It was ironic that, the same week Germany celebrated the 30th anniversary of the fall of the Berlin Wall, the left-wing Berlin city government committed to implementing a socialistic five-year rent freeze from the start of next year. Previously, rents in Berlin, as in the rest of Germany, have been adjusted according to a fixed formula linked to inflation.

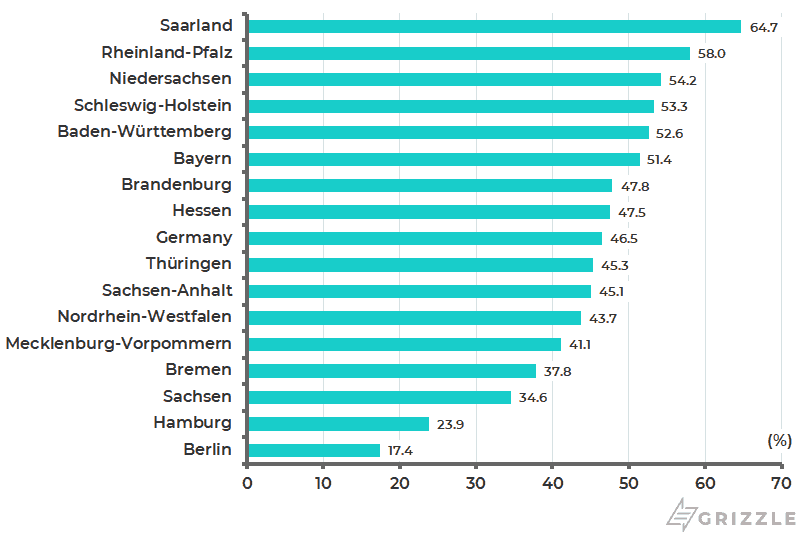

The political appeal of such a policy is clear. While the national home ownership rate in Germany is a relatively low 46%, in relatively poor Berlin it is much lower with 83% of the city’s population renters (see following chart). Still the declared policy has already led to major uncertainty and a freezing of activity.

Freezing Rent Will Only Cause House Prices to Rise

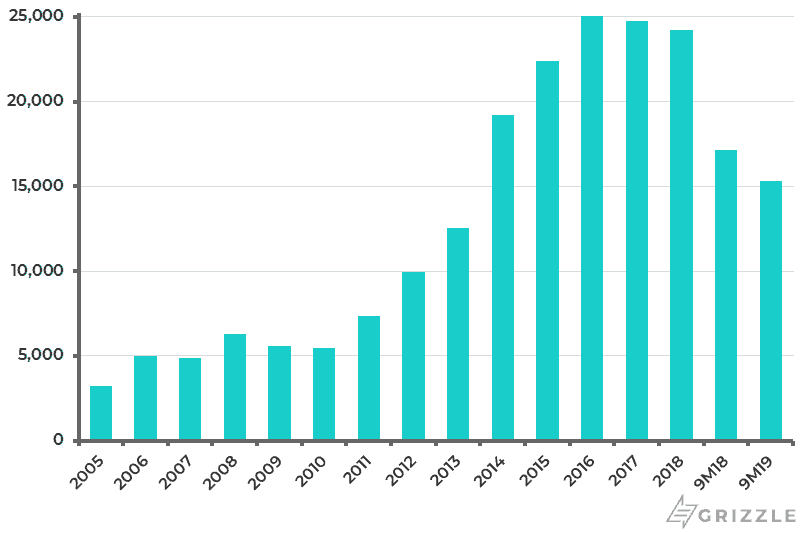

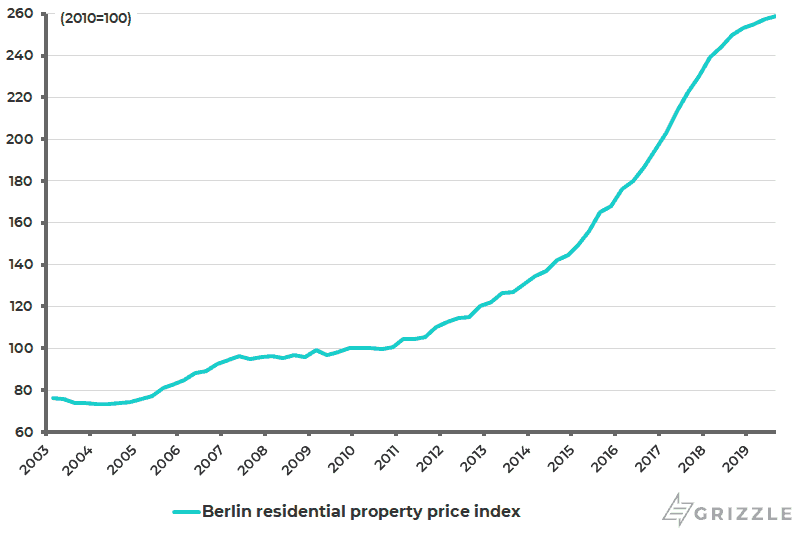

Construction permits are already declining in Berlin after a property boom which has lasted for more than ten years, while developers will now seek to get around the rules by converting existing property into the likes of serviced apartments exempted from the regulation. The number of building permits for apartments in Berlin declined by 10.7% YoY in the first nine months of 2019, having risen by 343% since 2010 (see following chart). The Berlin residential property price index is up by 170% since 2009 (see following chart).

