Foot Locker (NYSE:FL) has posted their results for Q4 2019.

Revenue came in at $2.22 billion which slightly missed analysts’ estimates of $2.24 billion and EPS was $1.63 beating analysts’ estimates of $1.58.

The stock has been hammered on Wall Street recently, losing almost half its value since the same time last year. Analysts are getting increasingly concerned about traditional retail stocks and their ability to compete with rising ecommerce players like the giant Amazon and other online retailers. However, the valuation of Foot Locker at these levels is getting interesting. The company also has a decent dividend of just over 4% yield with a payout ratio of just over 30%.

Foot Locker’s Business Is Pretty Easy to Understand

In short, Foot Locker sells shoes. Foot Locker runs a chain of traditional brick-and-mortar locations typically placed in malls and sells popular brands like Nike and Adidas in its stores. Foot Locker also has their own brands, with the most famous one being a brand called Champs.

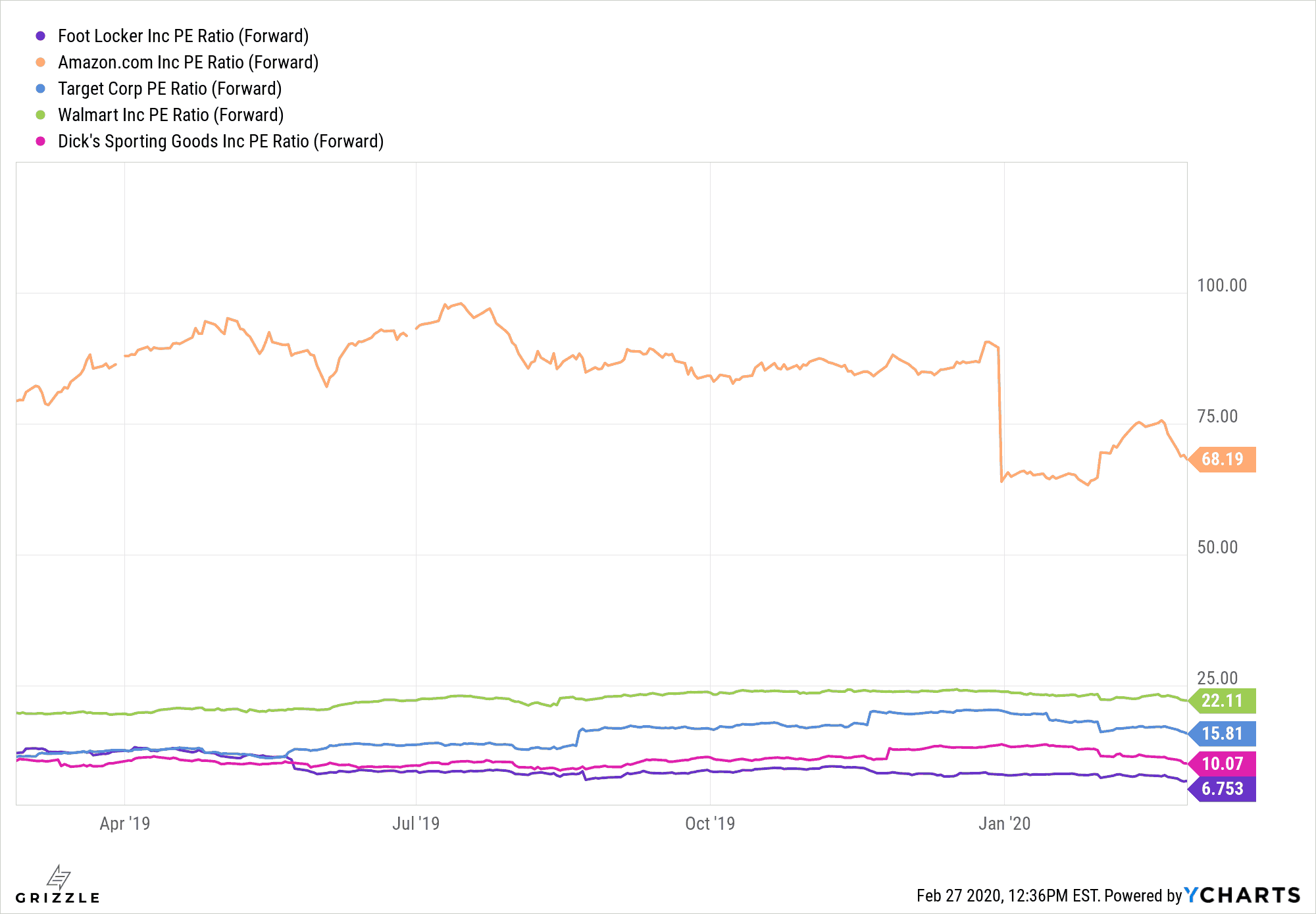

Foot Locker is expected to post very little sales growth (1-2%) in the next 2 years, and that has sent investors flooding into other stocks that offer a bit more growth. Taking a look at the forward P/E, we see that Foot Locker’s forward P/E is extremely low, coming in at under 7.

