Unprecedented Central Bank Money Printing is the Reason to Own Gold

The massive increase in monetary expansion initiated by the Federal Reserve in the wake of the lockdowns imposed to address Covid-19 is clearly a reason to own gold and, in the case of equity investors, gold mining stocks, on a long-term basis.

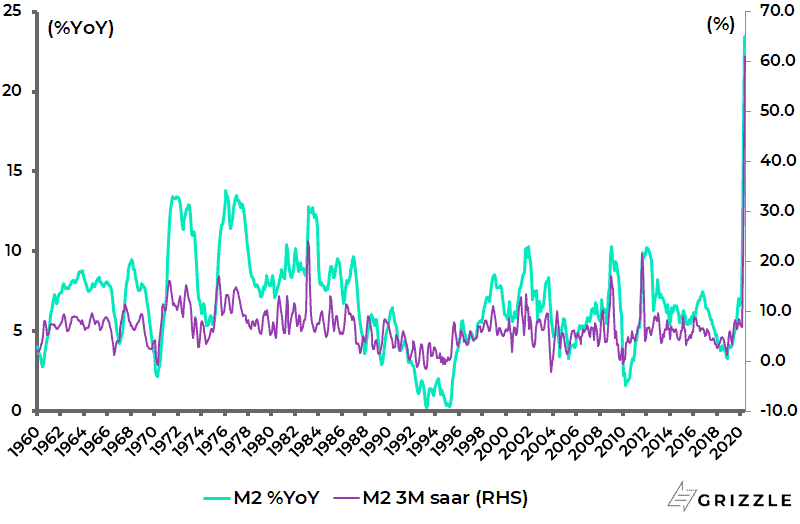

Remember M2 is rising at its most rapid rate since the monthly data series began in 1959, rising by 23.4% YoY in the week ended 18 May and up on a three-month annualised basis by 61.2% in the four weeks to 18 May (see following chart).

US M2 growth

This is why any correction in both gold and gold stocks, which is quite possible in the short term, should be viewed as opportunities to add to exposure to both after the significant gains recorded from the March lows.

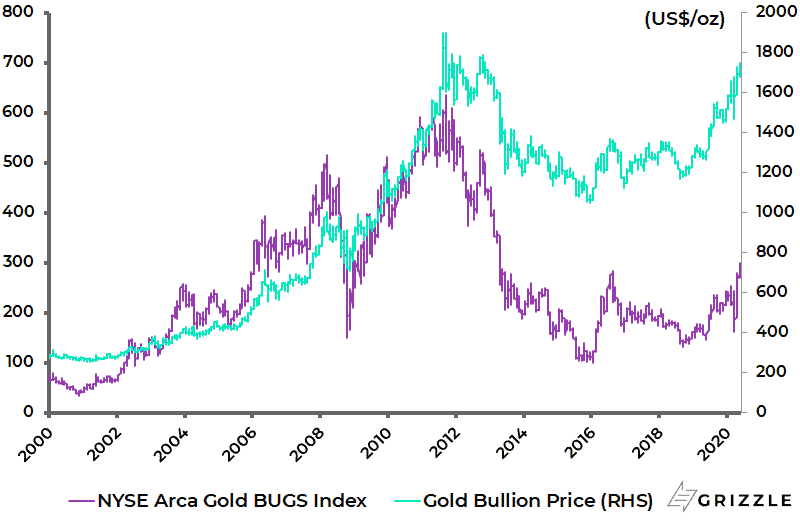

The gold bullion price has risen by 19% since bottoming in mid-March, while the NYSE Arca Gold BUGS Index is up 92% from the intraday low reached on 16 March (see following chart).

Gold Bullion Price and NYSE Arca Gold BUGS Index

Western Financial Investors Driving Bull Market

Meanwhile, it looks increasingly as if the current ongoing bull market in gold will be driven by financial investors in the West whereas the previous bull market from 2002 to 2011 was primarily driven by Asian demand, mainly from India and China.

