Back on December 17th, we wrote an article questioning Fire and Flowers’ ability to pay off upcoming debt maturities.

At the time the company had $43 million of cash against $47 million of debt due in the summer of 2020.

They also were generating losses of $5 million a quarter due to construction costs for new dispensaries and on other growth initiatives.

Back then the stock was trading at $0.90/sh.

Since our article was written, management converted some of the debt to new shares, as we warned, driving the price to an all-time low of $0.32/sh in March.

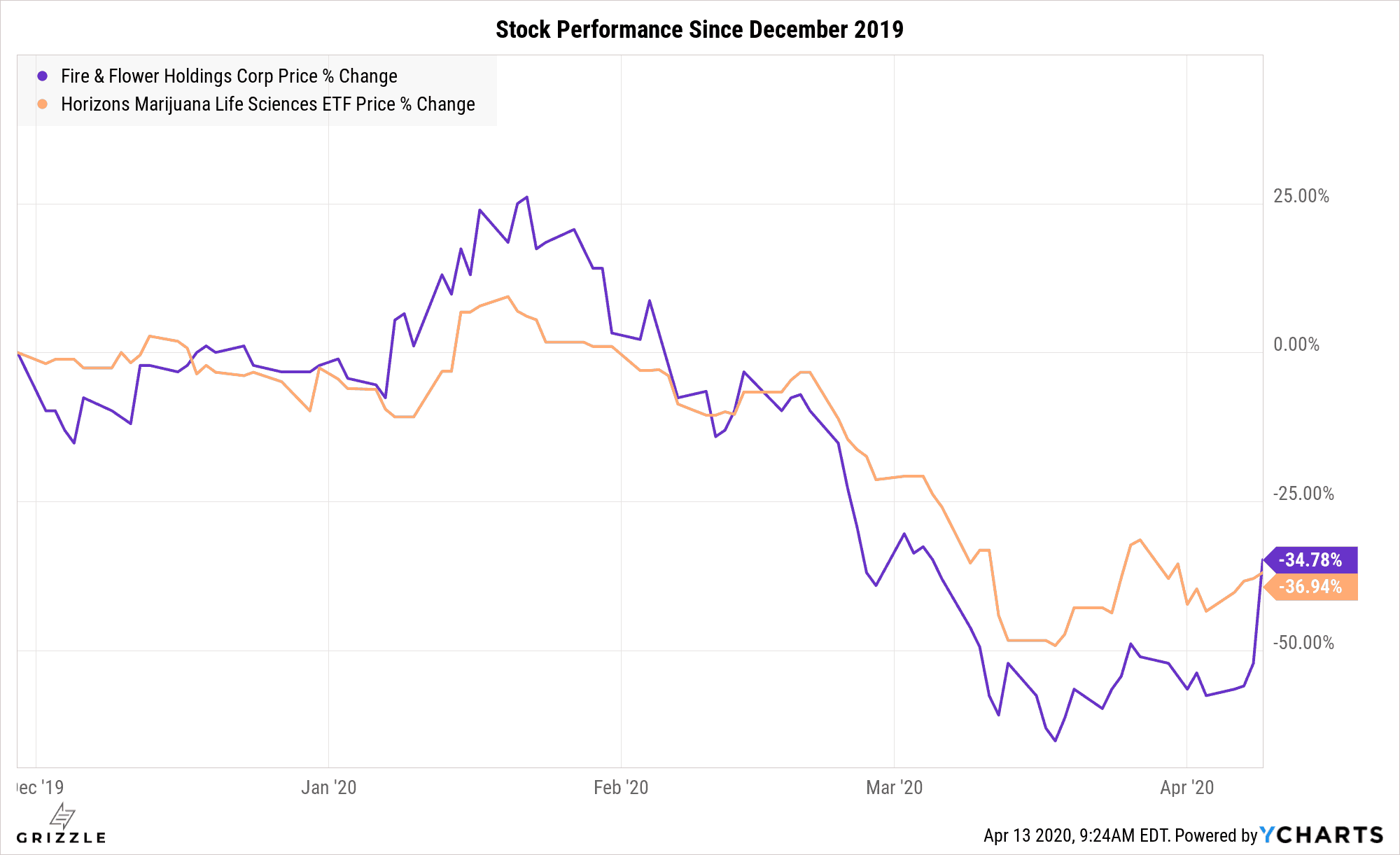

F&F Underperformed the Cannabis Sector Until Recent Spike

The stock has rebounded somewhat since, but with the news today that Fire & Flower is raising another $25 million through convertible debt that may one day increase the share count, investors are likely wondering when this company will stop diluting everyone’s ownership stake.

