The Federal Reserve statement at the last FOMC meeting in March displayed no concern about the then 67bp rise in the 10-year Treasury bond yield since the previous meeting on 27 January.

The message conveyed was that the sell-off in the bond market has been a sign of a strengthening economy, not rising inflation concerns.

The Fed duly raised its 2021 real GDP growth estimate at that meeting from 4.2% to 6.5% and the core PCE inflation forecast from 1.8% to 2.2%.

But if the attention has remained mainly on the Fed of late, there have also been interesting developments of late as regards the European Central Bank.

But the question now is whether the ECB has moved to adopt yield curve control in terms of targeting nominal yields.

But, if so, it is a yield curve control that, so far at least, dares not speak its name.

The formal statement at the ECB meeting on 11 March committed the central bank to conduct quantitative easing purchases under its so-called Pandemic Emergency Purchase Programme (PEPP) at a “significantly higher pace than during the first months of this year.”

But the market has been left somewhat unclear as to exactly what the ECB is focusing on, at least based on the statements made by ECB President, Christine Lagarde, save for a general desire to ease financial conditions.

Lagarde has referred to a “holistic and multifaceted set of indicators” which the ECB is targeting as regards its quanto easing purchases.

This is hardly precise language.

But there is another member of the ECB Board, Fabio Panetta, a compatriot of former ECB head and now Italian Prime Minister Mario Draghi, who has been rather more specific.

Panetta, like Draghi, worked in the Italian central bank.

In a speech in early March on the subject of monetary policy and the way out of the pandemic, Panetta stated that “by keeping nominal yields low for longer, we can provide a strong anchor to preserve accommodative financing conditions”.

Panetta went on to say in the same speech: “Anchoring nominal yields allows real yields to fall … Implementing such a policy requires the central bank to broadly identify what level of nominal yields it is aiming to achieve; to tailor its purchases to achieve that level; and to be ready to intervene to the extent necessary.”

This sounds to this writer like a policy of targeting nominal yields, which also implies potentially unlimited balance sheet expansion on the part of the ECB.

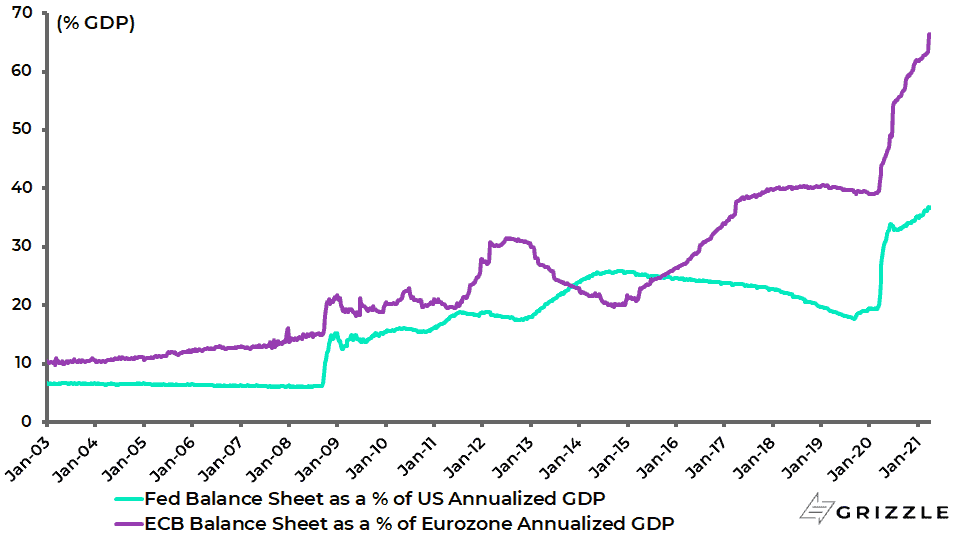

On this point, the ECB balance sheet is already much higher than the Federal Reserve’s as a percentage of GDP.

Since the onset of the policy response to the pandemic, the ECB balance sheet has risen from €4.69tn or 39% of Eurozone annualised GDP at the end of February 2020 to €7.51tn or 66.5% of GDP.

While the Fed balance sheet has risen from US$4.16tn or 19% of US annualised GDP to US$7.79tn or 37% of GDP over the same period.

Fed and ECB Balance Sheets as % of GDP

Indeed the ECB balance sheet has been rising at a more rapid rate than the Fed’s since mid-June 2020, rising by 41% in US dollar terms, compared with a 9% increase in the Fed’s balance sheet over the same period.

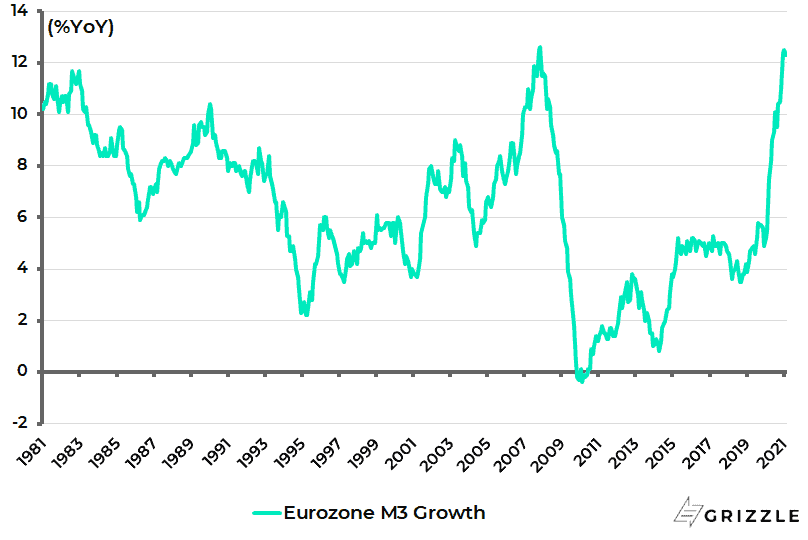

Meanwhile, as with the US, inflation expectations have been rising in the Eurozone as has broad money supply growth.

