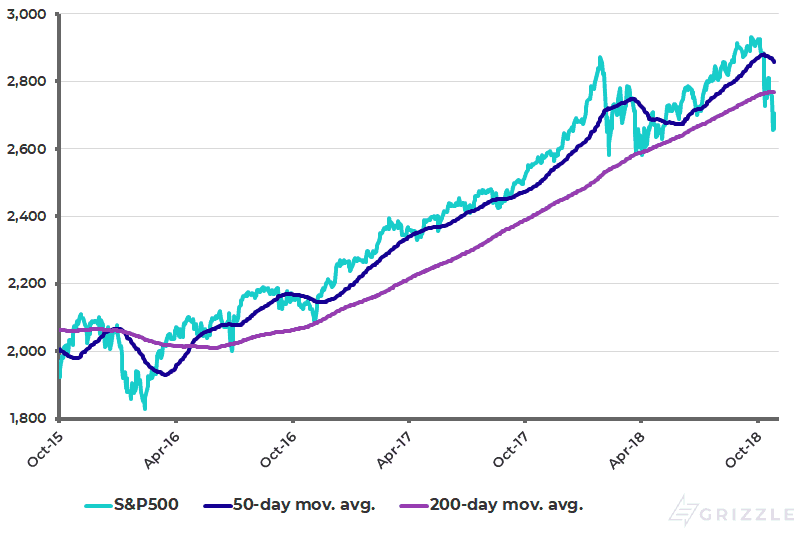

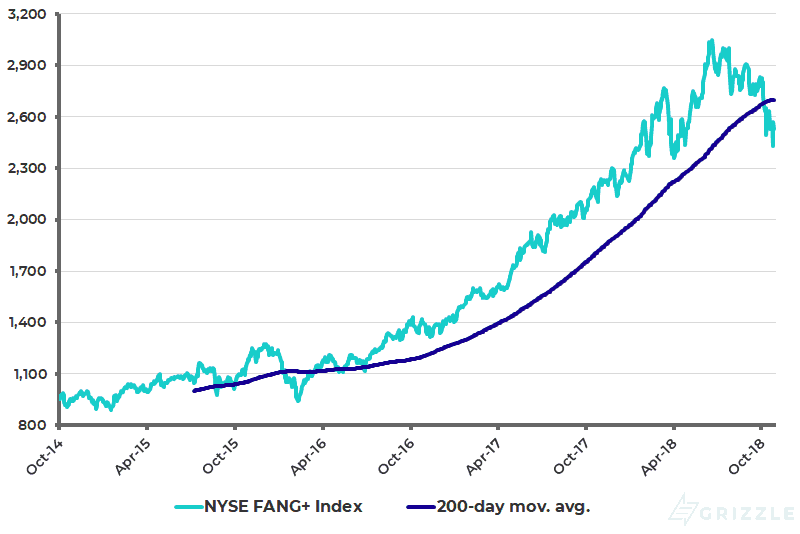

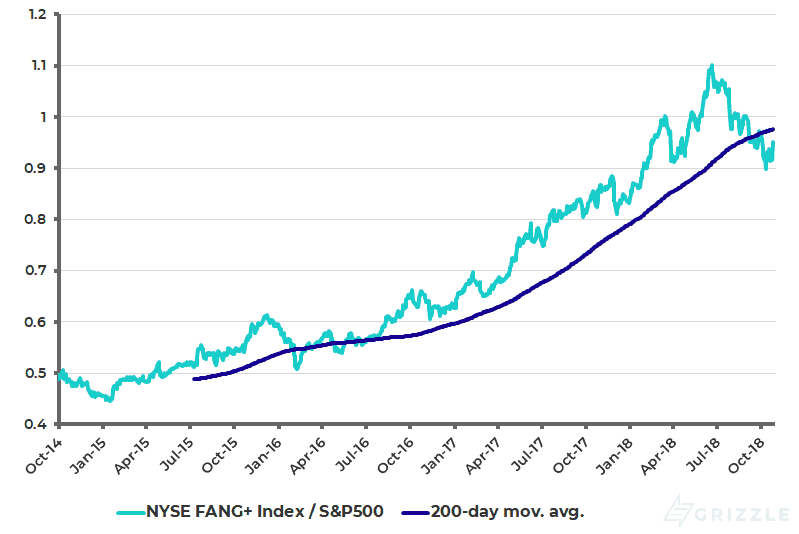

The recent breakdown of the S&P500 has revived the base case triggered by the ‘short vol’ unwind in February. That is that the S&P500 has reached a peak in this cycle (see following chart). It is also significant that the FANG stocks index, which have comprised the market leadership for the bull market, broke below its 200-day moving average on Oct. 5 for the first time since early 2016 (see following chart). The NYSE FANG index relative to the S&P500 has also broken down from the 2016-2018 uptrend, implying further FANG underperformance (see following chart).

