The Economist has a long-established tradition of contrarian cover signals, as have other business magazines, some of which are now no longer.

This is because most hacks, though to be fair not all, tend to be backward-looking not forward-looking.

On this point, The Economist famously called the bottom in the oil price in early 1999 when the Brent oil price bottomed at US$9.55/bbl in late 1998 and started rallying in early 1999 (see The Economist magazine: Drowning in oil, 6 March 1999). It may just have done the same last month with its cover story on 21st century power (see The Economist: “21st century power: How clean energy will remake geopolitics”, 19 September 2020).

Expensive Windmills and Lower Stock Prices

Amidst all the escalating noise about renewables and green investments, it is worth noting that the more successful the world is at eliminating fossil fuels, the more likely the price of oil is going to increase, and the more profitable it is going to be to produce.

This is because fossil fuels still account for 84% of world energy demand.

That should be positive for oil companies’ share prices long-term assuming any fund manager is still allowed to buy them.

But the problem is that some of them, like BP of late, have started buying windmills in a bid to become ESG compliant.

For example, BP announced in early August a plan to shrink its upstream business by 40% by 2030 and invest US$5bn a year in low carbon energy, up from around US$500m/year currently.

This planned investment in renewables will be “expensive” and is likely to get much more expensive in the event of a Biden victory, and a resulting Green New Deal, which is likely to lead to a boom-bust cycle in green assets characterized by epic overinvestment in the alternative energy space.

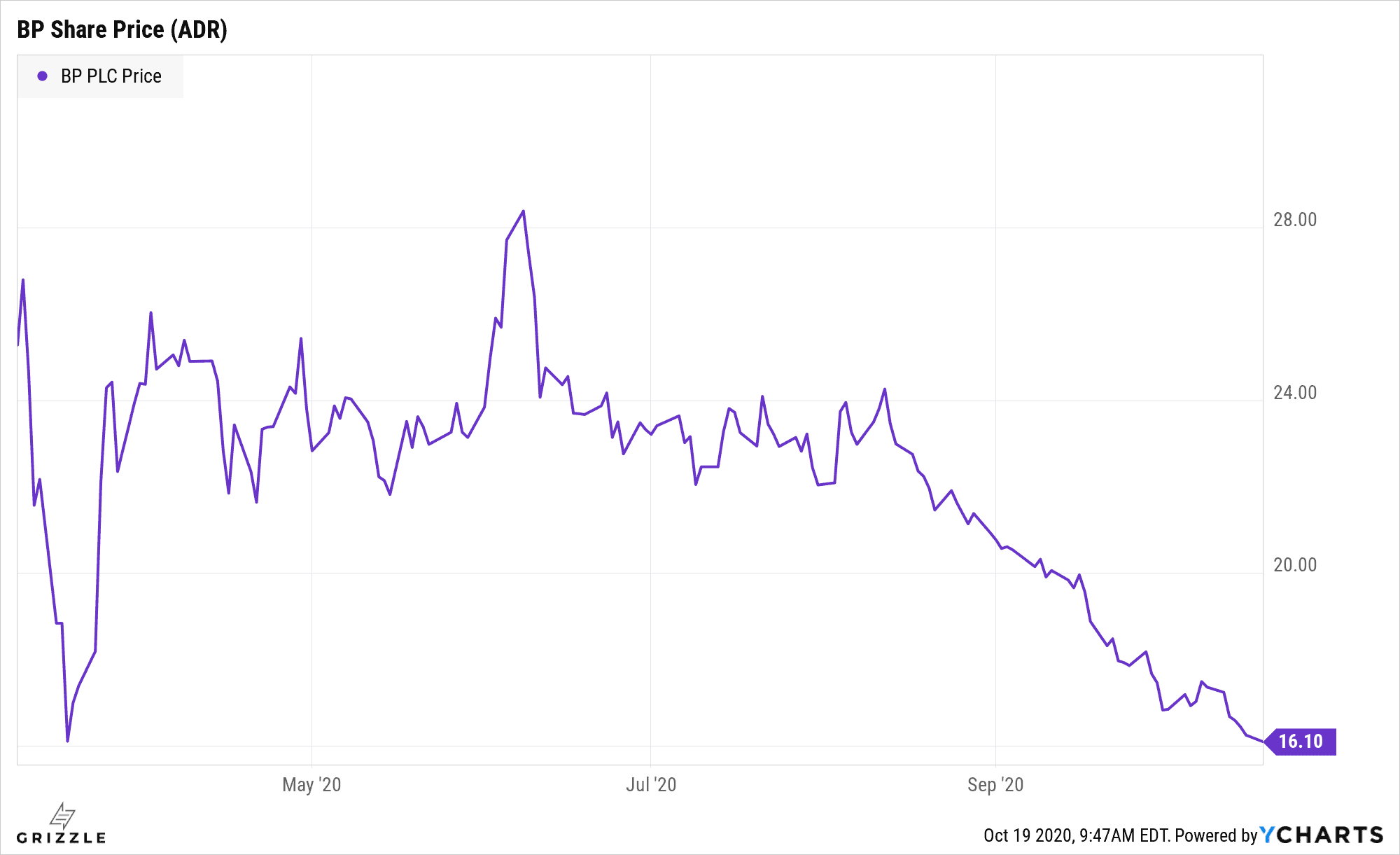

This appears to be one reason BP’s share price has sold off since the wind energy announcement.

