The US Treasury bond market has started to sell-off in recent weeks, in line with the base case here of a steepening yield curve as a result of a post-lockdown cyclical recovery.

The 10-year Treasury bond yield has risen from a recent low of 50bp on 6 August to 67bp.

US 10-year Treasury Bond Yield

Still the bond market action has been less violent than might otherwise have been the case because of widespread expectations, subsequently fulfilled, that the conclusion of the Federal Reserve’s 18-month-long strategic review would culminate in the formal softening of the inflation target.

As a result of Fed chairman Powell’s speech at the virtual Jackson Hole conference late last month, the American central bank has now formally given itself the licence to overshoot its 2% inflation target, potentially by the amount commensurate with the amount it has undershot in the past.

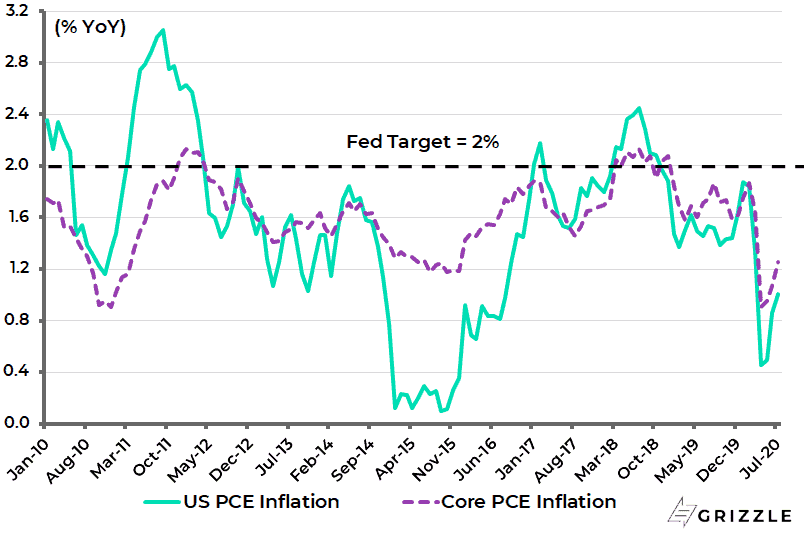

PCE inflation and core PCE inflation, the Fed’s favorite inflation measures, have been running at an average 1.5% YoY and 1.6% YoY respectively over the past ten years, or 0.5ppt and 0.4ppt below the Fed’s 2% inflation target.

US PCE inflation and core PCE inflation

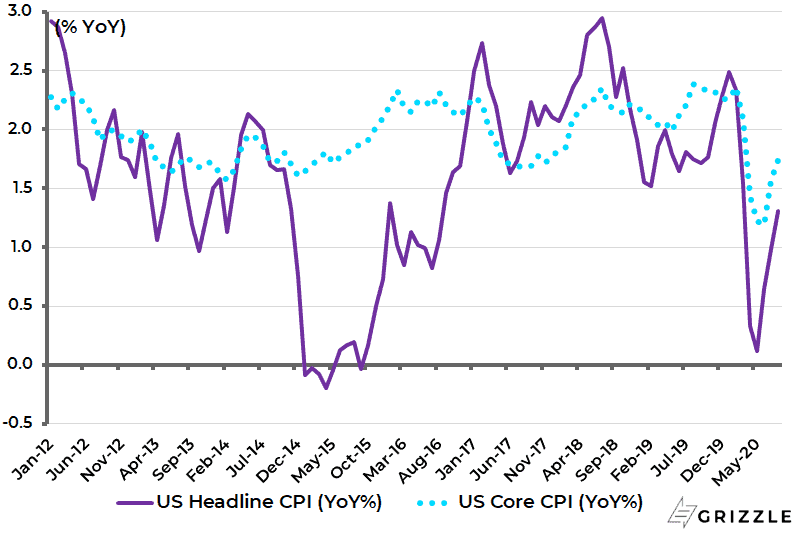

Such a policy helps explain the bond market’s lack of reaction to the July and August US CPI inflation data which surprised on the upside.

US headline CPI and core CPI both rose by 0.6% MoM in July and 0.4% MoM in August, and were up 1.0% YoY and 1.6% YoY, respectively, in July and 1.3% YoY and 1.7% YoY in August.

This compares with 0.6% YoY and 1.2% YoY in June.

US Headline and Core CPI inflation

Meanwhile, another explanation for the lack of volatility in the bond market is the by now widespread assumption, shared also by this writer, that some form of yield curve control in America is coming sooner or later.

This view is maintained despite the release of the Fed minutes last month for the late July FOMC meeting which stated that “many” participants do not favour such a move at this juncture.