Cannabis Companies are Built for Corporate Success, Not Your Success

There is a fundamental truth we’ve come to realize about most potstocks.

They operate on a business model of growth at all costs.

If you have to lose money to become the biggest player in the sector, its worth it, nomatter how many millions of shares you need to issue to do it.

At first, we wondered why management teams would be willing to dilute their ownership stake in the business to almost nothing, but then we remembered their high salaries and new lower-priced options they are issuing to themselves quarter after quarter.

This growth at all costs mentality comes at the expense of anyone who owns a share of stock.

Management may be growing revenue and hoping the profits will follow, but your share is entitled to less and less of the business until it is worth only a fraction of where you bought it even though the company is twice or three times as large as it used to be.

This is the negative power of dilution.

[su_panel]Investors should be sitting on the sidelines waiting until their favorite cannabis company can turn a profit and stops issuing more and more shares. That will be the point when you have a chance of actually making some money.[/su_panel]Is Fire and Flower Done Diluting

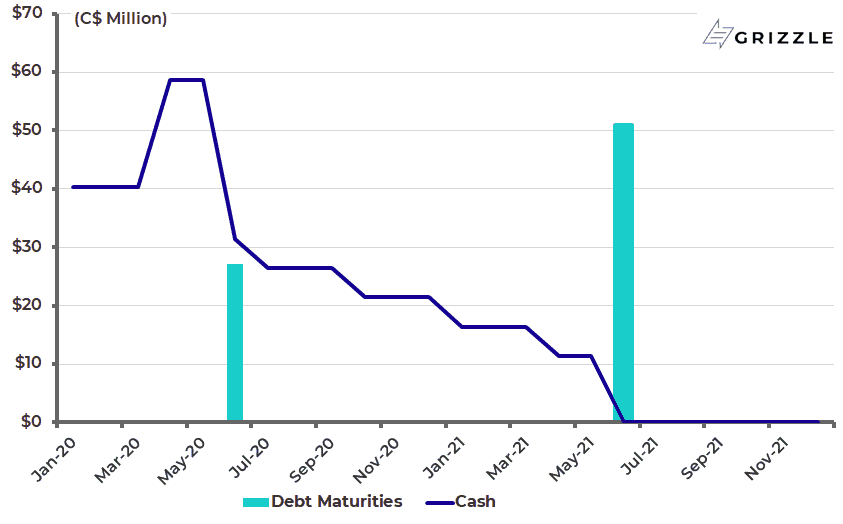

Now that the company is raising an additional $25 million, does that mean they have enough cash to execute their long term strategy?

Unfortunately for current investors, the answer is likely no.

The reason management did this capital raise was because $27.2 million of debt is coming due on June 26th and management did not believe they had enough cash to comfortably pay off the debt.

Here is a simple explanation of what this debt raise means for the company.

- They are replacing 8% interest non-secured debt with 8% interest secured debt due in a little more than a year.

- The new debt converts into shares at $0.50 compared to the old debt which converted at $1.20.

- The new debt will increase the share count by 33% if the stock trades above $0.50, compared to the old debt which would have increased the share count by only 15%.

- The debt will continue to cost them around $2 million a year in interest cost, almost 8% of gross profit.

Estimated Cash Balance vs Debt Due

The prudent move as an investor is to sit on the sidelines until 1 of 2 catalysts take place:

- Management finishes issuing shares to fund growth and has a clear path to profitability

- The stock price increases to $2.00/sh or above leading Couche-Tard to exercise their millions of warrants, leaving Fire and Flower flush with cash and ready for expansion.

Until investors see one of these catalysts play out, the only item on the menu is dilution, dilution and more dilution.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.