Germany Homeownership Rate (2018)

Berlin Building Permits for Apartments

Berlin Residential Property Price Index

As is always the case, longer term rent controls can only lead to a decline in residential supply which will only further increase the price of property, most particularly as Berlin, unlike most other German cities, has enjoyed rapid population growth in recent years. Berlin’s population has risen by 9.6% from 3.33 million in 2011 to 3.64 million in 2018, while Germany’s total population is up only 3.4% over the same period to 83 million. But it looks like that lesson in the negative self-defeating “boomerang” consequences of price controls will have to be re-learned.

Germany Opinion Polls

Rent Freeze Signals a Shift to the Left

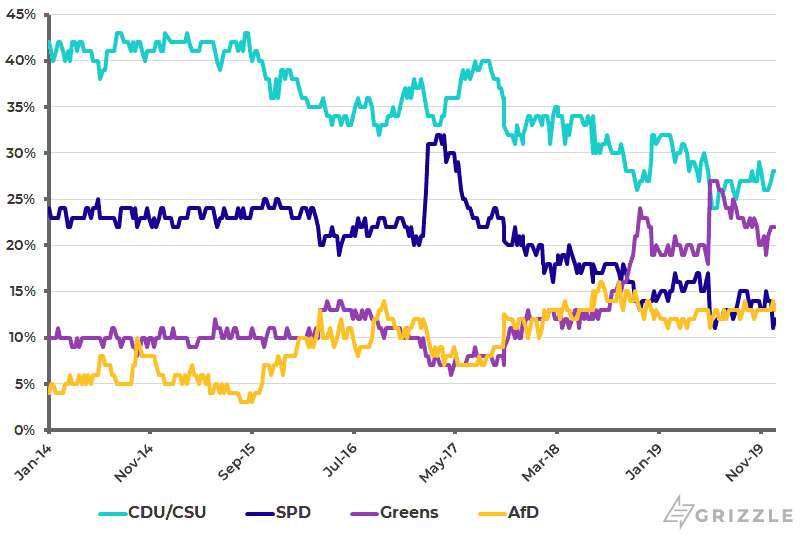

Meanwhile, the proposed rent freeze is a reminder of the potential for German politics to swing to the left. In this respect, the potential remains for a federal election to occur next year if the SPD votes to walk out of the grand coalition with the CDU. This has become more likely with the election of a new more leftist leadership at the SPD’s annual congress this month. This is because the SPD’s support continues to collapse in the polls, falling to 12% at present from 32% in March 2017 (see chart above).

In the most recent state election in late October in Thuringia in the old East Germany, the SPD got only 8.2% of the vote, compared with 12.4% in 2014. Meanwhile on the right the CDU got 21.7% and the anti-immigrant AfD 23.4%. Still it remains the case for now that the AfD is much stronger in the old East Germany than the West. In this respect, it is worth noting that Adolf Hitler was voted into power in 1933 by the Protestants in the East of Germany, not by the Catholics in Bavaria.

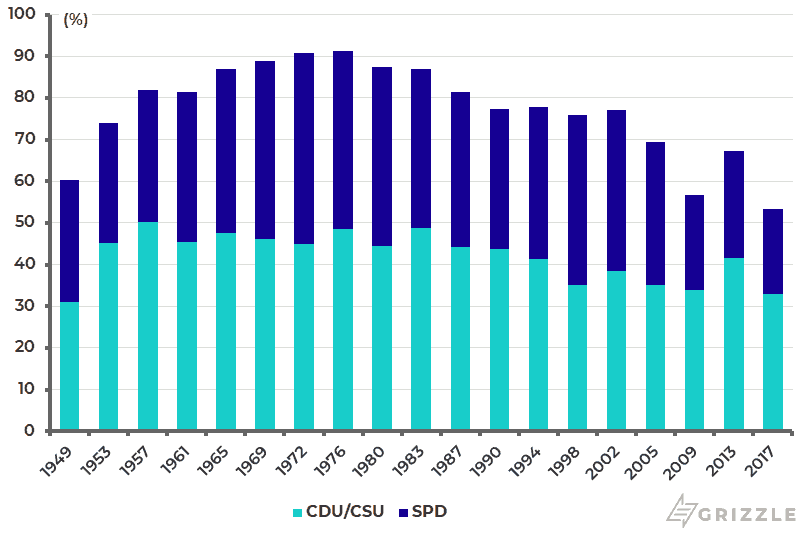

Germany Federal Election Since 1949 (CDU/CSU and SPD votes)

