Gogo Inc (NASDAQ: GOGO) reported Q4 results that beat expectations. However, the results might be largely moot with their stock price plummeting 29% this week along. For context, they provide inflight internet services for commercial and business aircraft — they are another extreme case of coronavirus collateral damage.

Gogo’s quarterly revenue came in at $221.3 billion, up 7% compared to the consensus estimates of $206.5 million. Earnings per share of -$0.28 beat consensus estimates of -$0.56 by an impressive 50%.

Year over year, Gogo’s quarterly revenues have risen 2%, while earning per share also increased by 62%. The company also exceeded its guidance on full-year improved cash flow, generating $162.6 million in 2019, compared to $100 million guided.

While these are very strong results, it’s safe to say Gogo is facing one of the tougher macro environments. Transportation and ancillaries expected to see a drastic reduction in sales during the first half of 2020. Luckily their balance sheet is healthy with $170 million cash at the end of Q4 and working capital of $172.2 million.

The company elected not to release guidance for 2020 given the uncertainty surrounding the effects of the coronavirus on their business.

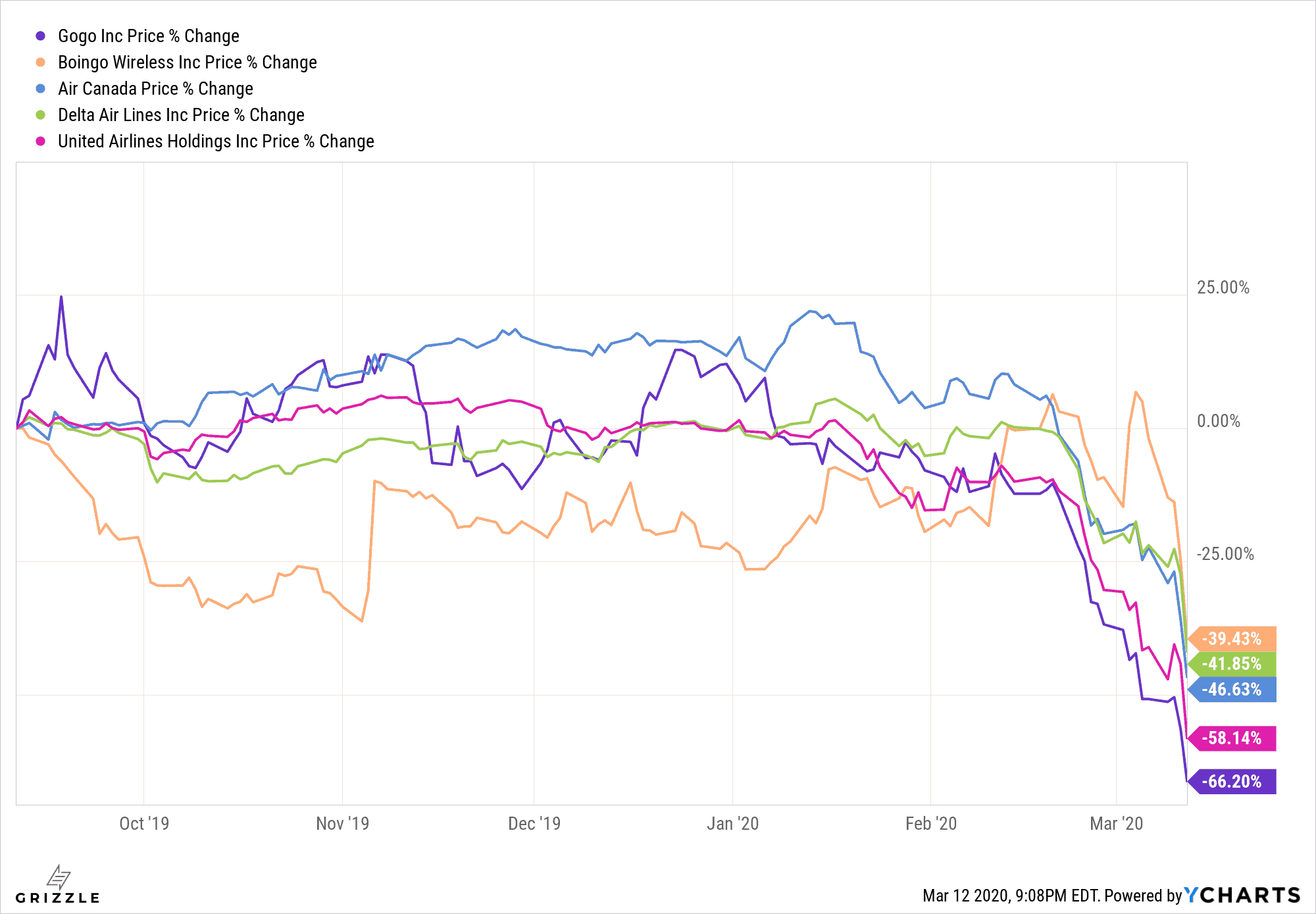

Investors Punish Airline and Ancillary Stocks

Over the last six months, the stock prices of airlines and ancillaries have seen drops in the range of 40-65% in the wake of the coronavirus outbreak. This is substantial compared to the 18% drop in SPY over the same period.

