Major oil producer Exxon Mobil (NYSE: XOM) reported earnings that missed estimates.

On the bottom line earnings per share were a loss of -$0.14, well below estimates for earnings of $0.04/sh

Cashflow of $6.3Bn was generally in line with street estimates of $6.34Bn.

Results this quarter are really an afterthought with the market focused on how quickly demand will recover as consumers start to venture back outside in the coming months.

Grizzle has been all over this oil trade and told investors on April 3rd there was more pain to come in the oil market.

We then flipped on April 20th and said the oil price had bottomed and we were buyers of Exxon Mobil and others.

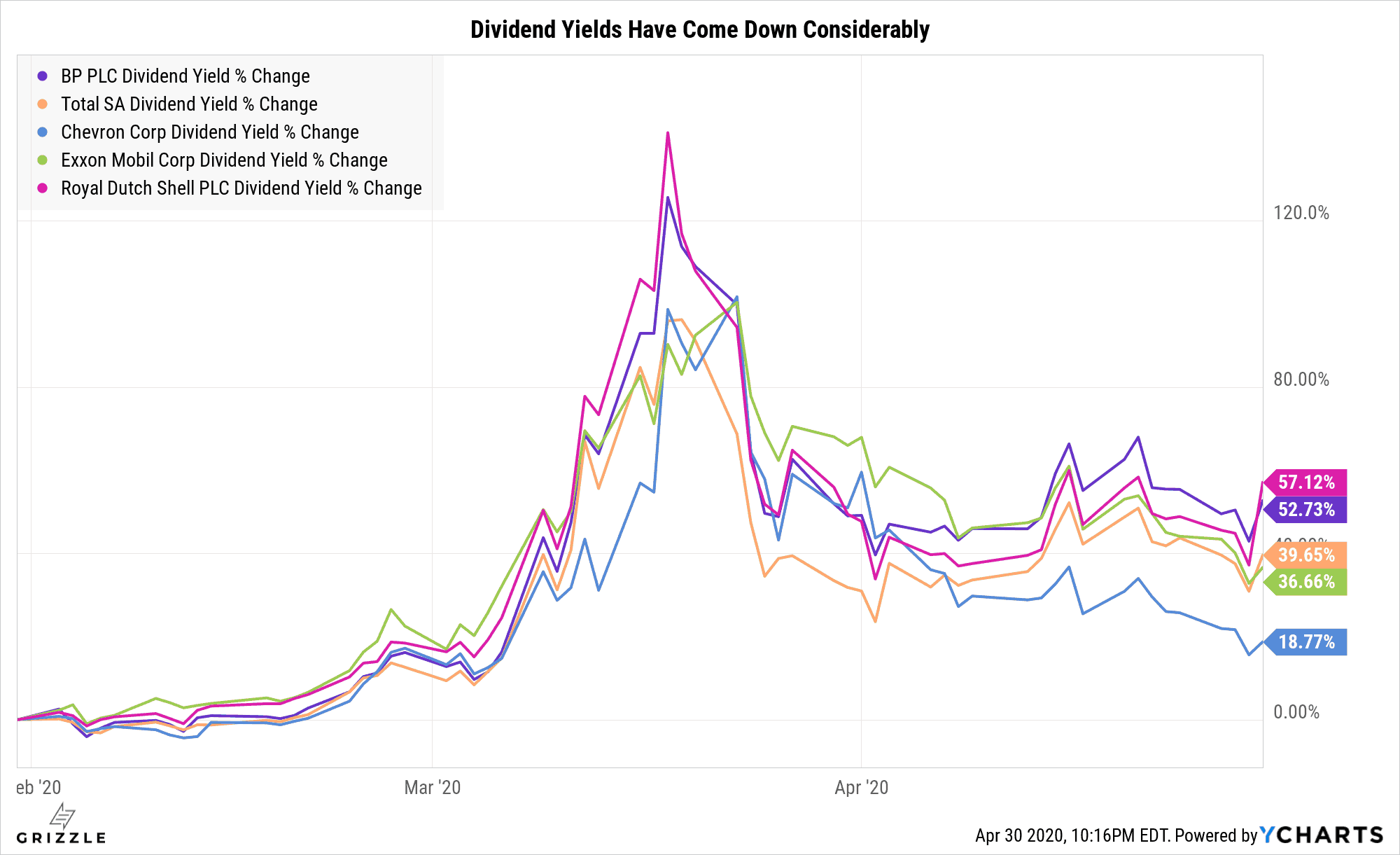

Investors in major oil producers own mostly for the dividends and little else.

