When Green Growth Brands (CNSX:GGB) first hit the public markets in November, the pitch was filled with tons of potential.

Backed by the founders of DSW and American Eagle who brought enviable consumer branding experience and industry connections to the table, the sky seemed the limit.

However, like many other early cannabis ideas, the growth aspirations got ahead of the financial realities of running a successful business.

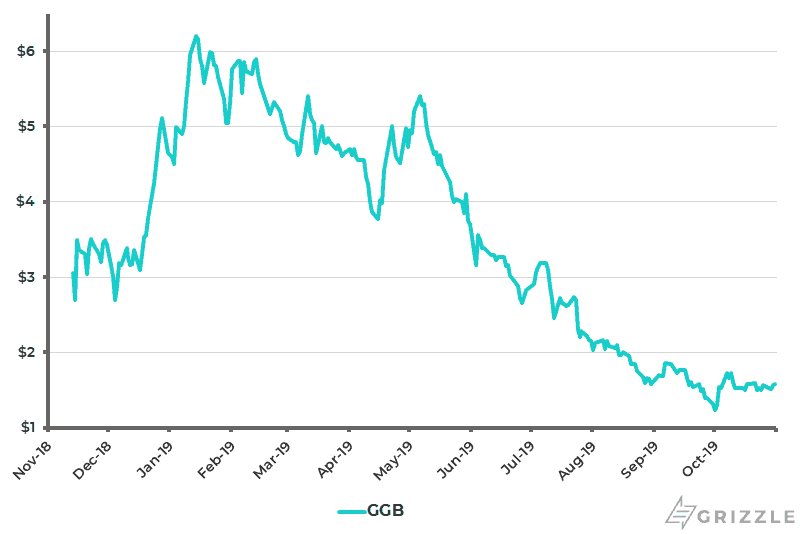

GGB has been on a crazy roller coaster ride in only 12 short months.

From listing in November at an opening price of C$3.05/sh, to bidding for Aphria in December, hitting C$6 in January to now sitting on a C$1.60 share price, times have changed.

Similar to the precarious situation MedMen finds itself in, Green Growth has borrowed too much and is struggling to find the cash to pay back the loans once they come due.

GGB Needs to Survive Two Big Debt Payments

On November 15th 2019, GGB will be on the hook to pay back a $30 million promissory note to GA Opportunities corp related to GGB’s buyback of shares in May.

GGB does have a lifeline, with an undrawn lending facility of $77 million, split into a $25 million chunk and a $53 million chunk.

If GGB is only able to borrow $25 million of the $77 million lending facility the company will be out of money by November 15th when the $29 million loan from GA opportunities fund is due.

If they are able to borrow the full $77 million they will end the year with $20 million or less of cash we estimate, but are on the hook for a debt payment of $45.5 million due May 17th 2020.

Keeping in mind GGB burned $28 million of cash in the latest quarter just on operations and property construction, they are operating on the razor’s edge to even make it to December with any value left for stock holders.

$28 million is probably too low considering the purchase of Moxie, another multi-state operator, and Spring Oaks a Florida license holder haven’t yet closed.

Green Growth will have to pay for these company’s burn rates as well, telling us the cost structure is going up not down.

Is There Any Value Left for Shareholders?

While avoiding a liquidity crisis (ability to pay debt coming due) is one thing, the actual value of the business remaining for stockholders is yet another.

If you own shares in Green Growth Brands, what you really care about is if there is any equity value left for you after all liabilities are paid.

And here is where we have some bad news.

| GGB Value (MM USD) | Jun-19 | Oct-19 | Dec-19 |

| Cash | $10 | $70 | $21 |

| Goodwill | $36 | $219 | $219 |

| Intangibles | $40 | $76 | $76 |

| Total Assets (adjusted) | $150 | $574 | $525 |

| Tangible Assets | $94 | $317 | $269 |

| Total Liabilities | $106 | $106 | $185 |

| (+) New Debt since June | $79 | ($30) | |

| Total Liabilities + Debt | $106 | 185 | 155 |

| Shareholder Value $USD | ($12) | $133 | $114 |

| Shareholder Value $CAD | ($16) | $172 | $148 |

| Shares Outstanding (million) | $194 | $384 | $384 |

| Stock Value/Sh | ($0.08) | $0.45 | $0.39 |

As of June 30th 2019, shareholders are effectively wiped out if the company writes down any goodwill or intangible assets.

However there are some moving parts that make the future look slightly better than the past.

Forecasting the balance sheet as of today and the end of the year, the stock value increases slightly after incorporating the Moxie and Spring Oaks acquisitions (done with stock), but the stock value continues to erode thereafter because of the large cash burn.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]By the time May rolls around and the $45.5 million debt payment is due, GGB will be out of cash. Their only options will be to issue more shares or borrow more debt, both of which will lower the value of your stock. Add in the millions of out-of-the-money warrants and options and we can’t see how this stock can recover. [/su_panel]Typically a profitable company will continue making money which increases the value of the assets and the equity (stock), but in GGB’s case this company is still deep in the red.

Every quarter that goes by sees the value of assets decrease while the company either issues more stock or takes on debt to keep the lights on.

The end result is falling assets, increasing liabilities and a less valuable stock.

Our estimate of the true value of this stock is 75% below where it trades today at C$1.60/sh. The downside is real.

What Should Stockholders Do?

Bullish investors will likely argue the company can issue more shares and/or borrow to bridge the gap until they can turn a profit.

With rapid revenue growth and huge footprint in CBD locations, the cashflow upside should be significant.

But when you look at the financials, GGB has a long and uncertain road to profitability.

To start, GGB had a negative gross margin in the past year.

This is the equivalent of opening a bakery and selling cookies for $1.00 when they cost you $1.50 to make. You won’t be in business long with this model.

Even in a future where revenue increases to $100 million a quarter by the end of 2020, from $7 million today and the gross margin increases to 50% from 0%, GGB will just be breaking even.

By Q4 2020 GGB will have borrowed another $75 million of debt or diluted shareholders by at least 15%-20%.

Any way you look at the future of this company, the stock price is going lower.

Green Growth Brands is in a downward debt and equity spiral from which it is unlikely to recover.

Cut your losses and move on.

Full Disclosure: The Author has no position in any of the securities mentioned in this article

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.