Between cancelled flights and a reduced number of travellers, investors are clearly anticipating multiple quarters of poor financial performance.

For reference, Boingo is anther wireless internet and communications company that primarily services the airline industries.

6-Month Stock Performance

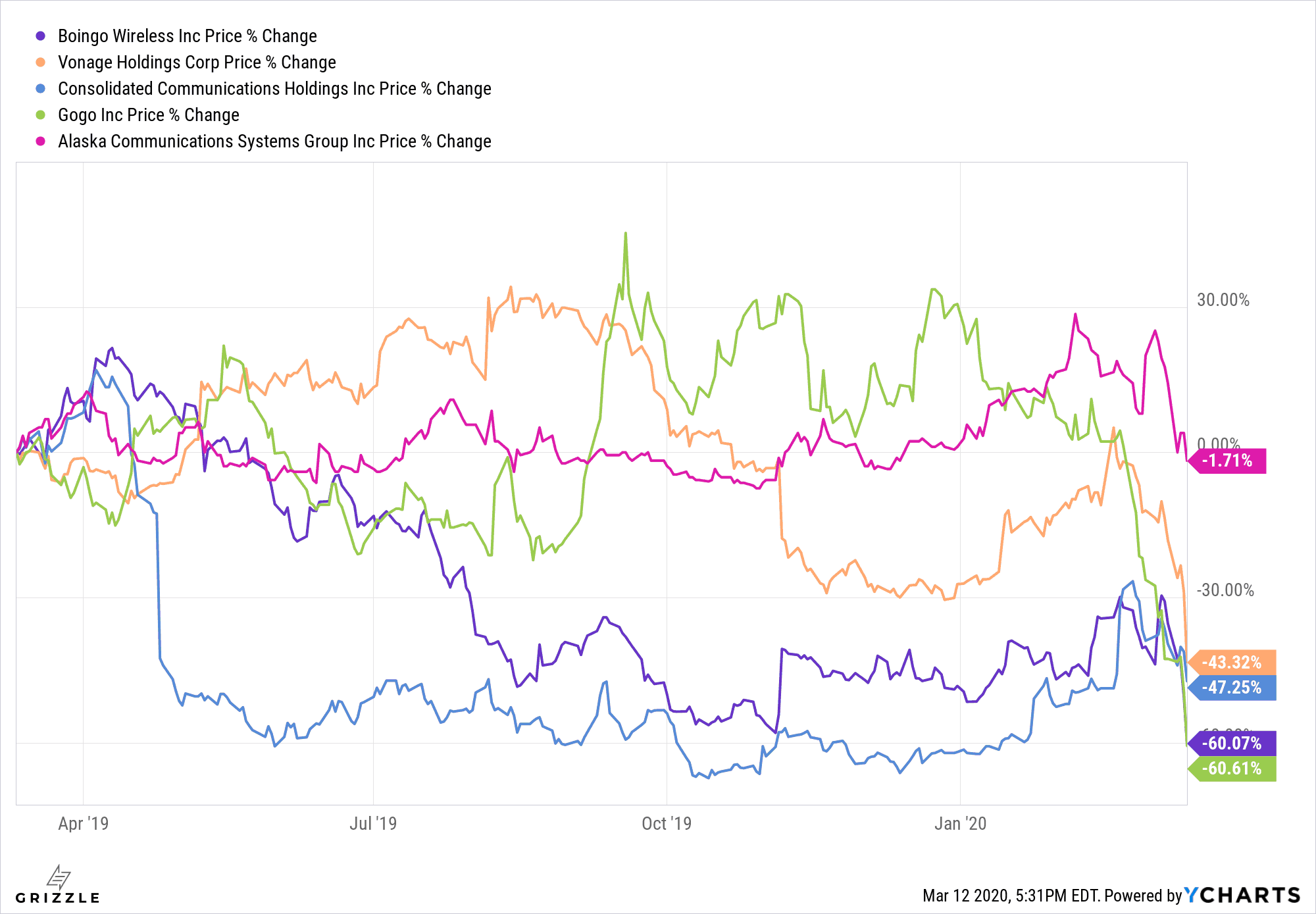

Compared to other mid-cap web-services and communications stocks, both Gogo and Boingo have seen their stock price fall ~15% further in the recent bear market. Both are down nearly 60% over the last year.

