Google’s parent company Alphabet (NASDAQ: GOOGL) reported Q1 2020 results that topped market consensus on earnings and revenue. The stock is up 3.3% in after-hours trading.

Revenue & Segments

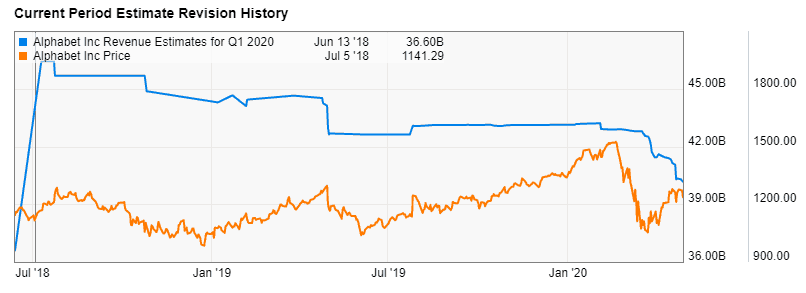

Revenue for the search engine behemoth came in at $41.16 billion for the quarter, beating analyst estimates of $40.17 billion (2.5% beat). Analyst revenue estimates had already been sliced by -7% since the beginning of the year as a result of the coronavirus pandemic.

Revenue had increased +13% versus the previous year and had decreased by -10.7% versus the previous quarter.

The company noted in the press release that performance was strong during the first two months of the quarter, however there was a significant slowdown in ad revenues in March.

Google Search revenue came in at $24.5 billion, up +8.6% versus the previous year and down -10% versus the prior quarter. CFO Ruth Porat noted on the conference call that in March revenues began to decline and ended the month in at a mid-teens year-over-year percentage decline. Although search activity increased as a result of the coronavirus, users’ interest had shifted to less commercial topics and additionally there was reduced spending by advertisers.

YouTube revenue for the quarter was $4.0 billion, up +33% versus the previous year and down -15% versus the prior quarter. Direct response continued to have strong results throughout the whole quarter, while brand advertising growth began to experience a headwind in mid-March. By the end of March total YouTube ad revenue growth had decelerated to a year-over-year growth rate in the high single digits.

There are 2.5 billion monthly active devices for Google Play, during the pandemic CEO Sundar Pichai noted that app downloads increased by +30%.

Earnings & Outlook

On the earnings line, Alphabet beat analyst estimates by 10.5%, posting earnings of $11.90 per share compared to consensus estimates of $10.76. Analyst have reduced their earnings estimates by -14% since the beginning of the year.

Alphabet’s operating margin decline from 21% in Q4 2019 to 19% in the current quarter.

The CEO believes the company is positioned for resilience post the coronavirus crisis as Google’s Search ad model is easy ‘on’ and ‘off’ for advertisers, additionally the company is more diversified primarily driven by Cloud.

Ruth Porat stated the second quarter will be difficult for advertising, while Cloud continues to be well positioned. The company is slowing the pace of hiring to protect of margins, headcount growth will be decelerated by the 3rd quarter of the year. Alphabet now expects a reduction in capex for the full year.

