Fastly, a provider of web-based speed software (NYSE:FSLY) reported results that disappointed the market.

The stock is down about 13% in after-hours trading as investors ignored a revenue and earnings beat and focused on disappointing earnings guidance for next quarter and continued losses expected in 2020.

Management reported 288 enterprise customers this quarter, up from 274 last quarter and growth of 27% from a year ago but only 5% growth from last quarter.

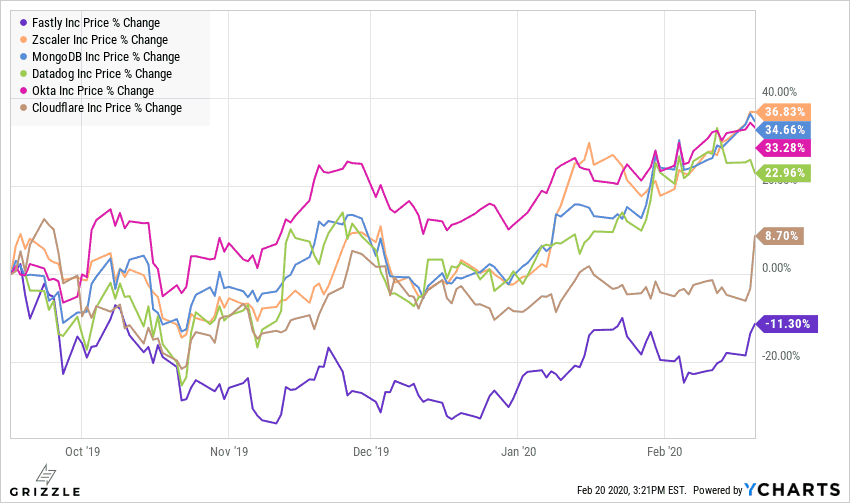

Fastly is the worst-performing stock in the peer group since September due to slower than average growth and larger than average losses. Results today are unlikely to change the narrative and the stock will continue to struggle without a clear path to profitability or a reacceleration of growth.

Software Stock Performance Since September

Revenue came in at $59 million, 8% better than consensus of $55 million and guidance of the same amount.

Revenue growth of 45% accelerated from last quarter’s growth of 35% which is a positive sign, but was ignored by investors.

The earnings per share loss of -$0.10 beat consensus and management guidance of an -$0.11/sh loss.

The market looked through this quarter’s results and focused on guidance for Q1 2020 that was 9% worse than expected and guidance for the full year 2020 of $30-$40 million of losses.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]In a sector that values growth above all, Fastly isn’t showing the market enough of it. Management needs to start shrinking losses quicker than they are today or show a reacceleration in customer growth from the currently anemic 5% per quarter. The stock will continue to underperform peers like Zscaler, CloudFlare and MongoDB in our opinion until either of these catalysts show up. [/su_panel]