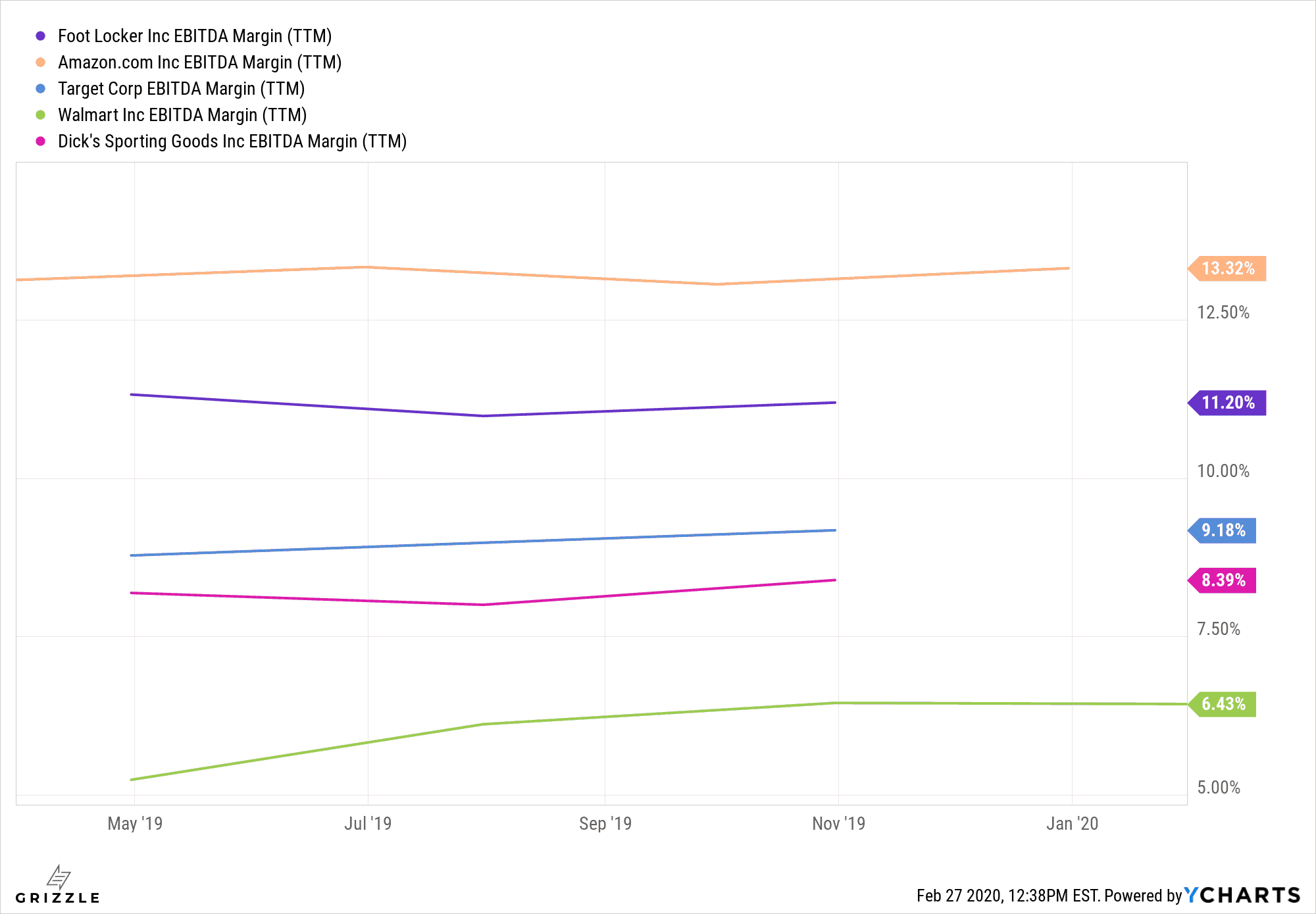

However, despite the low valuation, it seems like the EBITDA margin for Foot Locker is quite good compared to the rest of the industry.

