Facebook (NASDAQ:FB) reported another quarter of stellar results beating both EPS and Revenue estimates.

Revenue of $21.08 beat consensus of $20.9 billion while EPS of $2.56 beat the consensus of $2.53 by 1%.

This is the 9th straight quarterly beat and demonstrates what a strong competitive position Facebook is in.

Users continued to grow with monthly active users (MAU) up to 2.5 billion from 2.45 billion last quarter and 2.3 billion the same time last year.

Monetization of users was very strong up 16% over the same time last year.

Revenue per user (ARPU) hit $8.43 this quarter, up from $7.26 last quarter and $7.37 a year ago.

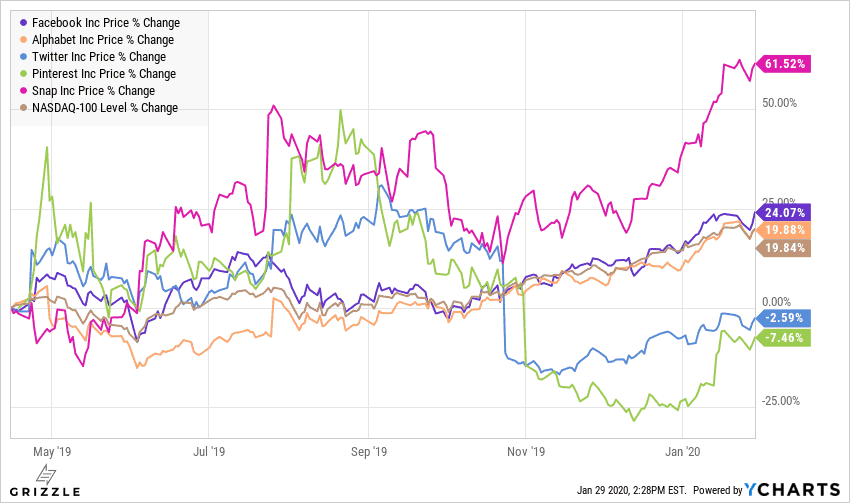

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Even with antitrust concerns holding down the multiple, Facebook remains a juggernaut in digital advertising. This quarter’s earnings did nothing to change our view that this is a must-own tech stock until we see the U.S. government come knocking on the door. [/su_panel]Facebook has outperformed the Nasdaq composite and most peers in the last 12 months, rising ~24%, beating out all peers but Snap.

FB Stock Second Best Performer in 2019

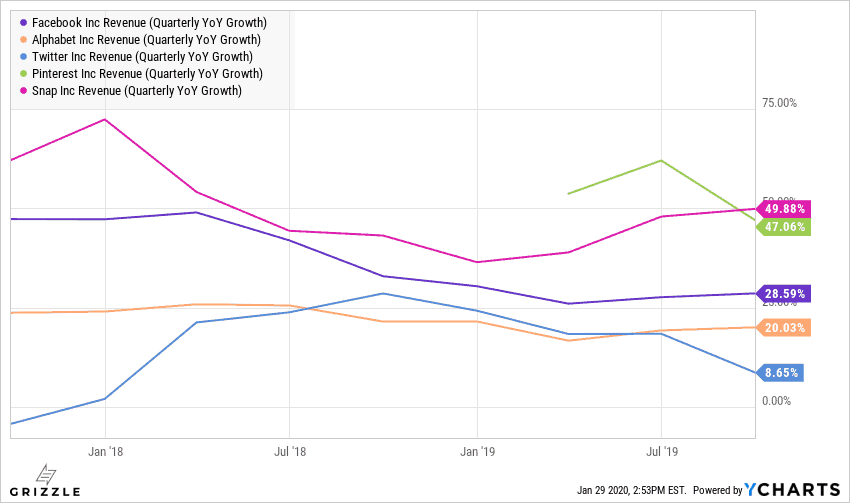

Even though revenue growth has been on the decline for Facebook, they have done an excellent job slowing the decline in 2019.

For a company generating $20 billion a quarter to be growing at almost 30% a year is a crazy achievement.

We suspect if Facebook starts to struggle with new avenues of growth, management can just pull back on investment and turn it into a dividend and buyback machine ala Apple.

Quarterly YoY Revenue Growth

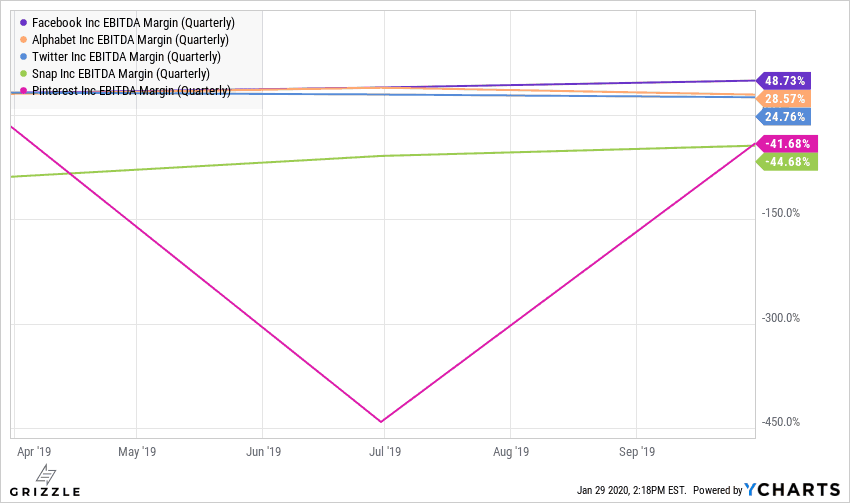

Looking at profitability, Facebook continues to far outclass peers.

The EBITDA margin (a proxy for cashflow) is a full 70%-80% higher than Google and Twitter and far outclasses money-losing Snap and newly public Pinterest.

When you own a commanding piece of the online ad market you can generate above-average profits.

Facebook EBITDA is Still Way Above Peers

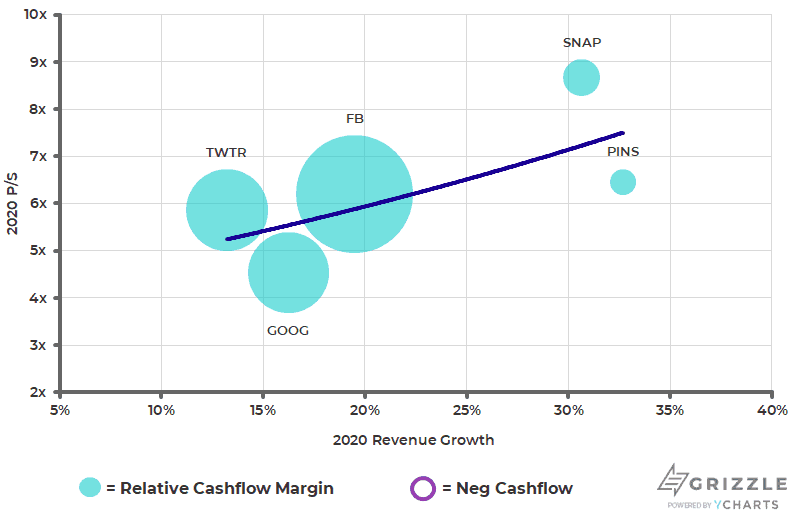

Looking at valuations, Facebook still looks slightly cheap, likely explained by all the worries about the government cracking down on the tech giants.

FB revenue growth should be slightly above 20% in 2020 with an EBITDA margin of 51% which is still far above Google, Twitter, and other social media stocks.

Facebook continues to be in a league of its own.

Forward P/S Multiple vs 2020 Sales Growth

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.