S&P500

NYSE FANG+ Index

NYSE FANG+ Index relative to S&P500

US Dollar: Short-term Bull But Long-term Bear

Obviously, none of the above means that Asia and emerging markets will stop being correlated to a further Wall Street decline. It just means that there is a hope of renewed outperformance for emerging markets, most particularly if the US dollar peaks out. But for that to happen requires confirmation that the Federal Reserve tightening cycle is ending and this is not yet in sight.

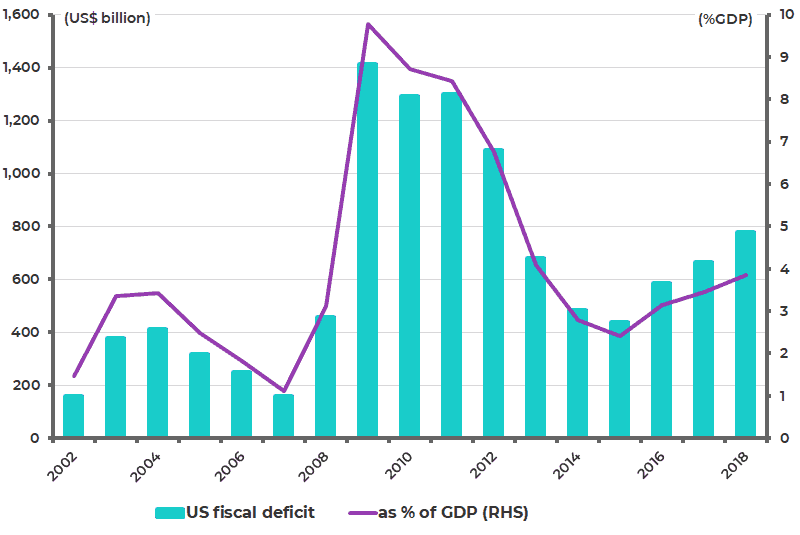

Donald Trump’s increasingly overt criticism of the Fed over the past two weeks has put one dent in the dollar, as has the latest official confirmation of the surge in America’s fiscal deficit. The US Treasury Department reported this month that the fiscal deficit for FY18 ended Sept. 30 increased by 17%YoY to US$779 billion (see following chart). This is a reminder that, while the macro ‘combo’ of monetary tightening and fiscal easing is US dollar bullish in the short- to medium-term, it is long-term bearish.

US fiscal deficit

Stock Market Peaked Despite Rising Profits

Meanwhile it is always worth asking the question what could be wrong with the above base case, namely that the US stock market has now peaked for the cycle, with the technical damage done to the market leadership in terms of the FANG stocks. The obvious answer is that earnings growth in America remains robust with 3Q18 earnings reported so far in this earnings season up 23.7%YoY, according to Bloomberg. It also remains the case that both top line sales and profit margins continue to rise.