Performance & Valuation

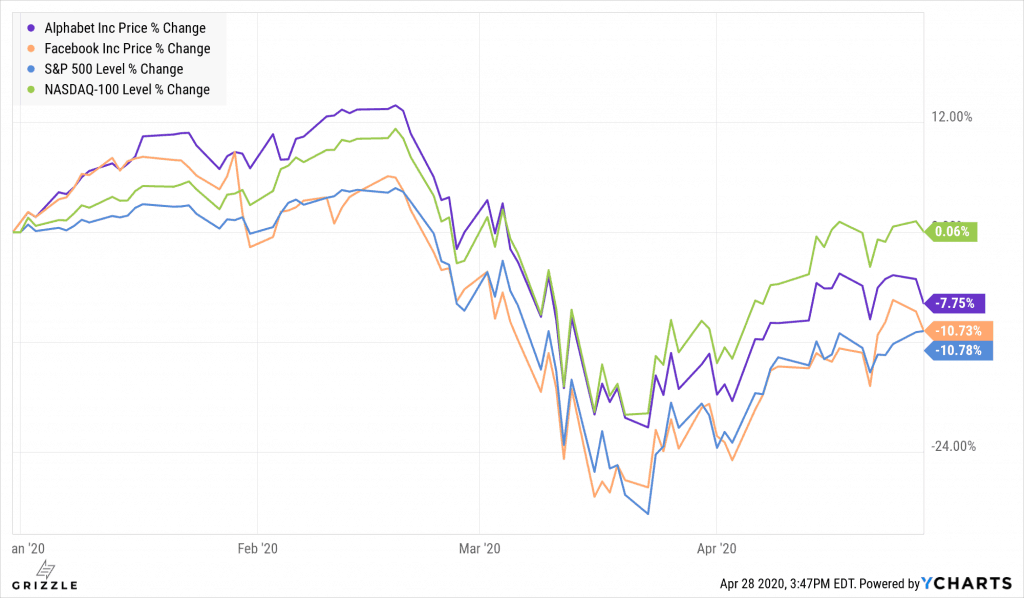

On a year-to-date basis Alphabet stock has under-performed the Nasdaq 100 by -7.5% because of the company’s reliance on ad revenue. However, Alphabet has outperformed Facebook by 3% in the same period, a company with similar exposure to ads.

Year-to-Date Price Performance: Alphabet, Facebook, S&P500 and Nasdaq 100

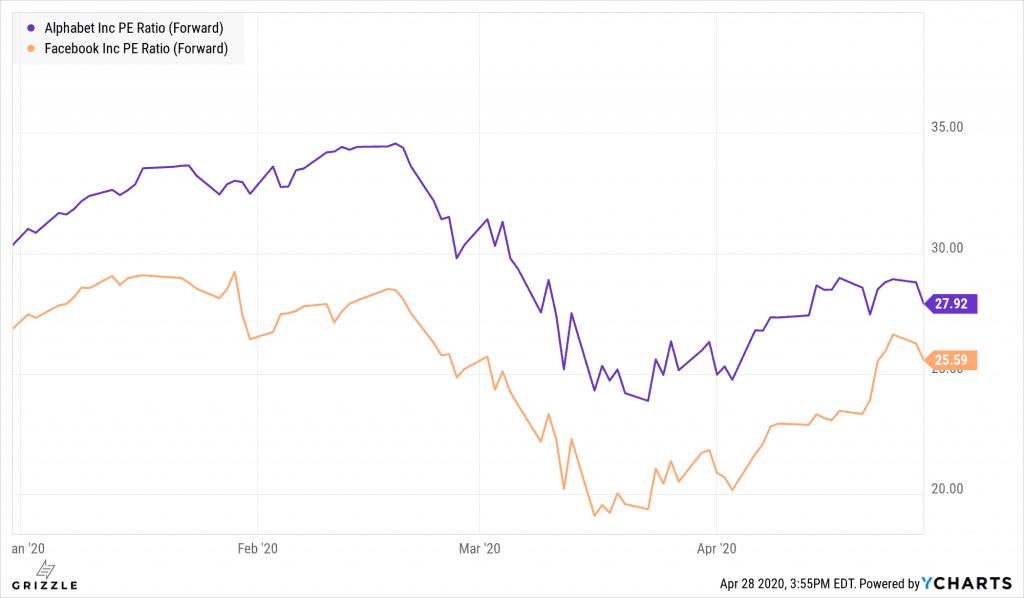

On a forward consensus P/E valuation basis Alphabet trades at a modest premium to Facebook, 28.0x versus 25.7x respectively. We believe the premium is warranted given the quality of Google’s core offerings: Search and YouTube.

Forward Price-to-Earnings: Alphabet vs. Facebook

https://youtu.be/DtqUdNfHrQI

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.