Although technology stocks aren’t known for their dividend prowess, there are several companies that pay above-average yields. We’ve tracked down five tech sector players with attractive yields and other value metrics that are worth considering. You can see a quick summary in the chart below (values were calculated as of the time of this writing).

Microsoft Inc. (NASDAQ: MSFT)

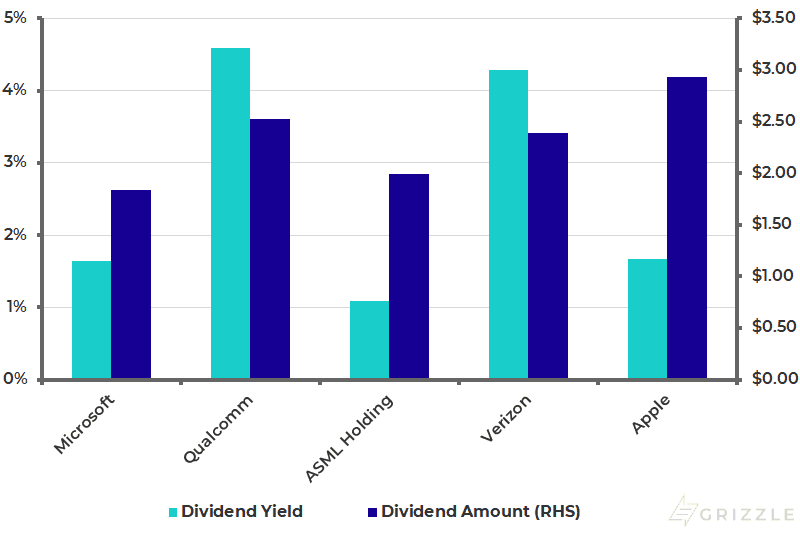

- Dividend Yield: 1.64% ($1.84 per share)

- Dividend Growth: 15 years

Last November, Microsoft briefly surpassed Apple and Amazon as Wall Street’s most valuable company – a title it hadn’t held in 15 years. Though short-lived, Microsoft’s market cap superiority reflected the company’s resurgence under the direction of Satya Nadella. The software giant has become a major player in the cloud computing market, with its Azure platform generating massive growth in recent years. For the second straight quarter, Azure’s revenue grew 76%. The company’s “Intelligent Cloud” category as a whole booked $9.4 billion in sales, up 20%.

Microsoft’s dividend yield is much higher than the tech sector average of 0.99%. Double-digit revenue growth, favourable PE ratios relative to its peers and an expanding cloud/blockchain presence make Microsoft a solid opportunity.

Qualcomm Inc. (NASDAQ: QCOM)

- Dividend Yield: 4.59% ($2.53 per share)

- Dividend Growth: 8 years

When it comes to big tech dividends, very few companies measure up to Qualcomm. At 4.59%, Qualcomm’s dividend yield has essentially quadrupled over the past decade. The multinational semiconductor giant distributes roughly two-thirds of its earnings as dividends, guaranteeing high quarterly payouts but likely sacrificing future growth in the process. In its most recent quarter, Qualcomm posted better than expected earnings but said revenues fell short of estimates.

Despite the mixed results, the company issued positive guidance on its fiscal second-quarter, where it expects to earn between $0.65 and $0.75 per share on a revenue range of $4.4 billion to $5.2 billion.

ASML Holding N.V. (NASDAQ: ASML)

- Dividend Yield: 1.09% ($1.99 per share)

- Dividend Growth: 3 years

Investors on the prowl for high growth and above-average yield will find ASML Holdings an attractive bet. The European semiconductor company has grown its dividend for the last three years, including a 50% spike in 2018. Over the past ten years, ASML payouts have increased tenfold. In 2018, AMSL benefited from strong revenue growth, better than expected earnings and a payout ratio of less than 30%.

Combined with rising gross margin and large buyback activity, ASML looks poised to offer greater value in the near term. Share prices have also outperformed the Nasdaq over the past five years.

Verizon Communications (NYSE: VZ)

- Dividend Yield: 4.29% ($2.39 per share)

- Dividend Growth: 12 years

Verizon Communications fell out of favour with some investors last quarter after the company took a $4.6 billion write-down due to its underperforming “Oath” media unit. Still, that wasn’t enough for income investors to turn their back on the telecommunications giant. After all, VZ’s dividend yield is more than four times higher than the technology sector average. Although the company missed analysts’ fourth-quarter revenue target, it posted a 30% surge in adjusted net profits.

Verizon also surprised where it matters most: wireless subscribers. In Q4 alone, the company added 1.2 million wireless net retail postpaid subscribers thanks to a variety of cost-cutting initiatives. The mobile shift to 5G technology – something Verizon has marketed heavily in recent years – will likely play into the company’s hands moving forward.

Apple Inc. (NASDAQ: AAPL)

- Dividend Yield: 1.67% ($2.93 per share)

- Dividend Growth: 6 years

Apple may have admitted it has a big China problem after smartphones sales in the world’s second-largest economy slowed, but there’s no denying its emerging status as a major dividend player. The iPhone maker has grown its dividend in each of the last six years while keeping its payout ratio at less than a quarter of net income. Relative to earnings, Apple’s stock price is inexpensive. It’s even more of a bargain when you strip out the $130 billion in excess cash (doing so reduces the company’s PE ratio to 11.5 from 14.2 presently). Aggressive share buyback plans and continued profitability should lead to higher dividends for the foreseeable future.

While China continues to offer strong headwinds, a reprieve in the form of a new free trade agreement with the United States is likely coming. The Wall Street Journal reported Sunday that a new trade deal looks imminent after both sides made a number of concessions on tariffs and protected industries. That optimism may trickle down to Apple in subsequent quarters.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.