This begs the question as to whether the recent sell-off is an over-exaggeration.

Stock Price Performance

Communications Tech Is Tough

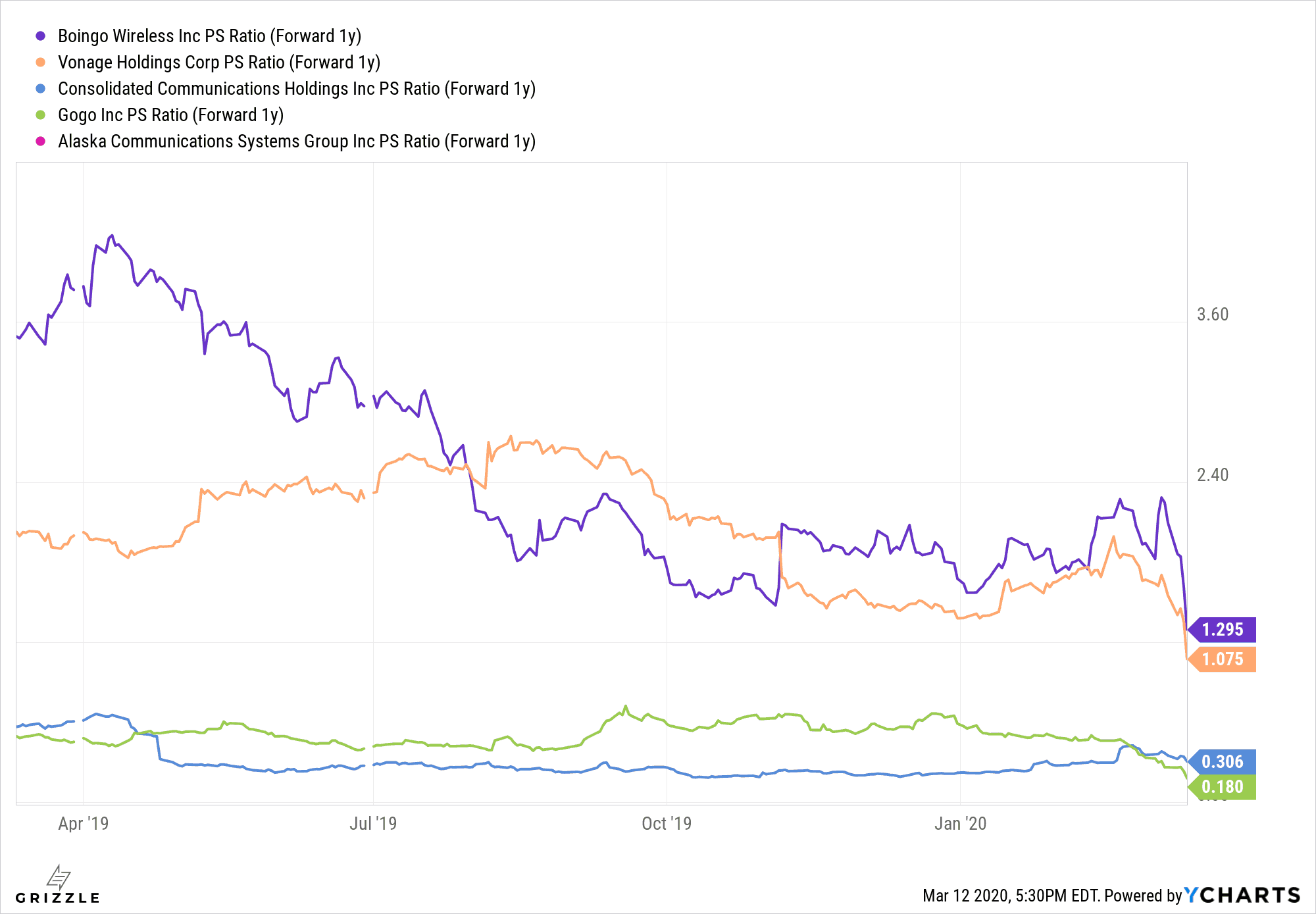

Looking deeper into fundamentals, investors can determine whether this sell-off presents a solid value trade, or whether Gogo may struggle to recover.

From a forward-valuation perspective, Gogo is the cheapest communications stock in the group on a 1-year forward price to sale ratio. Unfortunately, there may be a reason for their discounted valuation.