BP and Equinor announced on 10 September the formation of a strategic partnership to develop offshore wind energy in America.

BP will also pay US$1.1bn to purchase a 50% interest in both Empire Wind and Beacon Wind assets from Equinor.

BP’s share price has declined by 23% since 8 September.

BP Share Price

Overinvestment in Renewables Will Lead to Higher Oil Prices

Meanwhile, it was interesting to read a comment by a senior executive at Russia’s largest state-owned oil company, Rosneft, recently that the likes of BP and Shell were creating an “existential crisis” for oil suppliers with their shift towards renewables.

Didier Casimiro was quoted as saying: “We will have a (supply) crunch, price volatility and, yes, higher prices” if the world goes back to pre-Covid levels of oil demand (see Financial Times article: “Rosneft attacks rivals’ shift to renewables”, 29 September 2020).

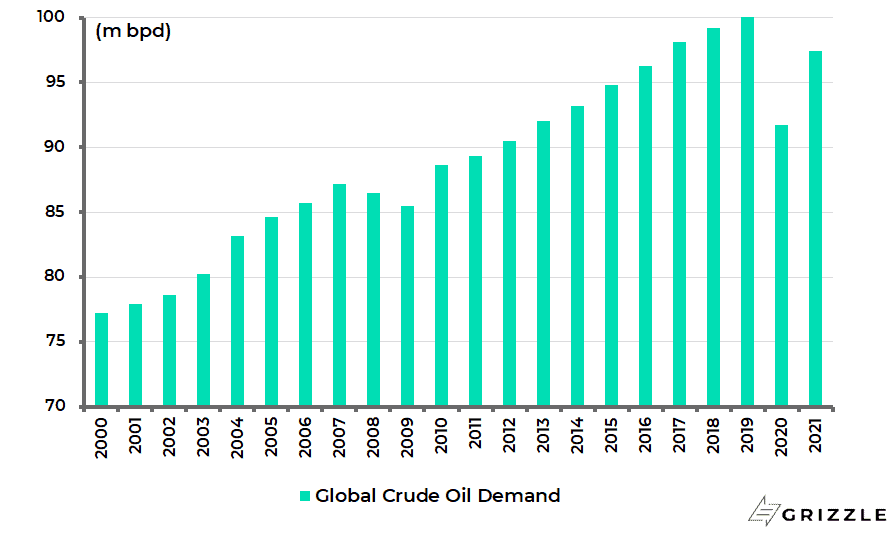

Remember that there was record global oil demand of 100m barrels/day in 2019.

Global Crude Oil Demand

Meanwhile the best book GREED & fear has read this year, though it was not published this year, remains “The Moral Case for Fossil Fuels” by Alex Epstein.

Published back in 2014, among the many points made by the author is that the oil companies should stop apologising for what they do.

This writer agrees but it is clear that some of them have already started to capitulate on this score.

Investors should favor those who have not.

Meanwhile, this writer’s view remains that the emerging markets, in particular, will be consuming oil for many years yet and that oil demand in 2021 will be much closer to the 2019 record year of 100m b/d than assumed by believers in “the new normal”.

Still, there is no doubt, whatsoever, that a Biden victory will further accelerate the alternative energy boom with the proposed US$2tn Green New Deal.

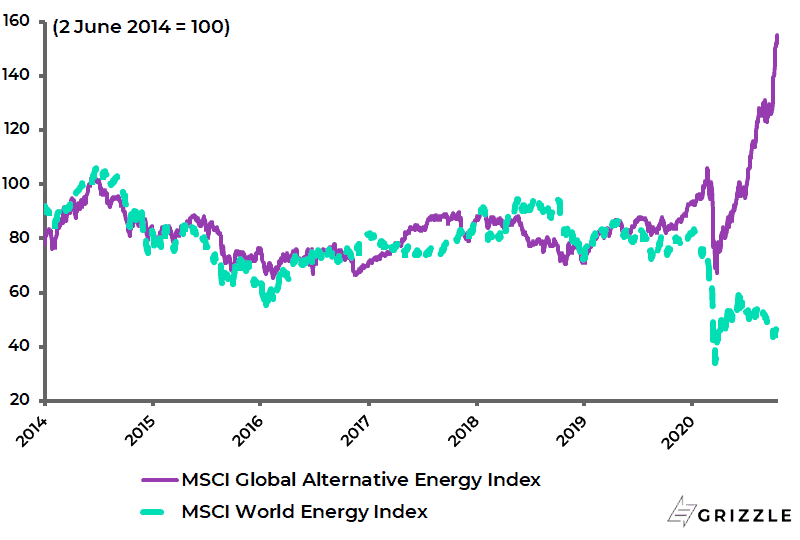

This explains why, as expectations have risen of a so-called “Blue Wave” in the forthcoming US presidential election, alternative energy stocks have rallied hard as energy stocks have collapsed.

The MSCI World Energy Index has declined by 29% in US dollar terms on a total-return basis since early June, while the MSCI Global Alternative Energy Index is up 55% over the same period.

MSCI Global Alternative Energy Index and MSCI World Energy Index

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.