FedEx reported its fourth quarter fiscal 2020 results ended in May post market today that exceeded analyst expectations, causing its shares to trade higher after hours.

The company generated $17.4B of revenue, above analyst estimate of $16.54B by 5%, but was down by 2% year over year.

Earnings per share was $2.53, which beat consensus estimate of $1.6 by an impressive margin of 56%.

The company’s EBITDA however was $752M, which was lower than the street estimate by 47%, due to reasons that will be further discussed in detail subsequently.

Operational Overview

The loss in commercial sales volumes due to business closures internationally, were mostly negated by the company experiencing peak level e-commerce residential deliveries in the US.

This allowed the company to see its FedEx Ground revenue increase by 20% year over year, revenue per shipment at FedEx Freight to rise as well, while fuel expenses decreased by 45% year over year.

In regards to the EBITDA miss however, it was largely due to asset impairment charges related to FedEx Office, which totalled approximately $370 million due store closures.

Additionally pre-tax noncash mark-to-market (MTM) retirement plan accounting adjustment of a net $794 million loss also helped lower the EBITDA too.

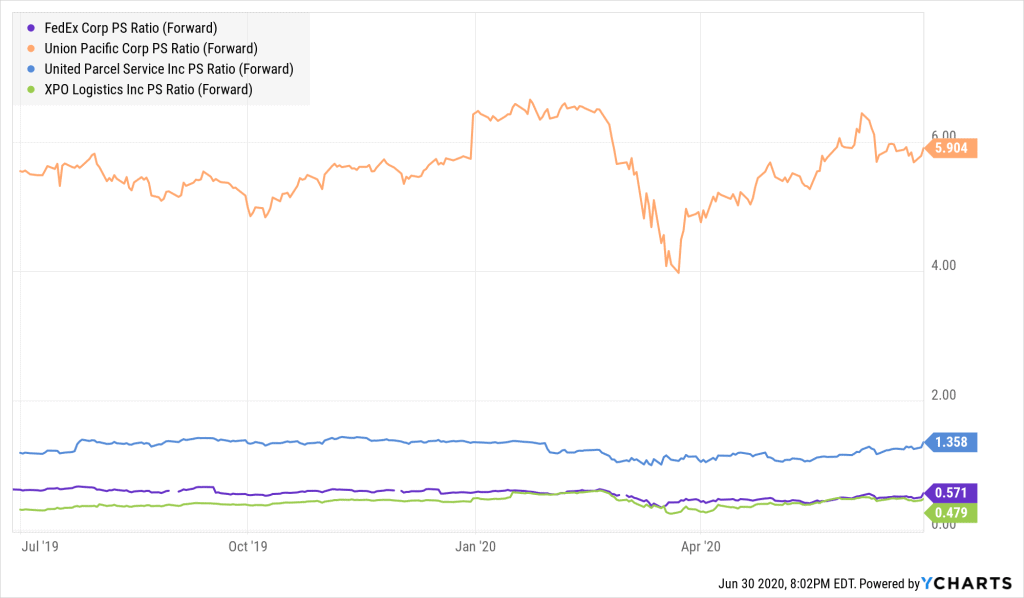

Valuation Analysis

FedEx’s share price is largely traded on par with the company’s book value, compared to the premium enjoyed by Union Pacific Corp’s (UNP) share price.

This is mainly due to the fact that UNP’s operational structure is more efficient than that of FedEx.

For instance, according to UNP’s pre pandemic earnings release for the quarter ended on March, and FedEx’s earnings release for the quarter ended on February, UNP’s EBITDA margin was higher by 43.96%.

Additionally, even though the company had much more debt in that quarter compared to FedEx, its debt to EBITDA ratio was more favourable at 10.2x compared to FedEx’s ratio of 12.5x.