Forward P/S Ratio (1-Year)

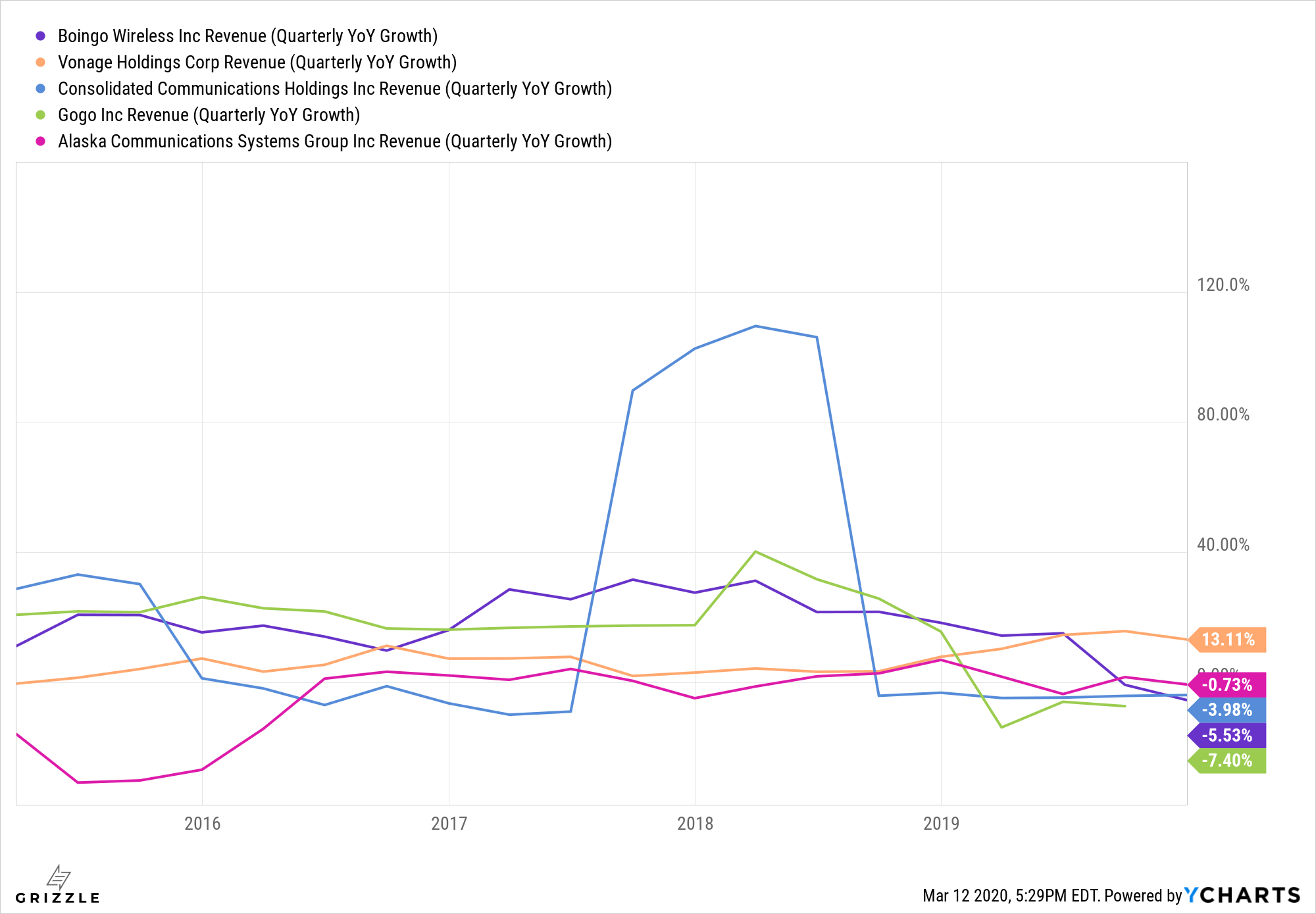

Looking at their operations, Gogo’s revenue growth is also the lowest in the group, at -7.4 year over year. With the impending sales decrease from the coronavirus shock, this is only going to get worse in the coming quarters.

In fact, it looks like most companies have been facing tough times recently, with all except Vonage showing negative growth. This might suggest the industry as a whole is facing some serious headwinds.

