Reports out of the mainland of late have seen a lot of discussion on President Xi Jinping’s new slogan of “Common Prosperity For All”, which emerged from reports of a meeting in August of the Communist Party’s Central Committee for Financial and Economic Affairs chaired by Xi.

This, and the announcement by Tencent in mid-August that it has set aside Rmb50bn to aid the government’s redistribution efforts, has raised concerns that making money is now politically incorrect in China (see Global Times article: “Tencent invests 50 billion yuan to help promote ‘common prosperity’”, 19 August 2021).

While such concerns are understandable it is necessary to put them into some perspective.

This is more a case of paying working people more than launching a full-scale attack on money making; though it should have been obvious since Xi launched the original anti-corruption campaign back in late 2012 that ostentations and displays of extreme conspicuous consumption were no longer advisable in mainland China.

While press reports have focused on Xi’s calls for higher taxation and the like, a Google translation of the notes of the abovementioned meeting also showed the Chinese leader called for “encouraging hard work and innovation to get rich” and “creating opportunities for more people to become rich”.

This writer is personally convinced that the Chinese leadership understand it needs innovation and entrepreneurship to upgrade the economy, and this requires the appropriate incentives.

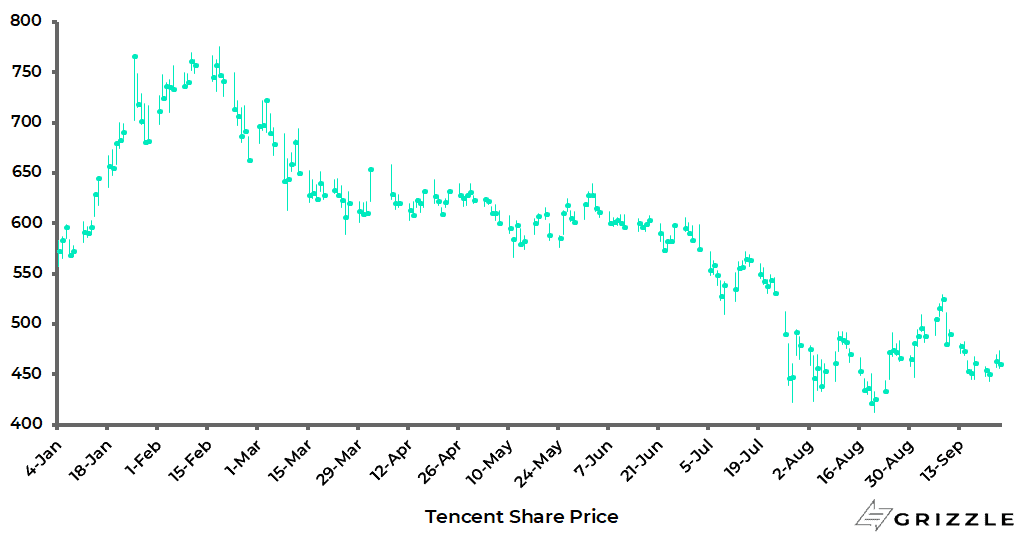

As for the Tencent news, and Tencent as a company has always shown itself more sensitive to the prevailing political winds than Alibaba, this also needs to be kept in some perspective.

The fact is that Chinese internet companies, which have been designated as so-called “key software enterprises” (a category including Alibaba and Tencent), have enjoyed beneficial corporate tax rates of 10% since 2008.

Many other companies pay a rate of 25%.

It is also the case that the negative market response on the day the Rmb50bn provision was paid by Tencent contrasts with the way American Big Tech stocks have usually shrugged off news of fines levied by American or European regulators on the likes of Facebook or Google.

This market action reflected investors’ relief that the regulators were only administering fines and not changing the rules of the game.

Tencent Share Price

US Government Lawsuits Continue to Roll out Against Big Tech

This in turn raises the issue that, while Chinese internet companies are now facing the reality of a change in the rules of the game, that remains only a potential risk in America.

Still, the risk of meaningful legislative and/or regulatory action in America against Big Tech certainly cannot be ruled out altogether, though the process will clearly be far more drawn out than Beijing’s top down enforcement methods.

That said, there have been some interesting developments on this issue in recent months which are worth recording.

In this respect, the Federal Trade Commission (FTC) filed a new complaint in a federal court against Facebook in August saying that it violated antitrust laws by buying Instagram and WhatsApp.

This is after an earlier FTC case was dismissed by a US district court judge in June.