What this means is the only valuation measure you need to look at is the dividend yield.

Every major oil company’s dividend yield peaked in late March, but some have come back more than others as the stock prices recovered.

The dividend could still be cut at some of these companies depending on how long the oil price stays this low, but for now, it looks like Exxon and Chevron are the closest to trading back to pre-Coronavirus levels.

Exxon management looks to be strongly committed to the dividend and does not want to kill the 100-year streak of rising dividend payments.

With the dividend cut risk off the table, this stock still offers 18% more yield than back in February though that isn’t much when you consider what a sorry state the oil market is currently in.

[su_panel]Exxon is up almost 50% since late March and though supply is falling, demand will take time to rebound. This stock is pricing in a quick rebalance in the oil market and we would be taking at least some profits as we expect a short term peak is fast approaching. If the stock dips in the coming weeks it will be time to buy and hold for another 12-18 months. [/su_panel]Exxon’s Dividend Yield is no Longer Quite as Juicy

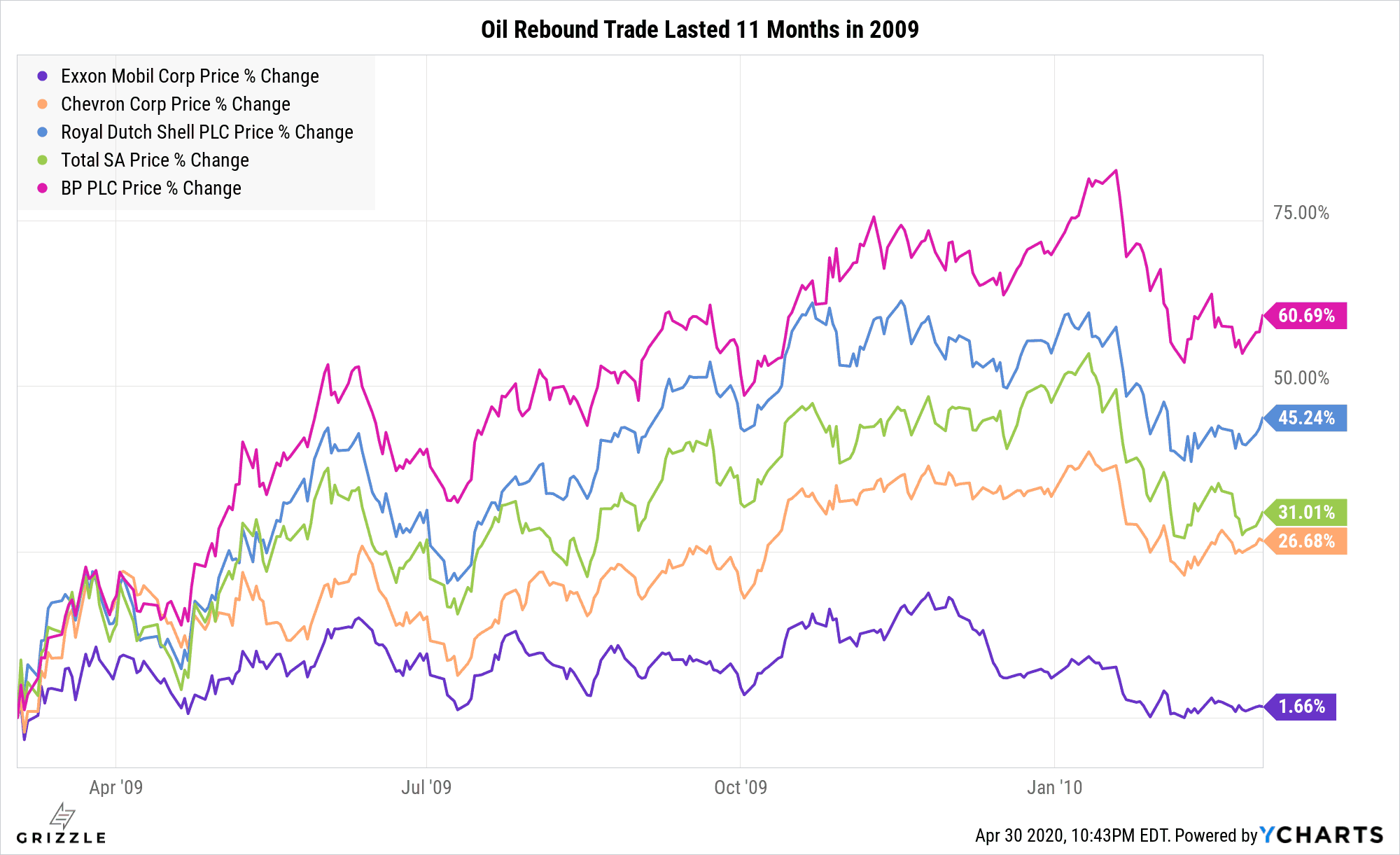

Going back to the last demand-driven oil recession in 2008 we can see the big money on the oil rebound trade was made relatively quickly.