Eurozone M3 growth was 12.5% YoY in January, the highest level since November 2007, and was 12.3% YoY in February.

Eurozone M3 Growth

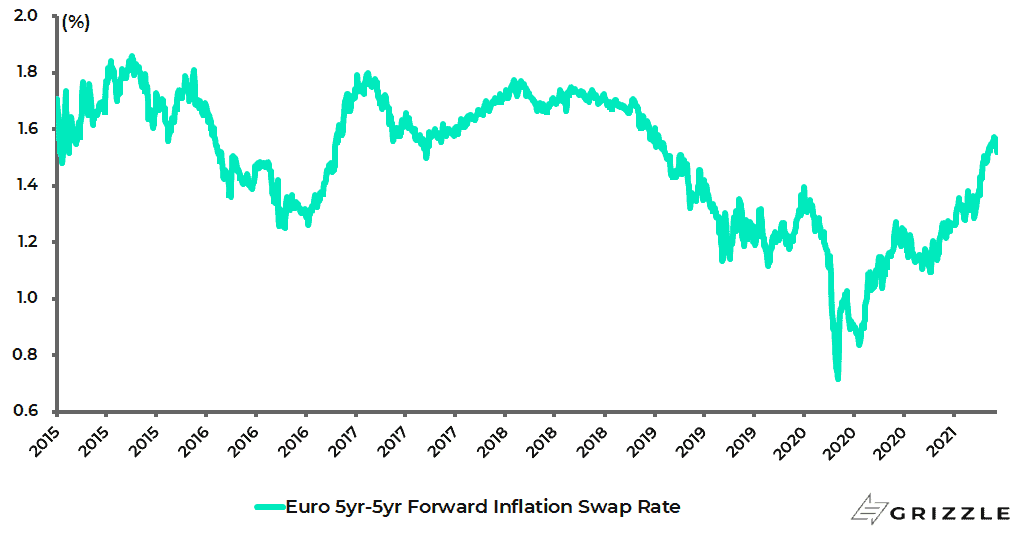

While the Eurozone 5-year 5-year forward inflation swap rate has risen from a low of 0.72% in March 2020 to 1.57% on 9 April 2021, the highest level since January 2019, and is now 1.52%.

Eurozone 5-year 5-year Forward Inflation Swap Rate

In this context, it is interesting to note that 16 German economists and businessmen filed a 140-page legal complaint accusing the ECB of “blatant monetary financing of states” in breach of Article 123 of the Lisbon Treaty last month (see Die Welt article: “Krasser Fall von Staatsfinanzierung” – EZB wird an Grenzen ihres Mandats erinnert, 11 March 2021).

Still the base case of this writer remains that legal challenges to the ECB through the German constitutional court will ultimately get nowhere unless they have the key political support.

And that does not appear to be forthcoming.

German Chancellor Angela Merkel played a critical role in enabling Mario Draghi to break all the founding rules of the euro and the ECB during the Eurozone Crisis, just as she played a key role in the establishment last year of the Eurozone’s €750bn Next Generation EU (NGEU) Recovery Fund which has been viewed, correctly, as an important incremental step on the path to fiscal union.

Indeed Panetta referred to this in his speech when he said that NGEU provides “an opportunity, for the first time ever, to achieve genuine European fiscal stabilisation backed by common debt issuance”.

That comment will not be music to the ears of hard-working German savers.

Meanwhile, closet yield curve control in the Eurozone clearly has potentially bearish implications for the value of the euro since, as already noted, it implies unlimited balance sheet expansion.

Still, from another viewpoint, further moves towards fiscal union are euro bullish since they imply the German taxpayer underwriting the rest of the Eurozone which makes the fiscal situation sustainable for longer.

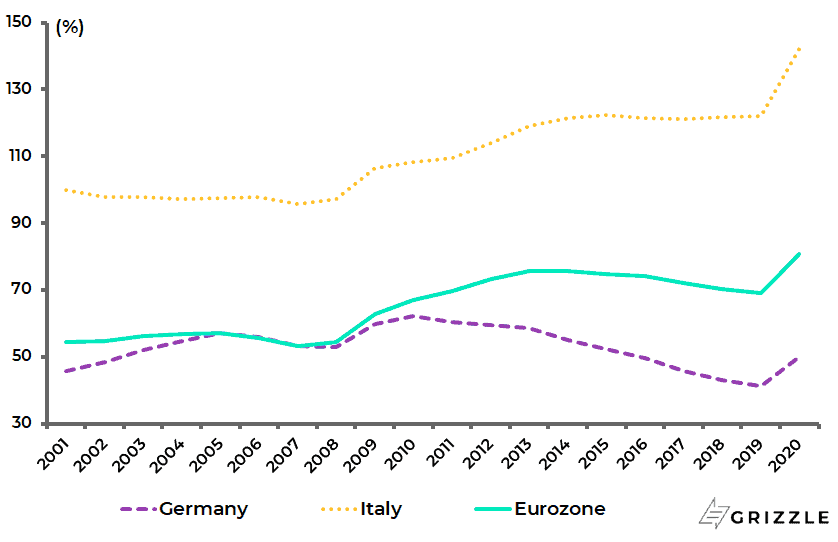

German net government debt as a percentage of GDP was only an estimated 50% at the end of last year, according to the IMF, compared with 142% in Italy.

Germany, Italy and Eurozone Net Government Debt to GDP

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.