Fire & Flower (TSE: FAF; OTCQX: FFLWF), a nationwide cannabis dispensary operator, announced that it plans to open 8 additional dispensaries in Ontario this year, on top of two recently purchased locations in Kingston and Ottawa.

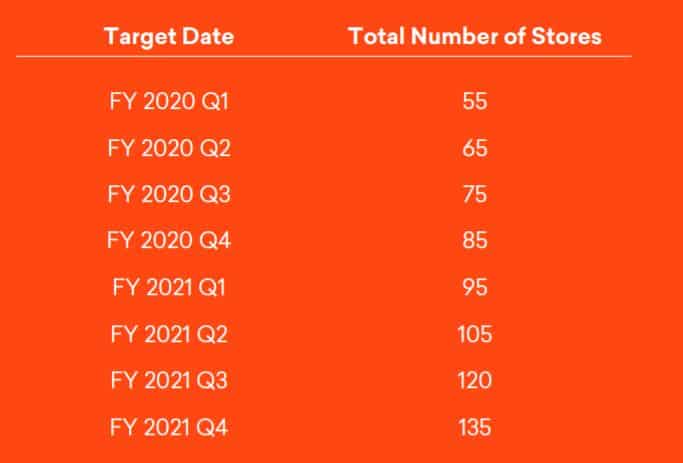

Once these 8 stores are completed, this will bring Fire & Flower’s total store count to 58 across the entirety of Canada.

Fire & Flower acquired the Ottawa and Kingston dispensaries about a month ago and paid with the issuance of 800,000 common shares as well as reserving an additional 933,333 shares upon completion of customary post-closing adjustments.

Around the time of the acquisition, shares of Fire & Flower were trading at about $C0.90 per share, which would value the deal of acquiring the Kingston and Ottawa locations at a combined C$1.56 million approximately.

Based on Fire & Flower’s annualized revenue of C$54.8 million, these two stores should increase the company’s annual revenue by $12 million combined.

As more stores are built, the sales will be distributed throughout more stores, which means that the run rate of $6 million per store will fall.

Expansion is exciting as it implies growing revenue and hopefully profits for the company, but for now, more store capital should raise some concerns for investors.

Can They Afford C$8 Million?

Last December, we reported on a potential cash burn problem at Fire & Flower, and our concerns haven’t yet gone away, even with the February decision to convert a big slug of debt to shares.

Fire and Flower is still spending C$5 million of cash a quarter and the decision to build out additional stores in Ontario may end up increasing losses even further.

Management already has plans to build out 10 stores a quarter which tells us these 8 stores are incremental.

Given management has already been spending about C$1 million to build out each new store, investors should assume the cash burn could be even higher in 2020 than the C$15 million management spent in the last 9 months.

Store Buildout Schedule

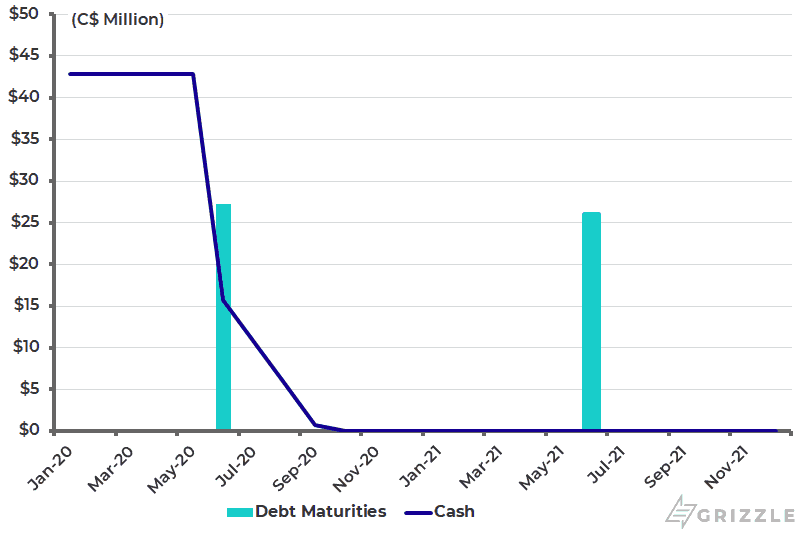

C$8 million of capital presents problems for the company as they are currently burning $5 million of cash and owe at least C$36 million of debt in June and July 2020.

The company is unlikely to show a profit next quarter, which tells us they will likely convert the debt into more shares when it comes due or borrow from the markets to pay off the debt.

Either outcome will continue to put downward pressure on the stock price.

DEBT MATURITY SCHEDULE AND FUTURE CASH BALANCE

With this planned expansion, Fire & Flower will heavily increase their presence in Ontario, Canada’s most populous province, and hopefully allow the company to break into this huge new market.

However, cash burn remains a problem for the company and investors should wait until management is able to raise at least a year of cash or get close to breakeven — both of these conditions Fire & Flower has not been able to meet.

Current shareholders should expect further share dilution as the company may be forced to issue more new shares to cover the cash burn.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.