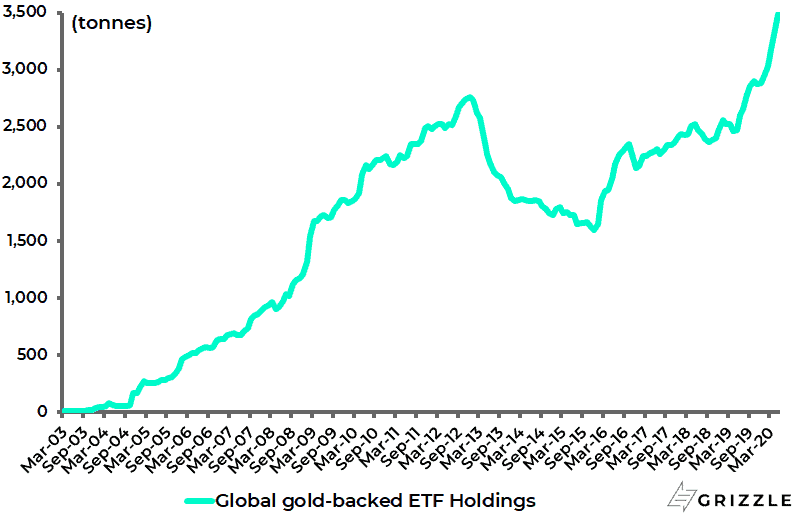

In that previous bull market gold rose from US$277/oz to a peak of US$1,921/oz. The different nature of the buying this time can be seen in the growing amount of money going into gold ETFs relative to history, and the relative lack of demand from China and India, two traditional buyers of gold.

Global gold ETF holdings have increased by 603 tonnes so far in 2020 to a record 3,489 tonnes, compared with an increase of 404 tonnes in the whole of 2019, according to the World Gold Council (see following chart).

Global Gold ETF Holdings

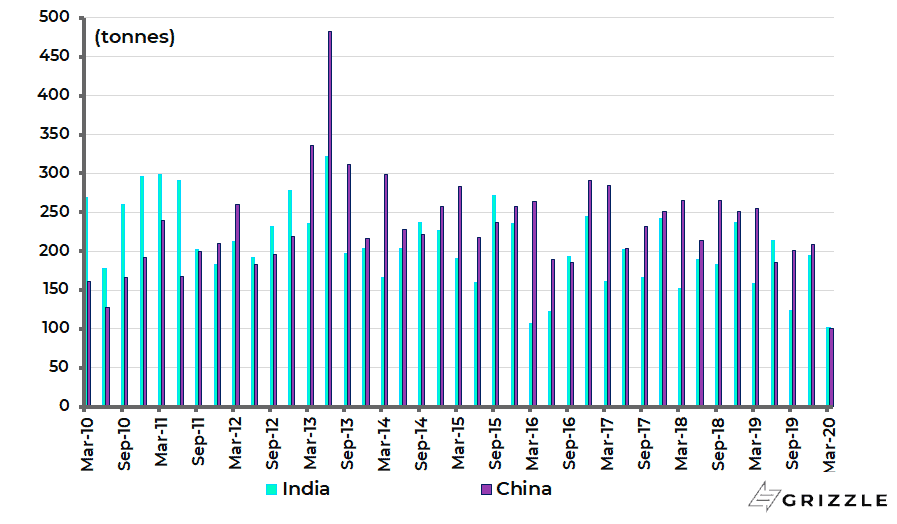

Lockdown has Weighed on Gold Demand in China and India

While consumer gold demand in India and China declined by 48% and 51% QoQ to 102 tonnes and 101 tonnes respectively in 1Q20 (see following chart).

Consumer Gold Demand in India and China

Indeed in India there is probably a growing risk of liquidation of gold caused by distressed selling given the large retail holdings of gold and the lockdown-triggered collapse in economic growth.

India has implemented one of the most aggressive lockdowns in the world. As a result, there have recently been estimates of Indian real GDP growth running at zero!

Central Banks are Likely Sellers – COVID Stimulus Payments will Force Their Hand

The other potential for forced selling of gold could come from central banks given the dramatic fiscal deterioration being suffered by many countries as a result of the massive stimulus programmes they have announced.