Dividend yields peaked and stock prices bottomed in March 2oo9.

By June 2009 the stocks had already peaked and then took another year and a half to reach a post-recession high.

What this should tell you is the long Exxon and other major producer trade may be quickly running out of steam.

XOM Stock Price Peaked Only 3 Months After the Bottom in 2009

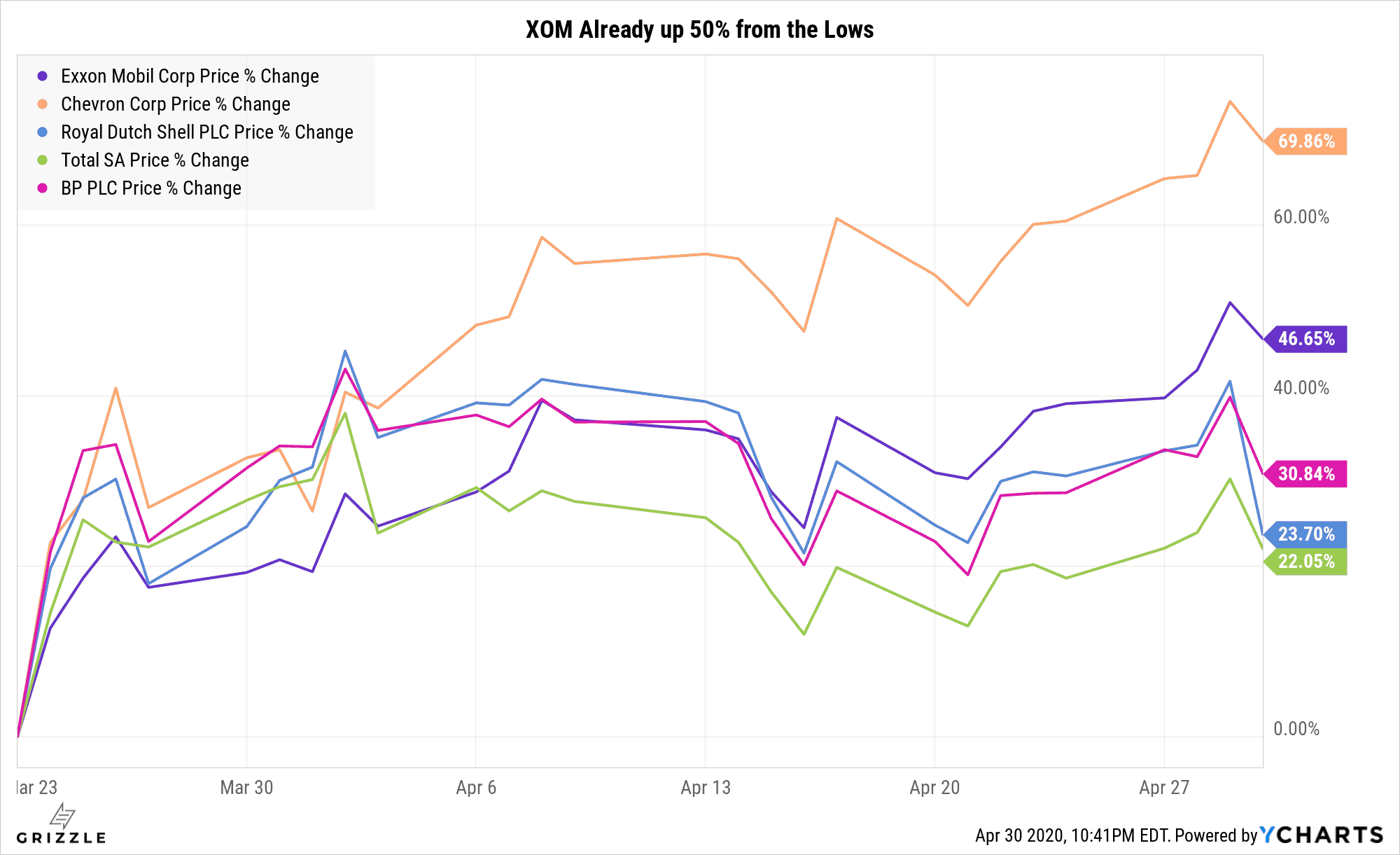

In the current rebound Exxon is already up 47% while the worst-performing stock, BP is still up 22%.