In this respect, it will likely take a further pickup in long term bond yields to trigger yield curve control.

Still this is not the end of the Fed’s monetary policy initiatives.

There has also been talk that the Fed might commit at the next FOMC meeting this coming week to more “forward guidance” by stating specifically that the Fed will not raise interest rates or end open-ended quanto easing until inflation and unemployment have reached some specified levels.

Meanwhile, a Democratic victory in the forthcoming presidential election, and a related Democrat takeover of Congress, will see pressure from the activist side of the party to embrace more formally policies aligned with Modern Monetary Theory (MMT).

Such policies, if implemented, would turn the Fed into an instrument of fiscal policy obliterating any lingering sense of central bank independence.

This is because the pressure on the central bank to monetise deficits would become explicit rather than, as is now the case, implicit.

Meanwhile the state of the US economy is the reason why the base case here is that the yield curve should continue to steepen as, cyclically, conditions continue to improve.

True, the continuing failure to agree a bipartisan deal in Washington has raised the threat of the so-called “fiscal cliff”, in the sense that some of the unemployed are now only getting US$333 a week, and in some cases will have to wait another week or more before receiving the increased benefit resulting from Donald Trump’s presidential decree on 8 August.

This will lead to a weekly payment of US$633, down from US$933 before the end of July but still well above the pre-Covid level of US$385. So far 25 states have started paying the extra benefits.

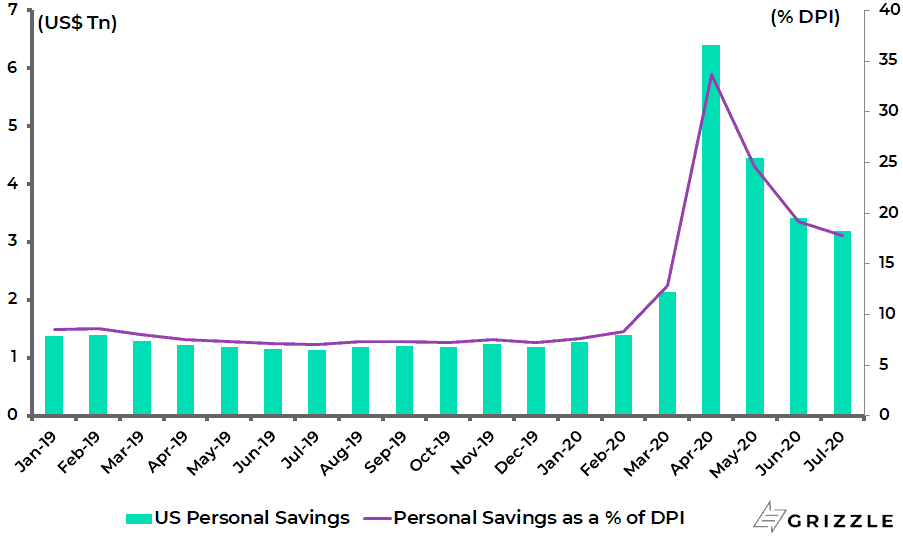

Still there is more resilience in the system than often appreciated because of the increase in household savings which is still well above pre-Covid levels.

US personal savings surged from an annualised US$1.27tn or 7.6% of disposable income in January to US$6.40tn or 33.7% of disposable income in April and were still US$3.19tn or 17.8% of disposable income in July.

US personal savings rate as % of disposable income

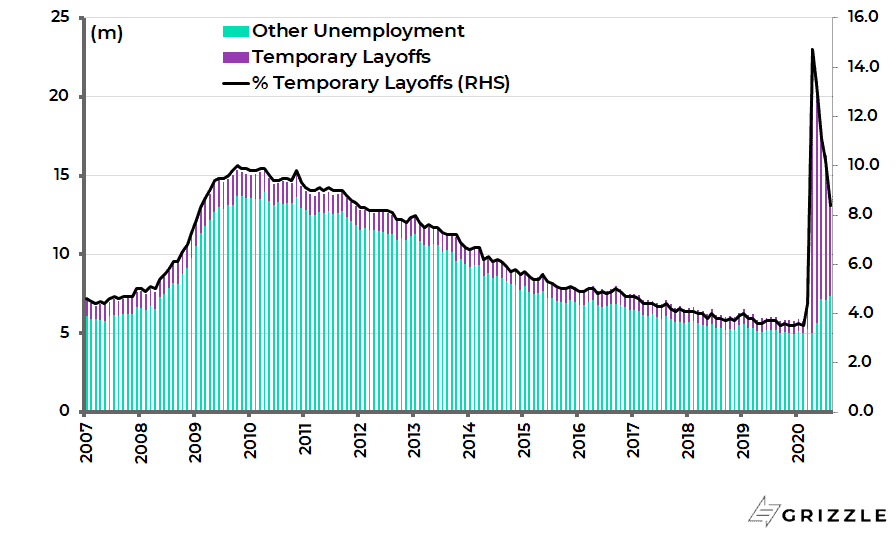

It is also the case that there remains considerable scope for the unemployment rate to fall sharply if the temporary unemployed are re-hired in line with the incentives provided by the Paycheck Protection Program (PPP).