Selling some of a central bank’s gold reserves could prove a tempting option. India is an example here given its substantial gold holdings. Official gold reserves in India totaled 655 tonnes (21.1m oz) at the end of April.

Another potential seller is Saudi Arabia where rising fiscal pressures recently triggered a draconian threefold increase in the VAT rate to 15% and the suspension of cost of living allowances. Saudi’s official gold holdings total 323 tonnes (10.4m oz).

Such potential selling pressures are the reason why gold may not break the US$1800-1900 level at the first time of trying.

Gold’s Blue Sky Breakout Mark: $1,921/oz

Still what investors should remember is that when gold finally takes out the 2011 high of US$1921/oz it will be the proverbial ‘blue sky’. The gold bullion price is now at US$1730/oz.

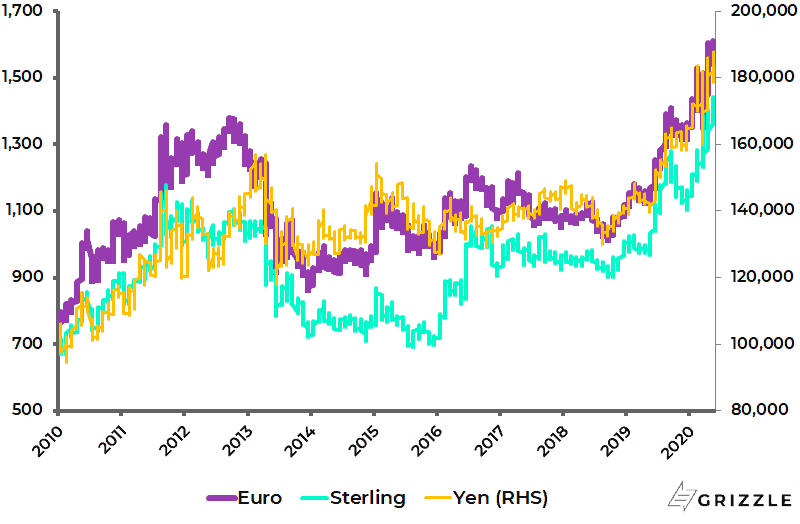

It should also be noted that gold has already made new all-time highs in the world’s other major currencies (see following chart).

Gold price in Euro, Yen and Sterling

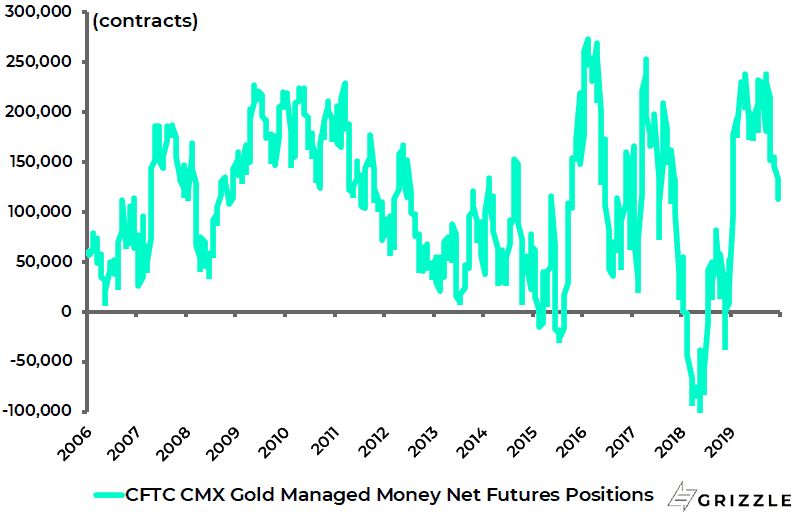

It is a further positive that speculators are nothing like as bullish as they were in mid-2016 when bullish positioning last peaked at a then gold price peak of US$1375/oz.

Money managers’ US gold futures net long positions have declined to 113,081 contracts in the week ended 26 May, compared with a peak of 273,076 contracts in July 2016 (see following chart).