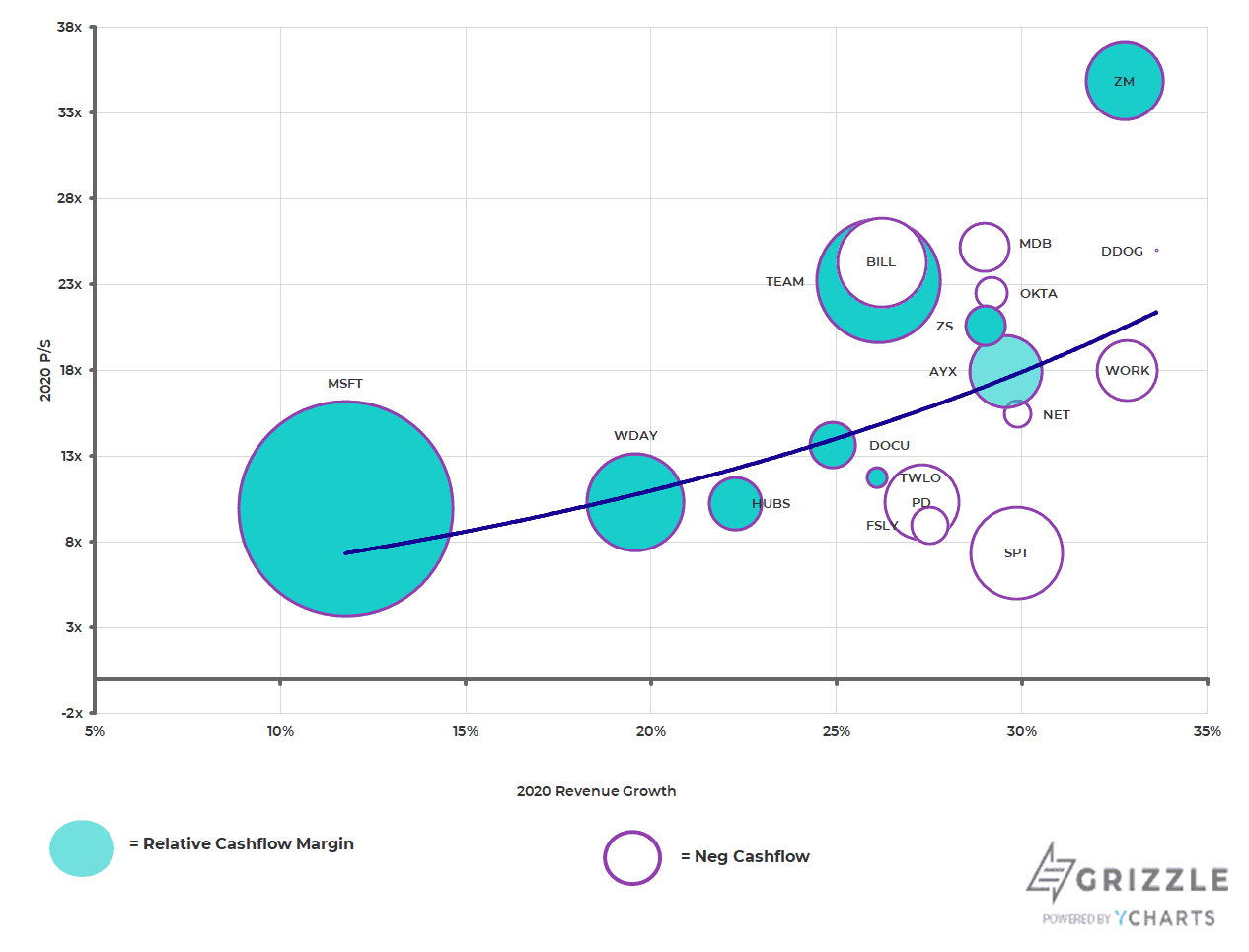

Fastly looks like a steal at only a 9x multiple of next year’s sales, a 50% discount to the group.

The company is growing revenue 35% a year, but the growth in underlying enterprise customers is an anemic 5%.

The market has made it clear it needs to see profits if the company isn’t able to match peers on growth before giving the company a multiple in line with everyone else.

Investors should look for better than expected EPS or faster customer growth as the catalyst this stocks needs to perform better than other software-focused peers.

2020 Price to Sales Multiples for the SaaS Group (Software as a Service)

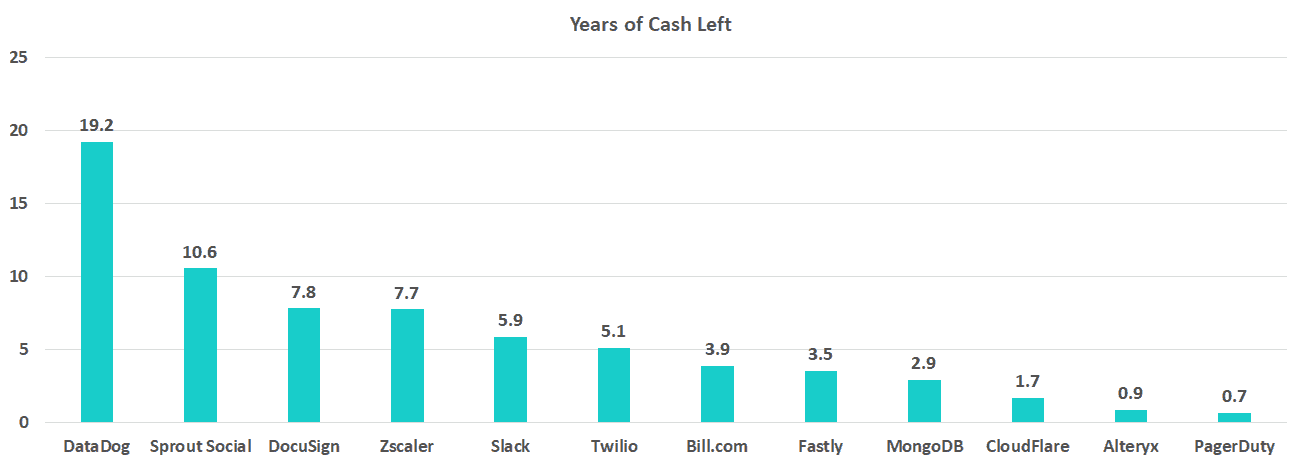

The company has 3.5 years of cash left which is not a huge runway considering the magnitude of losses.

The liquidity and losses coupled with the discounted multiple of sales tells us investors think there is a risk, however small, that Fastly won’t break even before the cash runs low and they have to come back to the market with hat in hand.

Years of Cash Left at Current Spending Rate

Buy Fastly if it Falls Below $20

Fastly is already a cheap stock, but if the stock falls below $20 per share, like it did in August, the stock becomes far too cheap to ignore in our opinion.

At that level all of the risk around liquidity, profitability and growth is well priced in and there could be room for a surprise on the upside.

This is a solid stock with a solid business model that has fallen out of favor with investors.

Without a catalyst, it will stay cheap, but if the price falls far enough we think the possibility of a turnaround outweighs the risks of slowing growth and big losses.

Fastly remains a stock to keep on the watch list.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.