Unemployed persons on temporary layoffs, measured as those who have been offered to return to work or are expected to be recalled to their job within six months, surged from 801,000 in February to 18.1m in April.

That number has since declined to 6.2m in August and now accounts for 45% of the total 13.55m who are unemployed, though down from 78% of the 23.1m unemployed in April.

If the number of such temporary laid off workers declines further to the pre-Covid level of 801,000, the unemployment rate would fall to only 5.1%, compared with the reported 8.4% in August and a peak of 14.7% in April.

US unemployment breakdown

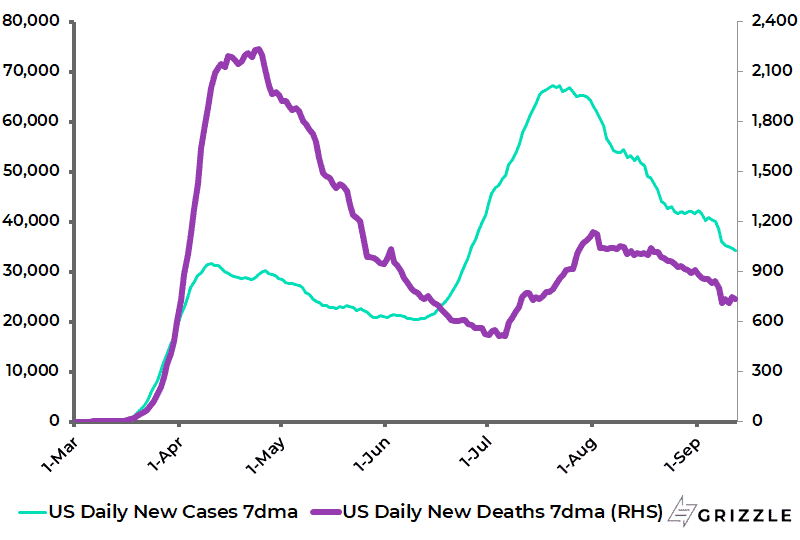

The other point, of course, is that the Covid-19 daily case data in America continues to decline and is now down 49% from the peak reached on 22 July.

While daily deaths remain 35% below the recent high reached on 1 August

US Covid-19 7-day Average Daily New Cases and Deaths

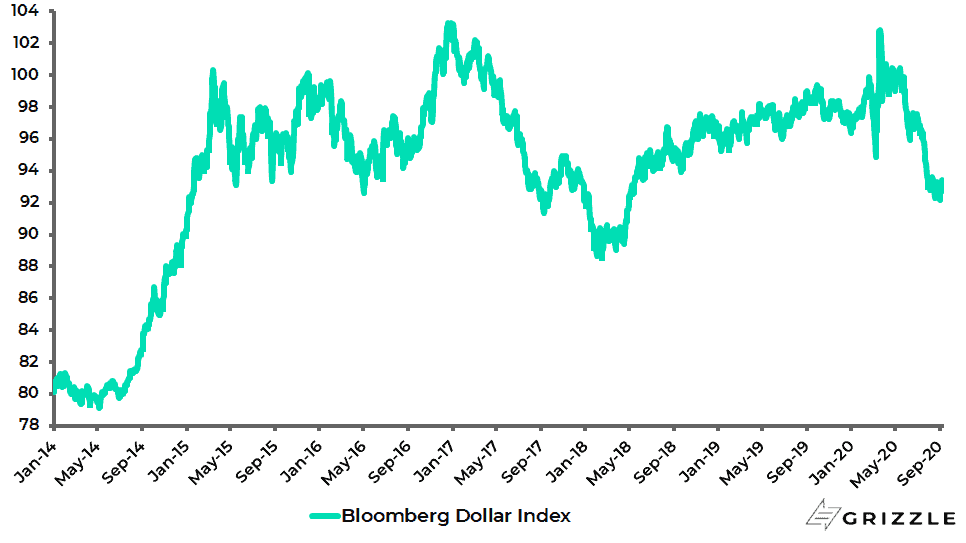

Meanwhile the US dollar has remained weak, and increasingly looks like it has peaked.