CFTC Comex gold futures managed money net long positions

Own Gold Bullion and Gold Mining Stocks vs. Gold ETFs

Meanwhile, if it is the case from a purist perspective that this writer would advise investors to purchase gold only via bullion or gold mining stocks, it is a practical reality that in a world of convenience shopping most will do so via paper gold ETFs. This is why gold ETF holdings need to be monitored closely.

Fundamentally, gold will continue to track real dollar interest rates, which is why it would be gold bullish if the Federal Reserve fixes long-term government bond yields as discussed here previously (see Stocks & Gold Assets To Own, Real Bear Market Is In Government Bonds, 27 April 2020).

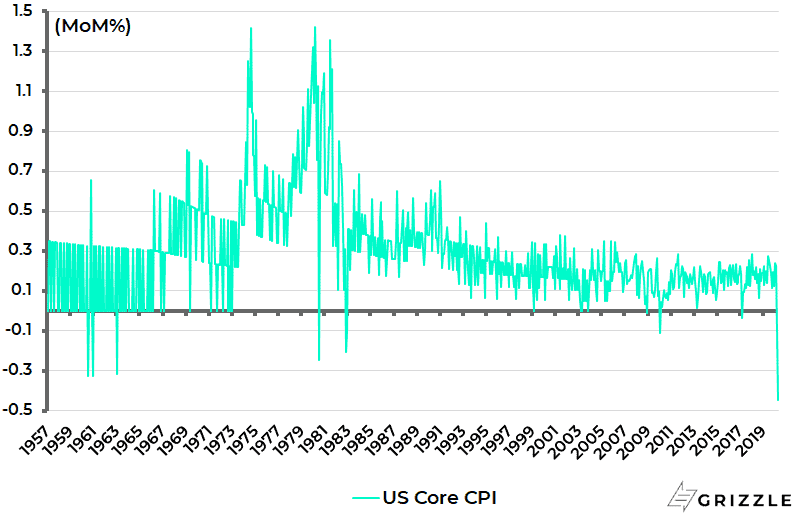

Still in the short-term inflation data will decline dramatically, potentially into outright deflation, as a result of the lockdowns. This trend is already evident from the latest US inflation data, as discussed here last week (see Negative rates or not, inflation’s at your doorstep, 27 May 2020).

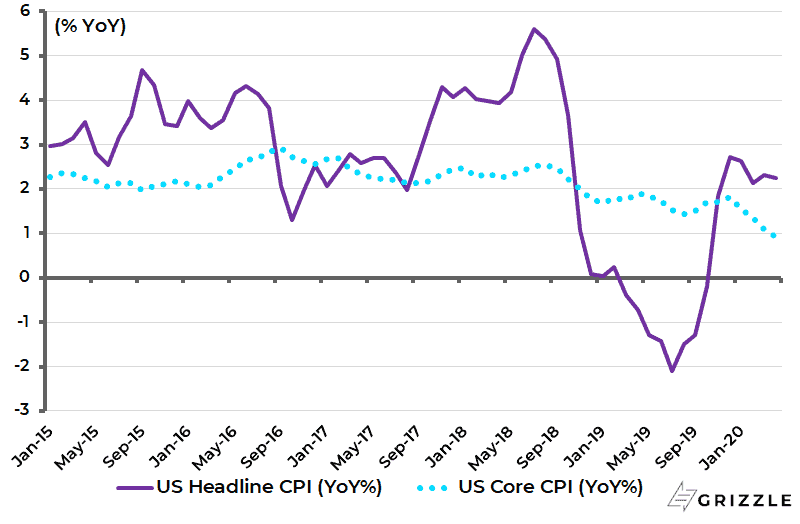

US headline and core CPI declined by 0.8% and 0.4% MoM respectively in April and were up only 0.3% and 1.4% YoY, down from 1.5% and 2.1% YoY in March.

This was the biggest monthly decline in core CPI since the core CPI series began in 1957 (see following chart).

US core CPI %MoM

If inflation turns negative on a YoY basis, the monetary theorists will argue for negative rates because real rates are rising.

Hopefully, the insanity of negative interest rates will be avoided in America. But if not, that would be yet another bullish catalyst for gold.

US Headline and Core CPI Inflation %YoY

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.