Green Growth Makes the Offer for Aphria Official

As investors, we think the official offer from Green Growth Brands (GGB) undervalues the company, no question. However, it provides a positive piece of information to investors.

If the prolific Schottenstein family is willing to make an official offer and put significant capital at risk to buy Aphria, they are signalling to the market they believe regulatory- and lawsuit-related tail risks are manageable and will not impair the ultimate value of the Aphria assets.

This is a powerful signal to send to other suitors who may be struggling with how to value Aphria’s liabilities.

Sentiment is likely shifting in Aphria’s favour, making it more likely a higher offer will eventually appear if shareholders reject the offer from GGB and Aphria’s stock languishes.

The GGB offer has also signalled to the market that Aphria will not stay independent forever at its current price.

Other cannabis players know they could never put together a similar Canadian asset package and international footprint for only $1.7 billion, Aphria’s current USD market cap.

Aphria trades at a 50% capacity discount to peers, presenting a wholly unique opportunity for a U.S. operator with expensive paper such as Acreage, Curaleaf, or Green Thumb to think two steps ahead and pick up a unique international footprint to be ready when the cannabis market goes global.

They could offer $12 per gram, presenting 25% upside for current investors then turn around and sell the Canadian capacity for $15 per gram, still a significant discount for a potential acquirer but netting the company a cool $750 million profit.

Plan B – Aphria Continues As Is

If at the end of the day, no offer comes along that management and shareholders believe is realistic, Aphria can still go it alone and investors will be handily rewarded.

Aphria has $173 million of cash in the bank, enough to support the company until it finishes the remaining $85 million of greenhouse construction in Canada and brings the entire 255,000 kg of annual capacity online later this year.

Starting in 2020 Aphria’s capacity should generate enough cash flow for investors to realize a juicy 10%-20% free cash flow yield.

At this point, Aphria’s stock should trade for at least C$15/share or the company becomes an extremely attractive takeout target.

Luckily, as Aphria investors we are effectively being paid to wait, with potential acquirers on the prowl and a wave of free cash flow just beyond the horizon.

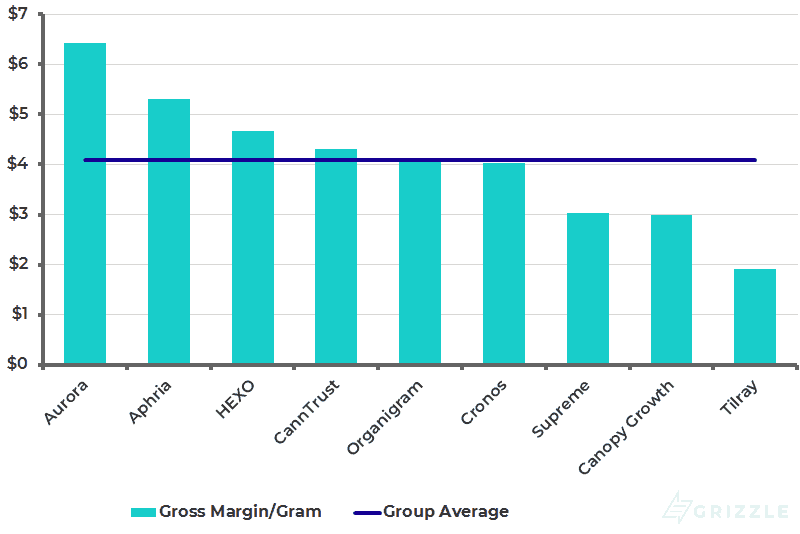

Canadian LP Current Gross Margin

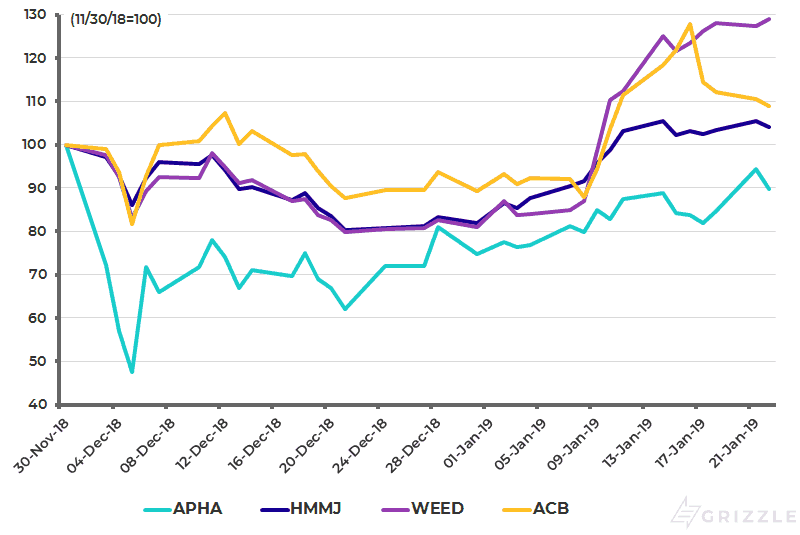

Aphria’s share price has recouped nearly all its losses since the publication of the short report. However, it has languished against its large-cap peers (Canopy and Aurora) and the broad cannabis index (Horizons Marijuana ETF – HMMJ).

Continued strong operational execution is the clearest pathway for Aphria to regain relative performance versus peers.

Relative Share Performance Since Short Report (Indexed)

Offer Details

Green Growth Brands made their tender offer for Aphria official last night.

They are offering 1.574 GGB shares for each Aphria share, valuing Aphria at $8.80/sh or 7% below yesterday’s close.

Green Growth has lined up a related-party entity who agreed to backstop $150 million of a $300 million capital raise which would be contingent on Aphria shareholder approval of the deal.

This investor will be paid $7.5mm in GGB shares for providing the backstop, or 1.25 million fully diluted GGB shares giving them 12.5% of the voting rights at GGB.

In the interest of full disclosure, employees of Grizzle personally purchased and currently own stock in Aphria, Inc. See the Content Disclosure section here on our Terms and Conditions page for more details.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.