The US Dollar Index has declined by 9.4% since peaking on 23 March.

US Dollar Index

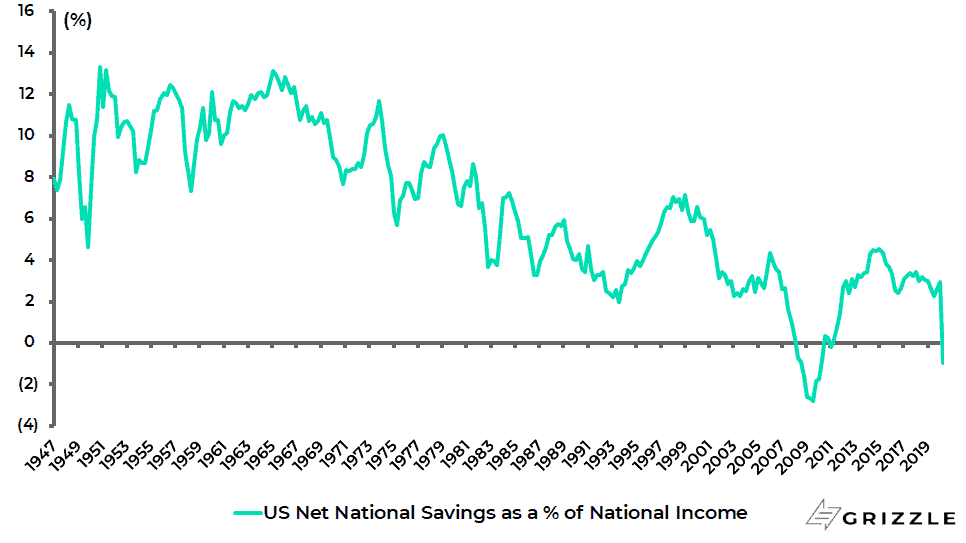

One way of viewing renewed dollar weakness is the declining trend in America’s net national savings; measured as the sum of savings by businesses, households and the government sector, adjusted for depreciation.

This is despite the lockdown-triggered rise in the household savings rate mentioned earlier.

Thus, US net national savings has declined from 4.5% of national income in 1Q15 to 2.9% in 1Q20 and a negative 1.0% in 2Q20.

This compares with the average of 7.6% in the period between 1947 and 2006 prior to the global financial crisis.

US Net National Savings as % of Nation Income

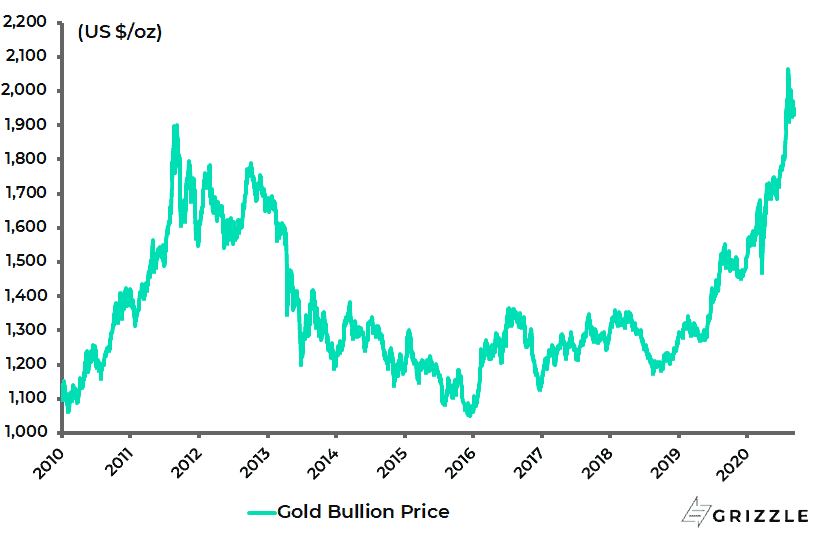

Gold the Beneficiary of the Structural Weak US Dollar

What increasingly looks like a structurally weak dollar is one more reason to like gold.

This writer remains positive on gold and silver, and indeed bitcoin.

Still, there is one obvious near-term risk to gold.

That is that further yield curve steepening, in line with growing evidence of US cyclical momentum, should be negative for gold and should result in more of a correction.

That is, of course, unless the market is convinced, as already discussed, that the Fed is going to remain dovish whatever the data.

For this raises the possibility that gold simply looks through such yield curve steepening.

In this respect, it is also worth mentioning that Powell formally ditched belief in the Phillips Curve in his virtual Jackson Hole speech.

That means the Fed will no longer view a tightened labour market as a reason to tighten monetary policy.

Gold Bullion Price

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.