There have been interesting developments of late in the Eurozone. These have raised expectations of even more dovish monetary policy as well as renewed hopes of more fiscal activism. First, Italy was given a break by Brussels in early July in terms of meeting its fiscal targets. The European Commission concluded on July 3 that “an Excessive Deficit Procedure is no longer warranted for Italy at this stage”.

The motivation of Brussels seems to have been to reduce the temptation for Italian Interior Minister Matteo Salvini to call a general election in Italy where he could campaign against fiscal austerity imposed by Brussels and Berlin. Salvini, as head of The League, continues to be well ahead in the opinion polls.

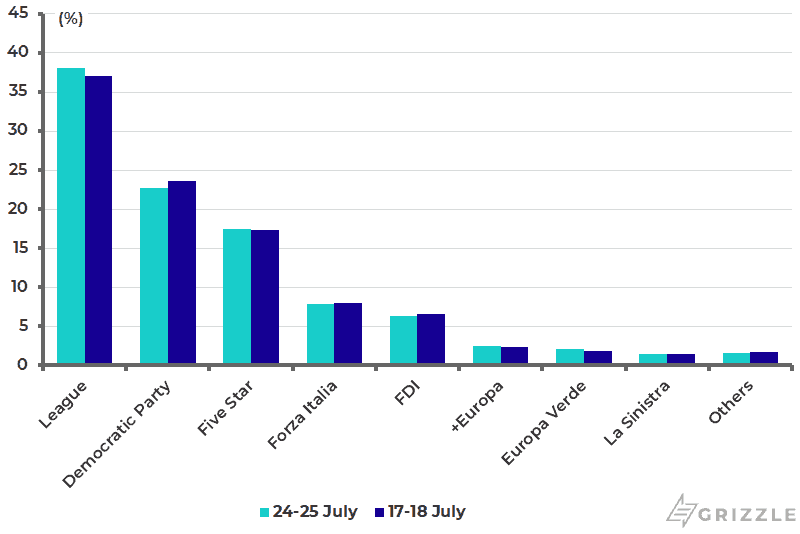

The latest poll conducted on July 24-25 shows that the League has a 38.1% support rating, compared with 22.7% for the Democratic Party and only 17.5% for the League’s coalition partner, the Five Star Movement (see following chart).

Italian Opinion Polls

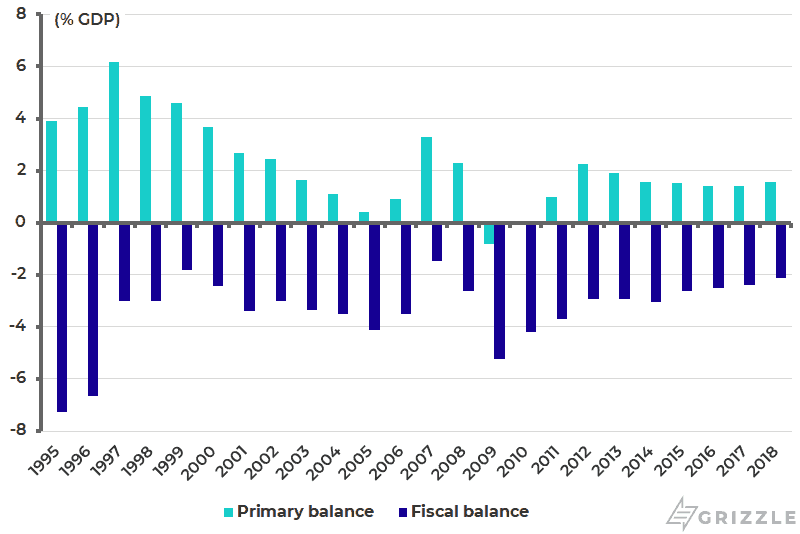

It is also the case that with France breaking its fiscal limits under Maastricht Treaty rules and with Italy still running a fiscal primary surplus (see following chart), the case to single out Italy for fiscal lapses hardly looks watertight.

Italy Fiscal Balance and Primary Balance

Will the Eurozone Push Towards Greater Fiscal Integration?

The other interesting development earlier this month was the announcement that former French finance minister and IMF Director for the past eight years, Christine Lagarde, is the official candidate to replace Mario Draghi as President of the ECB from Nov. 1. This is both a surprising appointment and, potentially, an extremely interesting one.

First, it overtly politicizes the ECB even more than Draghi has done. Second, it raises the prospect that Lagarde will be an ally in openly supporting French President Emmanuel Macron’s longstanding push to move the Eurozone towards greater fiscal integration. This probably means more fiscal stimulus in the Eurozone on the longstanding Draghi argument that fiscal policy should do more “heavy lifting”. It also means, more importantly, making a coherent case for moving further in the direction of fiscal union, which ultimately means a Eurozone-wide “risk free” government bond, or “Eurobond”, which, if it ever happened, would put the ECB on the same footing as the Federal Reserve or the Bank of Japan.

Obviously, such moves will encounter the traditional German opposition against “bailout unions”. But with German politics becoming ever less stable, in terms of the current CDU-SPD coalition looking ever more wobbly, the reality is that the political position of Macron looks much more secure on a relative basis than Angela Merkel’s. After all, he is still in power for the next three years, even if he is not as well positioned in the opinion polls as Italy’s Salvini. It is also the case that the growing possibility that the Greens could enter the federal government in Berlin would soften significantly the traditional German stance against fiscal union, or what the German political right calls “bailout” union. This is because the Greens, who have currently a 24% support rating in Germany, are in favour of Eurobonds.