Besides the Facebook case, the Justice Department and state attorney generals across America have multiple lawsuits pending against Google while both Democrats and Republicans have recently introduced bills in Congress concerned with anti-competitive practices by Big Tech, an issue which now crosses the political divide.

The latest move to relaunch the Facebook case comes after President Joe Biden in June named Lina Khan chair of the FTC.

This was a newsworthy appointment at the time as she has become one of the most vocal critics of Big Tech from her time working on the House of Representatives Judiciary Committee where she helped lead a 16-month long investigation into anti-competitive practices.

Interestingly, her confirmation was approved by a 69-28 bipartisan vote in the Senate.

As a sign of its concern, Amazon filed a motion in late June to recuse Khan from all business pertaining to the company.

Facebook also filed a similar motion in mid-July.

Meanwhile the Biden administration also nominated in July Jonathan Kanter as leader of the Department of Justice’s antitrust division.

He is a favourite of the progressive wing of the Democratic Party and, like Khan, advocates more aggressive antitrust enforcement with a focus on Big Tech.

If confirmed, he will take over the antitrust lawsuit filed against Google by the DOJ and a coalition of states for the company’s alleged monopolisation of search; though this case is not scheduled for trial until 2023.

As for the legislative proposals, five bills were introduced in the House in June which target various anticompetitive practices.

So far as this writer understands the details, one of them would effectively ban Big Tech companies from owning or operating a business that uses its platform for its primary product offering.

This would create a potential issue for, say, Google’s ownership of YouTube. Another bill would ban actions that benefit the company’s own services over competitors.

An example here would be giving a higher ranking to a platform’s own products in search rankings.

Another bill would put the burden of proof on Big Tech when they make acquisitions in terms of not buying out a potential competitor.

US Investors Still Unconcerned about Tech Regulatory Risks. Why?

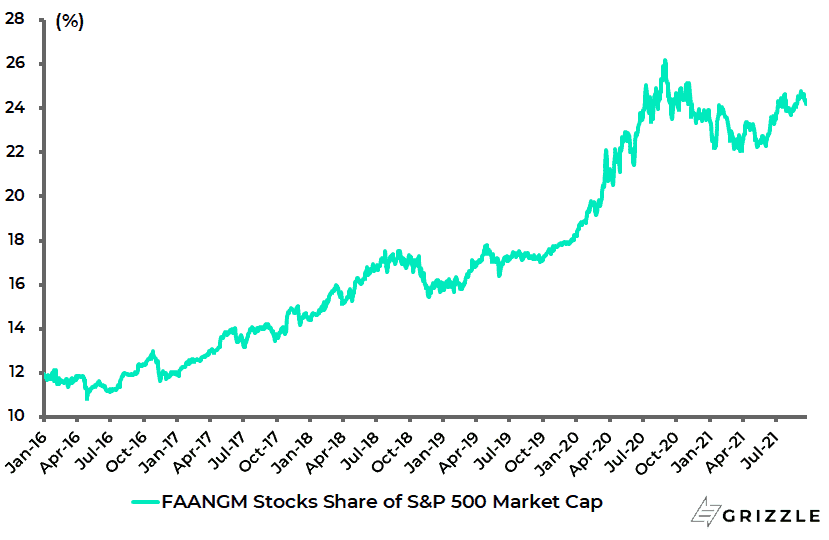

If such bills and legal cases are pending, it might be asked why there is not more concern in the stock market where the six Big Tech stocks still account for 24.2% of S&P500 market capitalisation though down from a peak of 26.2% in early September 2020.

US Big Tech’s Share of S&P500 Market Cap

The answer is that the market expects nothing to happen anytime soon in terms of actual legislation being passed while court cases take time and can always be appealed.

Still the issue of regulating Big Tech is not going to disappear altogether.

The progressive wing of the Democratic Party is certainly focused on it; though the Democratic establishment has always been very close to Big Tech which is why this writer must admit to surprise at some of the Biden administration’s recent appointments.

As for the Republicans, they must now surely regret that they did not do more about this issue when they controlled Washington, most particularly given the removal of Donald Trump from Twitter since 8 January.

Indeed there is now the extraordinary situation that the Taliban have access to Twitter but not America’s former president.

This probably guarantees that, if the Republicans ever control any part of Washington’s executive or legislative arms of government again, they are likely to move aggressively on this front.

That is, if nothing eventuates from the current bills before the House.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.