If there is another federal election next year, it is likely to be the first time since 1949 that the CDU/CSU and SPD do not get at least 50% of the vote (see chart above). That could open the way to a potentially left-wing coalition government of the Greens, SPD and Die Linke party, otherwise known as the Melon Coalition (green on the outside, red on the inside), if the Greens and the CDU cannot negotiate a coalition. This is because it remains, for now at least, not socially acceptable for the CDU to contemplate a coalition with the AfD for obvious historical reasons. As noted, SPD is currently polling at only 12% nationally, compared with 22% for the Greens and 28% for the CDU. The AfD is at 13% (see previous chart).

Such a left-wing coalition could, potentially, see the policies towards rents adopted in Berlin extended to other cities in Germany. If all this is a further reminder that German politics is becoming less moderate as the centre weakens, there has also been more evidence that German resistance to greater Eurozone integration is also weakening. One example is an article written by German finance minister, Olaf Scholz, in the Financial Times last month. Scholz wrote that “the need to deepen and complete European banking union is undeniable … an enhanced banking union framework should include some form of common European deposit insurance mechanism” (see Financial Times article: “Germany will consider EU-wide bank deposit reinsurance”, Nov. 6, 2019).

Banking Union, and Possibly Fiscal Union, Looking More Likely

True, Scholz was commenting on a personal basis, not as official policy of the current government. Still the direction of travel seems clear. That said, more concrete progress towards banking union and even fiscal union is more likely to occur in a German federal government in which the Greens are a major player since they remain much more favourably disposed to concepts such as Eurobonds, which imply more “risk sharing” in the Eurozone.

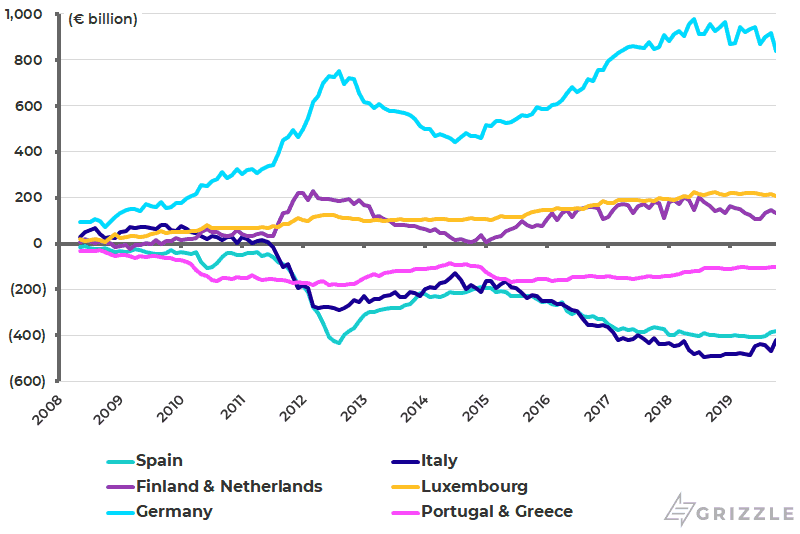

Meanwhile, the way the ECB bond buying has worked, in terms of its quanto easing program, is that it has led to the Eurozone being bound ever closer together financially, albeit in rather an opaque fashion. This can be seen in the so-called rising Target-2 claims of the Bundesbank and the national central banks in the Netherlands, Finland, and Luxembourg, on the rest of the Eurozone.

Thus, Bundesbank’s Target-2 claims have risen from €416 billion at the end of 2014 to €837 billion at the end of October 2019, while the combined claims of the central banks of the Netherlands, Finland, and Luxembourg have risen from €144 billion to €340 billion over the same period. By contrast, the Target-2 liabilities of the Italian and Spanish central banks, for example, have increased from €209 billion and €190 billion, respectively, at the end of 2014 to €420 billion and €379 billion at the end of October (see following chart).

Eurozone Target-2 Balance

These claims would become real money losses if Italy or Spain, or other Eurozone central banks with net liabilities, ever decided to exit the common currency. Meanwhile, a move to common deposit insurance in the Eurozone would go some way to reduce the risk for depositors of so-called bank “bail-ins”, which has been one justification at least for owning negative yielding government bonds in the Eurozone. Remember, some high net worth depositors in Cypriot banks were “bailed in” in 2013 losing 47.5% of their uninsured deposits exceeding €100,000.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.