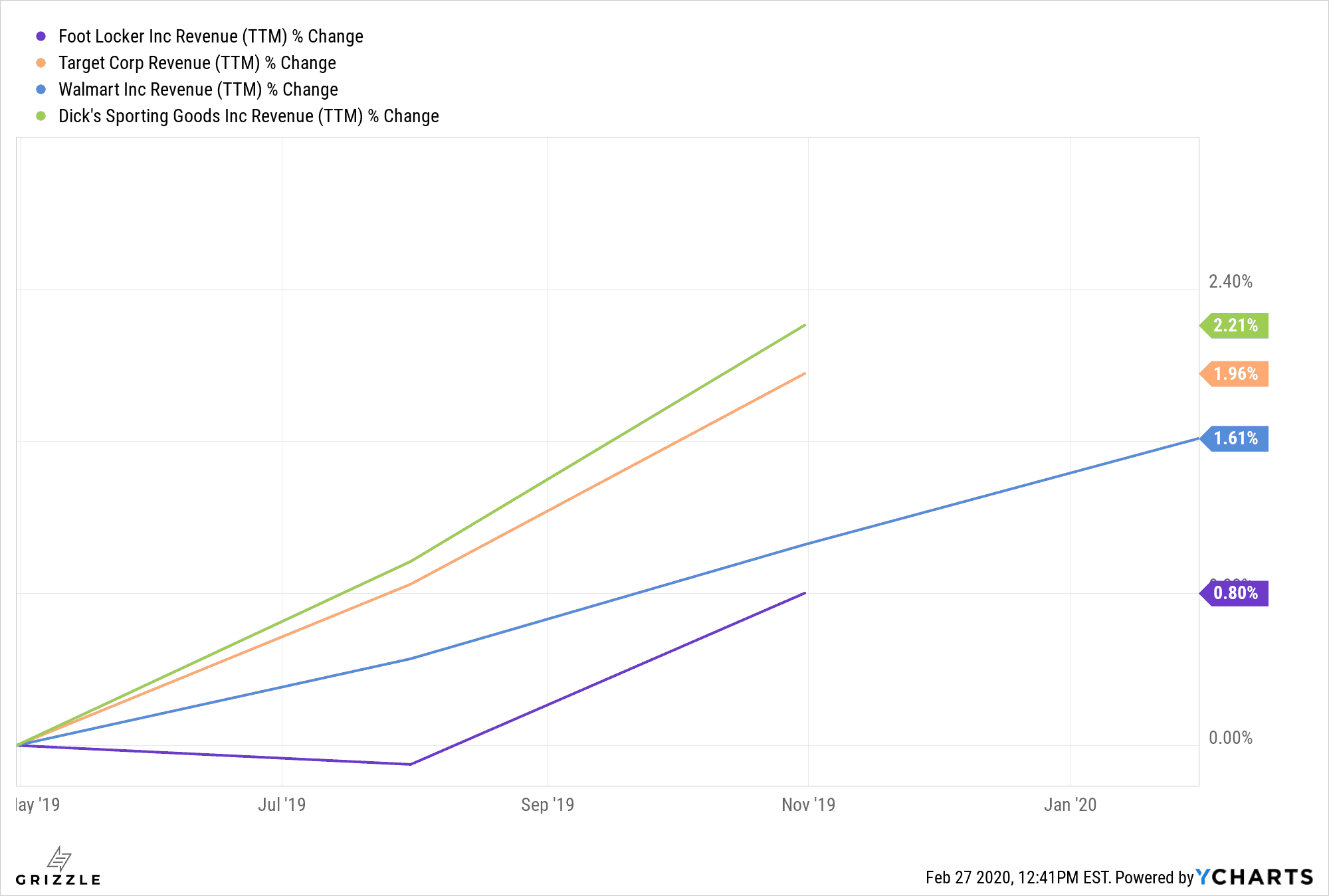

Although revenue growth for Foot Locker is lower than some other retail chains, the difference in growth rate is not that huge. Even factoring in future estimated growth, Foot Locker only lags slightly behind that of Walmart or Target who are expected to grow sales for the next 1 year period at about 2.9% and 3.7% respectively, versus Foot Locker’s 1.1% estimated growth around the same time period.

However, this hardly justified the difference in stock performance between Foot Locker and Target and Walmart. At these levels, Foot Locker seems very undervalued and an intriguing buy. Coupled with a high dividend yield and a low payout ratio, it seems like this stock is a bargain in this richly valued market.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.