With oil prices still sub $20 per barrel in the U.S. and an uncertain road to recovery from the ongoing pandemic, we would be taking some profits if these stocks run much further.

Now is not the time to be buying Exxon Mobil or any of these five oil stocks in size.

We most definitely think the stocks will go higher as oil rebounds back to a normal level of $30+ per barrel, but in the next 1-2 months, we think these stocks may go sideways at best.

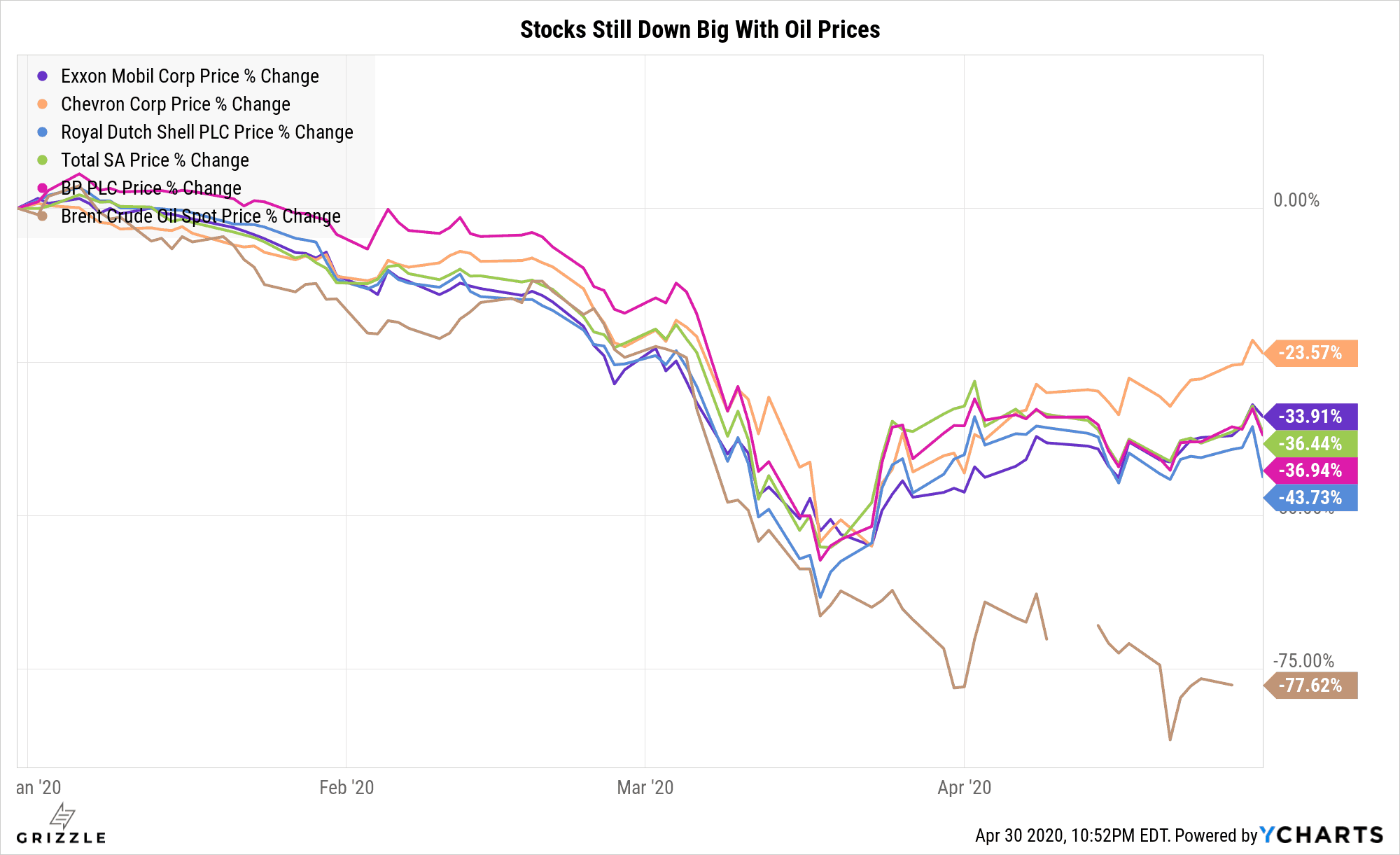

Is This Fierce Oil Stock Rebound Warranted?

Though the stocks are still down 20-40% since the start of the year, this performance is most definitely warranted with oil prices down a staggering 77%.