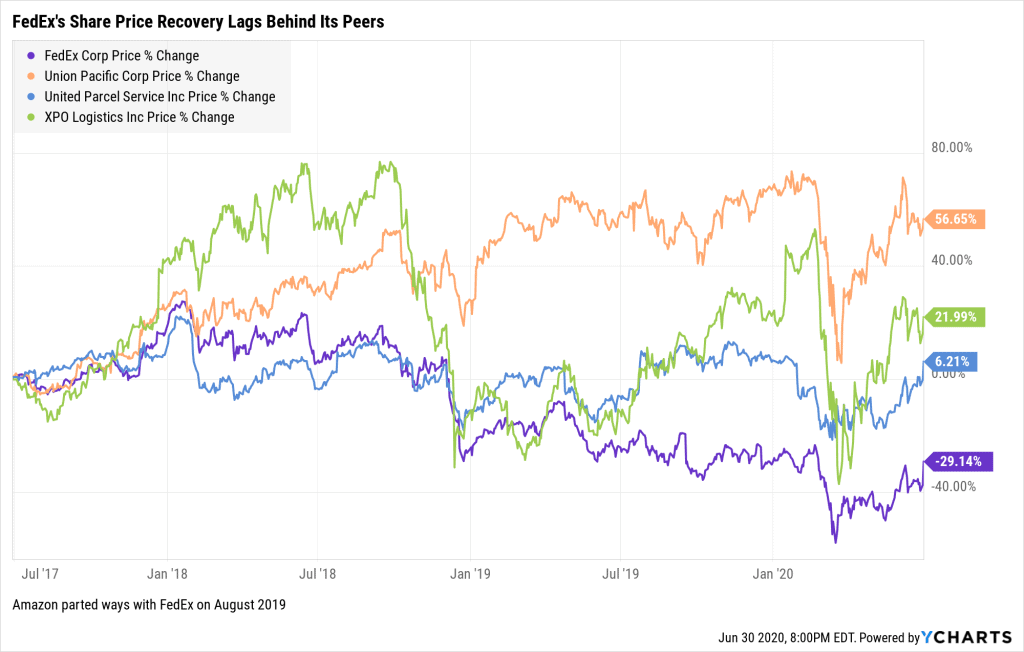

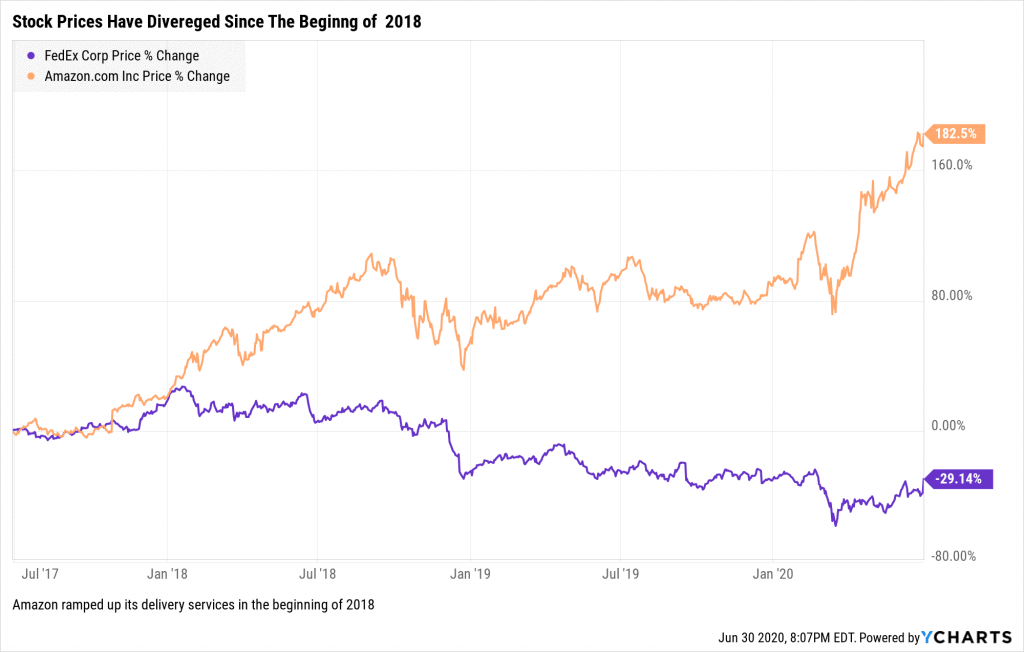

Ever since Amazon kicked started its own delivery services into full gear in 2018, traditional delivery focused companies have seen a drop in its share value, especially FedEx.

As Amazon grows its user base, it certainly takes away market share from companies like FedEx due to its advancing and efficient delivery methods.

Additionally while the world sees a surge in home delivery, FedEx still falls behind Amazon in meeting this demand. This was one of the key factors that led Amazon to part ways with FedEx in 2019.

However, FedEx has taken steps to counter the growing influence of Amazon since then like establishing relations with Walmart to meet their delivery needs for their competitive e commerce business.

Outlook

The management did not provide and future operational guidance, but FedEx’s CEO & Chairman, Frederick W. Smith, expressed confidence by stating that “As a result of the strategic investments we have made to enhance our capabilities and efficiencies, FedEx is well positioned to support and benefit from the reopening of the global economy.”

On the other hand, although countering Amazon’s presence will be a difficult task, the surprise revenue beat and particularly the growth in its FedEx Ground segment in the midst of the pandemic proves that the company is improving in meeting the growing demand of home delivery.

Therefore, we believe that FedEx could regain its lost market share if it continues to adapt to the rising volumes of e-commerce sales. Its ties with Walmart and its positive performance thus far, further favour this outlook.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.