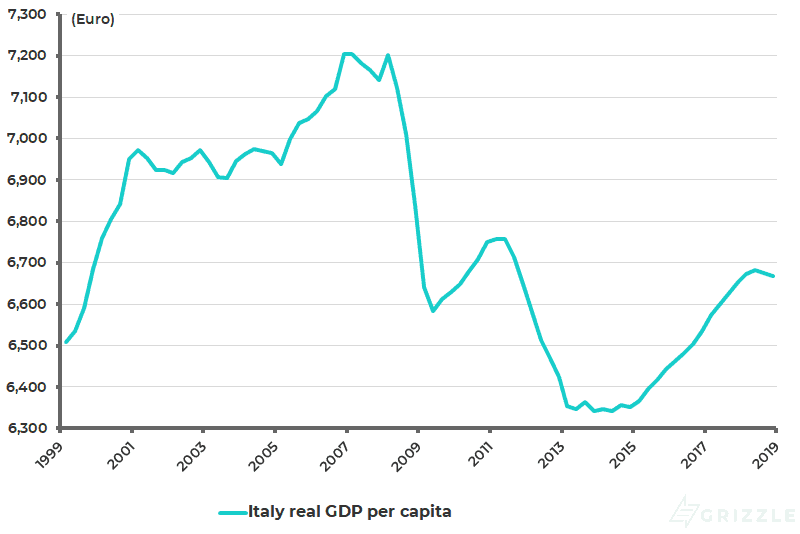

The above is why Italy remains the critical fault line in the Eurozone. The key point is that Italian real GDP per capita has barely grown in Italy since the formation of the euro at the beginning of 1999. Thus, Italian real GDP per capita is only up by an annualized 0.1% since 1999 (see following chart).

Meanwhile the other political development in the Eurozone worth noting is that Annegret Kramp-Karrenbauer (AKK), the recently elected leader of Germany’s ruling Christian Democratic Union (CDU) and the heir apparent to Angela Merkel, published an article in Die Welt on March 10 that made clear that she has major reservations about Macron’s drive to promote greater fiscal integration as a response to the surge in populist nationalism. To be precise, Kramp-Karrenbauer wrote: “European centralism, European statism, communitising debt and Europeanising social security systems and the minimum wage would be the wrong approach” (see Financial Times article “Kramp-Karrenbauer warns on EU reforms”, March 11, 2019).

Italy real GDP per capita

The above comments offer little or no hope for a renewed convergence of trade in the Eurozone based on assumed progress towards fiscal integration. That means if Berlin is not willing to support it, that integration is more likely to be forced later by a crisis when Germany wakes up to the liability facing the Bundesbank, via the Target-2 system, in the event of a breakup of the Eurozone.

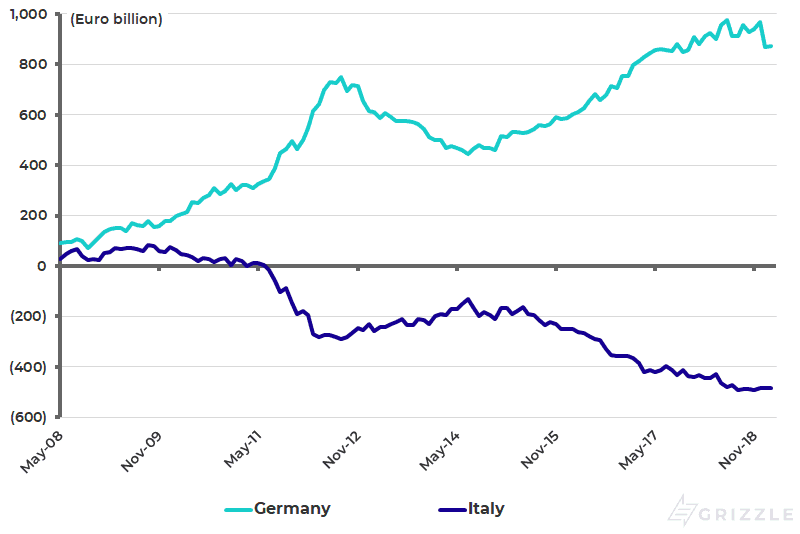

Germany’s Target-2 claims rose to a record €976 billion at the end of June 2018 and were €873 bilion at the end of February, while Italy’s Target-2 liabilities rose to a record €493 billion at the end of August 2018 and were €483 billion at the end of February (see following chart). The Bundesbank’s claims under Target-2 are now equivalent to 26% of Germany’s nominal GDP.

Germany and Italy Target-2 balance

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.