Though very low prices mean weaker players will go bankrupt quickly, rebalancing the market even faster, the demand part of the equation is totally out of the oil markets’ hands.

If the Coronavirus lingers longer than the market expects and the world doesn’t go back to normal by the fall, even the largest oil company’s will have to start making hard decisions about if they cut their dividends.

No one who producers oil can survive long with prices below $30/bbl

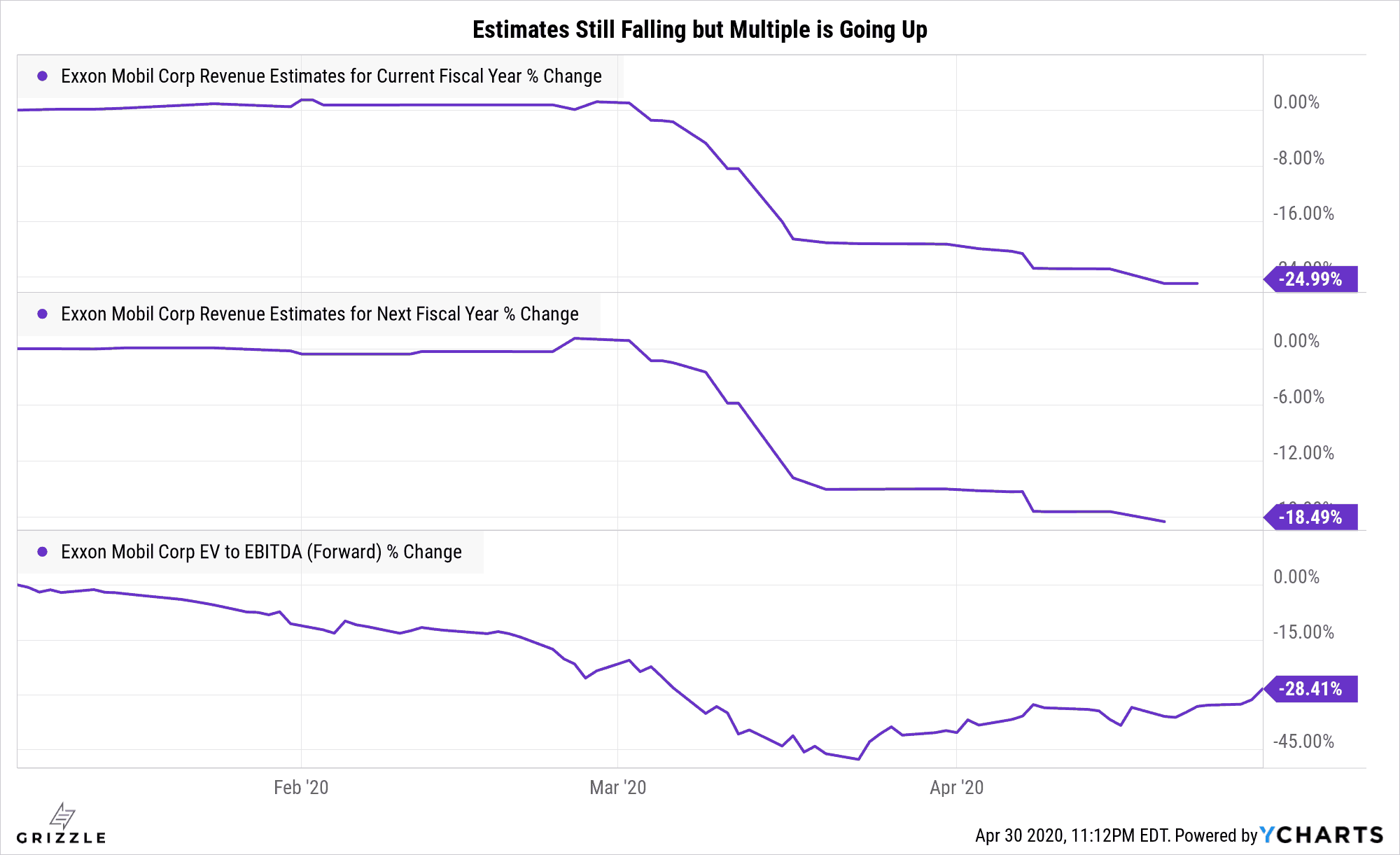

Analysts are still cutting their revenue estimates for 2020 and 2021, but Exxon’s multiple is back on the rise.

Exxon is now only 30% cheaper than at the start of the year while the oil price has fallen almost 80%.

This tells us a rebound is already at least partially baked in.

Disclosure: The author owns shares and call options on Exxon Mobil.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.