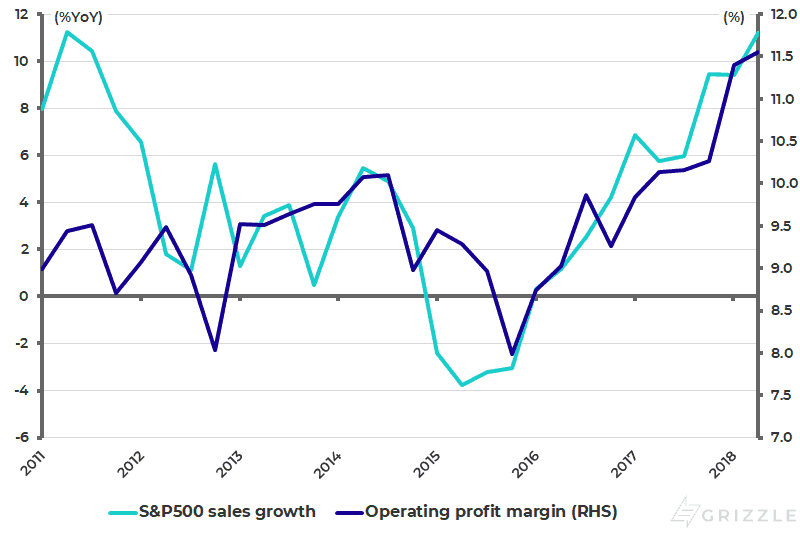

Sales by S&P500 companies rose by an estimated 11.2%YoY in 2Q18, the highest revenue growth in seven years, according to S&P Dow Jones Indices, while the S&P500 profit margin has risen from 8% in 4Q15 to 11.5% in 2Q18 (see following chart).

The rising profit trend is also reflected in the latest US macro data on corporate profits. The macro measure of after-tax corporate profits reported by the Bureau of Economic Analysis rose by 15.8%YoY in 2Q18, the highest growth rate since 1Q12. This is impressive even allowing for all the distortions to earnings driven by repatriation of corporate funds from offshore and the related renewed surge in share buybacks.

S&P500 sales growth and operating profit margin

Rising Labour Costs

If earnings growth remains robust in America, and also superior to what is seen in other equity markets globally, the obvious risk, aside from Fed tightening, is the impact to profit margins from rising costs. And labour is the largest cost for most companies. This is another reason, beyond its impact on monetary policy, why wage-related data remains critical to monitor.

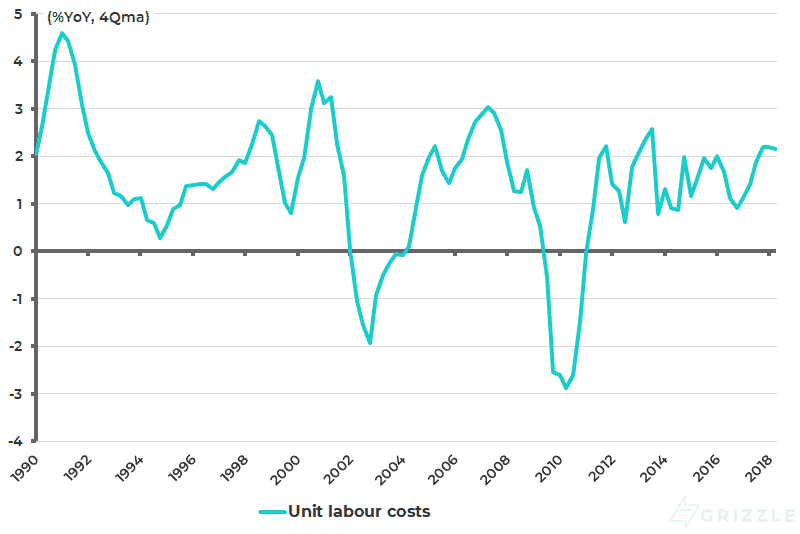

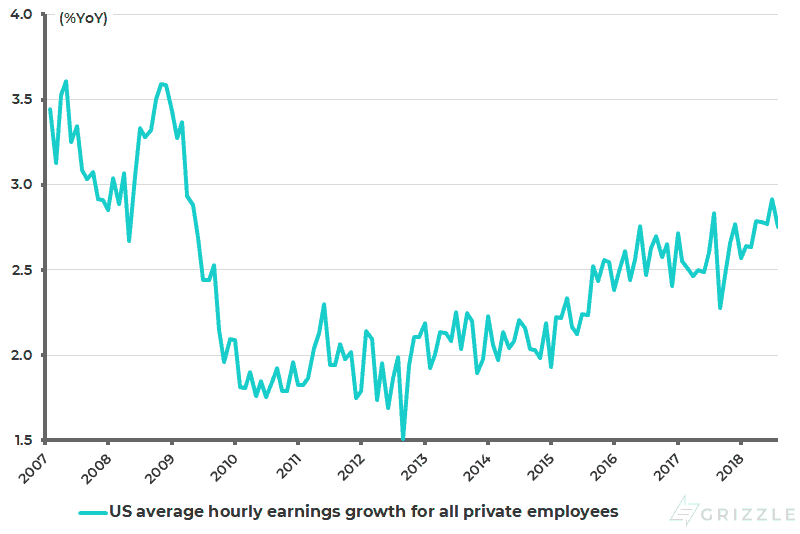

From a corporate standpoint, unit labour costs are rising but not yet alarmingly so. US nonfarm business sector unit labour costs rose by 2.2%YoY in the four quarters to 2Q18, up from 0.9%YoY in 2016 (see following chart). Meanwhile, average hourly earnings and other wage-related data continue to trend up but, again, not yet alarmingly so. US average hourly earnings rose by 2.8%YoY in September, down from 2.9%YoY in August which was the highest level since May 2009 (see following chart).