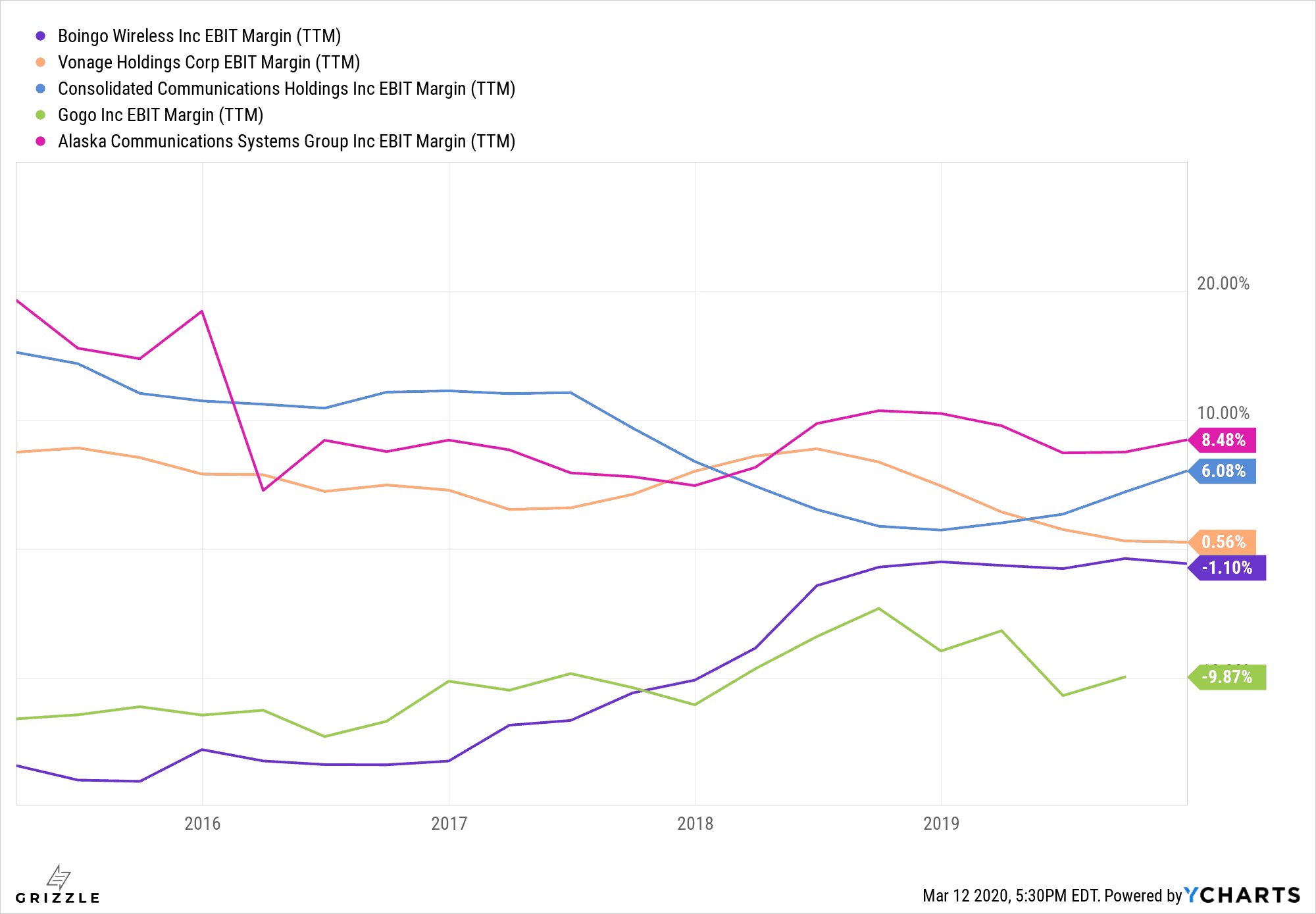

Looking at their margins, investors can tell it’s not a highly profitable business to operate.

Quarterly YoY Revenue Growth

Lastly, looking at profitability, the picture worsens for Gogo, and remains equally as cloudy for the other names.

Gogo is currently posting negative EBIT margins of -9.87%, although they are headed in the right direction. Similarly, Boingo is also struggling to become profitable. Removing depreciation and amortization from the equation and the EBITDA margins shift positively.

As expected, in 2019, they posted a negative EPS, with losses of -$1.81 per share. Looking forward, analyst estimates suggested operations were improving with positive EPS of $0.55 for 2020. However, this is all before the coronavirus outbreak and its corresponding effects.

While it looks like the company has made serious headways to improving operations, it’s unclear what effects (and over what time range) the coronavirus will have.

If it’s only a 1-2 quarter blip, this investment becomes much more intriguing. Until more clarity is provided, however, we recommend taking a wait and see approach. With over $1 billion of long-term debt on their balance sheet, a prolonged drag on their business could end up reversing their recent business improvements.

EBIT Margin

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.