A Macron-Lagarde alliance could, therefore, lead to a potentially radical change in Eurozone monetary and fiscal policy; though it should be noted Lagarde’s appointment has to be confirmed by the European Parliament in October. The ECB’s Governing Council last week signed off on Lagarde as Draghi’s successor.

What Effect Would Fiscal Integration Have on European Bank Stocks?

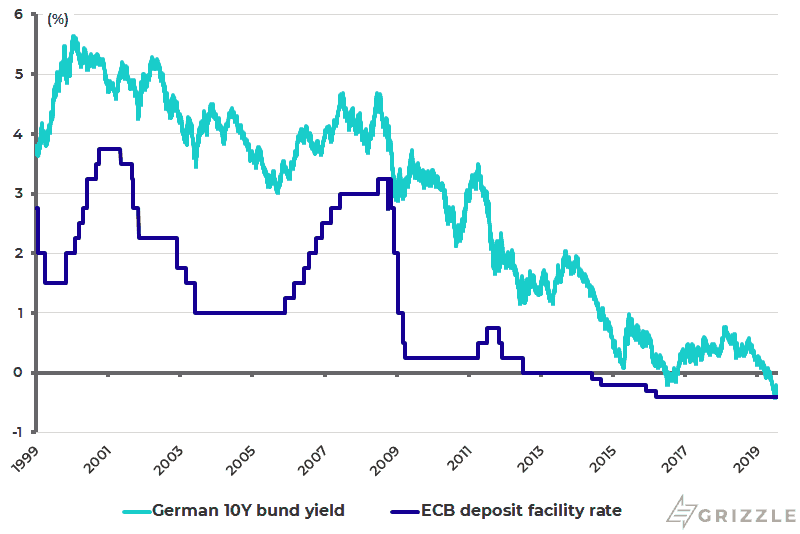

What about Italian bank stocks, or indeed European bank stocks in general? The above developments could be a positive. This is because if there is a real move towards fiscal union it would imply higher German interest rates as well as lower Italian rates (i.e. they meet in the middle). This would be potentially good news for banks and also raises the potential for a stronger euro. Hopefully, Madame Lagarde also understands that even more negative rates is the last thing the Eurozone, and its banks, need. But that may be too optimistic. The current short-term rate in the Eurozone is minus 0.4% while the 10-year German bund yield is minus 0.38% (see following chart).

German 10-year Bund Yield and ECB Deposit Facility Rate

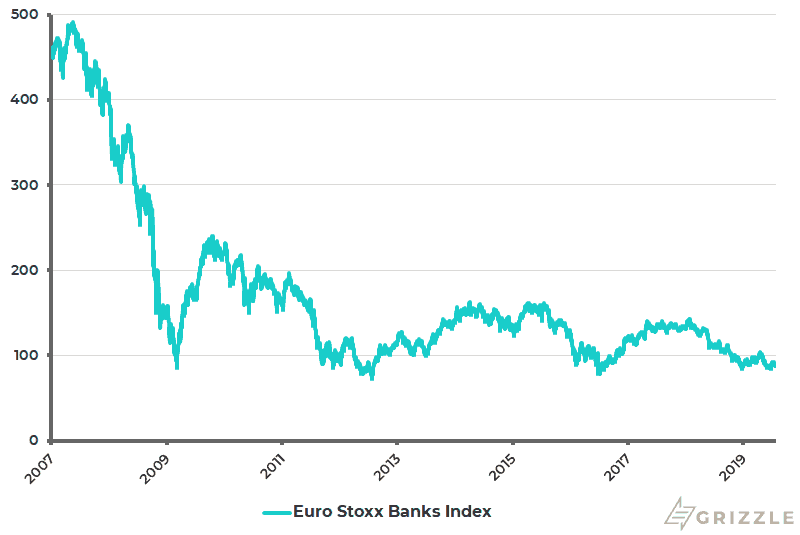

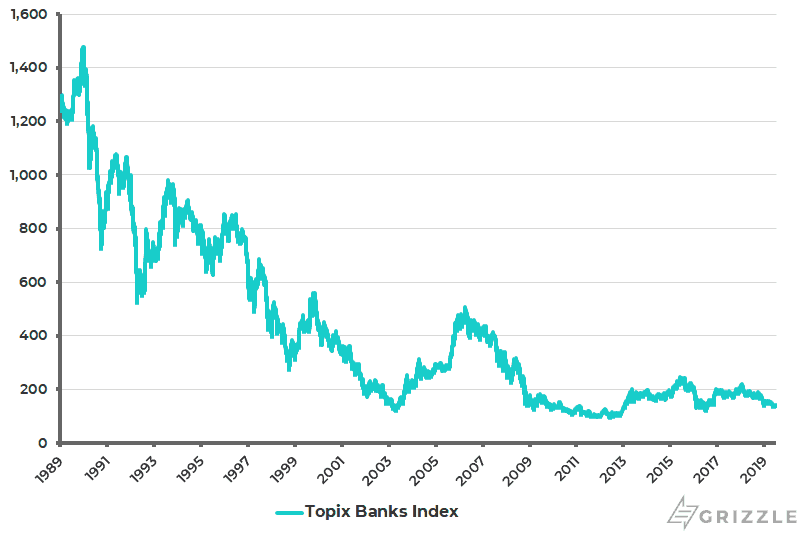

So the potential for fiscal union offers potential relief from the Japanification-of-the-Eurozone banking system story, the risk of which can be seen below in terms of the chart of Eurozone bank stocks since they peaked in May 2007. Compare this with the other chart below of Japanese bank stocks since they peaked at the end of 1989 at the peak of Japan’s Bubble Economy.

Euro Stoxx Banks Index

Topix Banks Index

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.