US unit labour costs (%YoY, 4Qma)

US average hourly earnings growth

Still, importantly, the base effect suggests that average hourly earnings growth is likely to accelerate in coming months. US average hourly earnings declined by 4 cents or 0.2% in October 2017. Assuming a monthly increase of 8 cents or 0.3%, which is the average monthly increase over the past three months, average hourly earnings growth will accelerate to 3.2%YoY in October. If this is indeed the case, it is likely to accelerate Fed tightening expectations to the detriment of the stock market.

Regulation Poses the Greatest Threat

Meanwhile, if cost pressures are a traditional threat to profit margins in a conventional economic cycle, this time is rather different since the market leadership has been the FANG stocks and, for them, the big risk is not rising costs but rather regulation or technological disruption; both of which could potentially demolish these ‘winner takes all’ business models entirely.

From a regulatory standpoint, the risks in America are again rising after the reprieve granted to Facebook Chairman and CEO Mark Zuckerberg following his Congressional testimony in April. Since then there have been more highly published data breaches at both Google and Facebook while, perhaps most damaging of all, both companies are fast becoming ‘uncool’. It is about time. These companies will increasingly be held responsible for the content on their platforms. The problem is, of course, that the geeks running these companies have no competence in editorial matters and probably never will have.

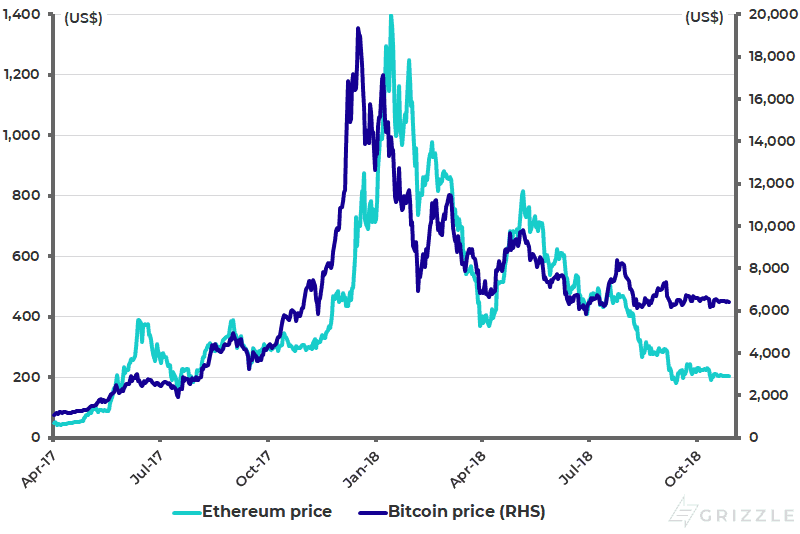

The other obvious threat to the Silicon Valley ‘scalable’ business models and related ‘network effects’, to quote some of the favoured jargon of the current cycle, is the decentralized model provided by blockchain technology. This is why this whole area is still interesting despite the vaporization in prices seen so far this year. Bitcoin is now down 68% from the peak, and Ethereum down 86% (see following chart).

Bitcoin and Ethereum prices

Can FANG Be Disrupted?

It was also interesting to read recently that the philanthropic founder of the Internet, Tim Berners-Lee, has just launched a startup called Inrupt, whose mission is to decentralize the internet and take power back from the digital monopolies (see Fast Company article: “Tim Berners-Lee tells us his radical new plan to upend the World Wide Web”, Sept. 29 2018).

This writer has no idea if Inrupt can be monetized but wishes the admirable Mr. Berners-Lee well. The point, as noted in the above-mentioned article, is very simple. In the centralized web, data is kept in silos controlled by the companies that build them. In the decentralized world envisaged by Inrupt there will be no silos. Meanwhile, it is beyond this writer why individuals and corporates are so trusting in the ‘cloud’ — just as it is beyond comprehensive why major media outlets gave away their contents to the ‘newsfeeds’ of the digital monopolies.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.