https://www.youtube.com/watch?v=Lds2y7ZLAXU

Amazon

- Amazon has already proven its a winner, and is getting a huge tailwind from Covid-19.

- Our play was ETSY Call Options. We did sell a little early because at one point they were trading at a higher multiple than Amazon – which is obviously fundamentally off.

- Part of the COVID-19 “Buy the Dip” portfolio.

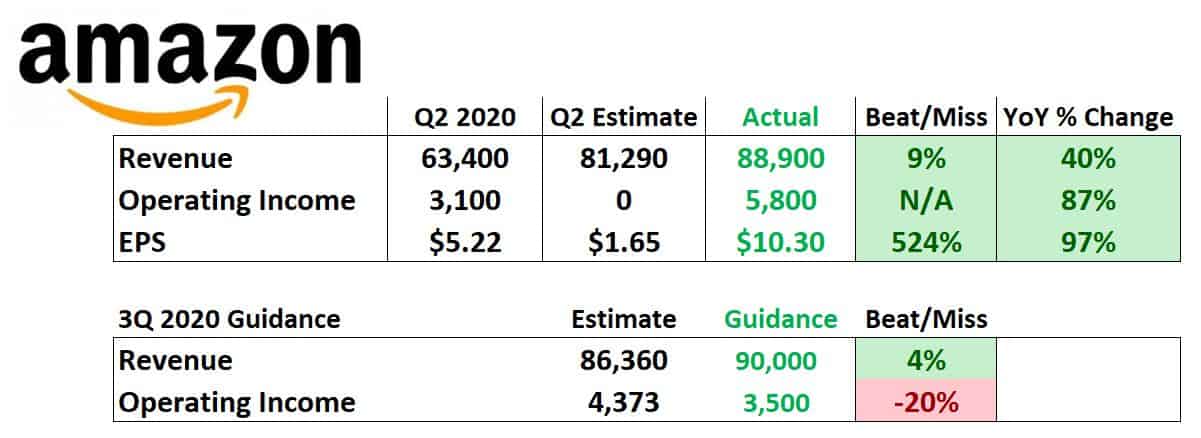

Amazon Earnings Results

- Growth in Revenue as a % Y/Y has been increasing the last 6 months.

- Massive increases for a company of this size.

- Crushed operating income estimate of 0.

- Including the $4bn they spent on COVID-19, operating income was

- Hedge Funds knew results were going to be good, it had a run baking in these results ahead of earnings.

- Guidance is above street with normalizations for covid-19 spending (~$5500MM)

- Story: Amazon should still work right now.

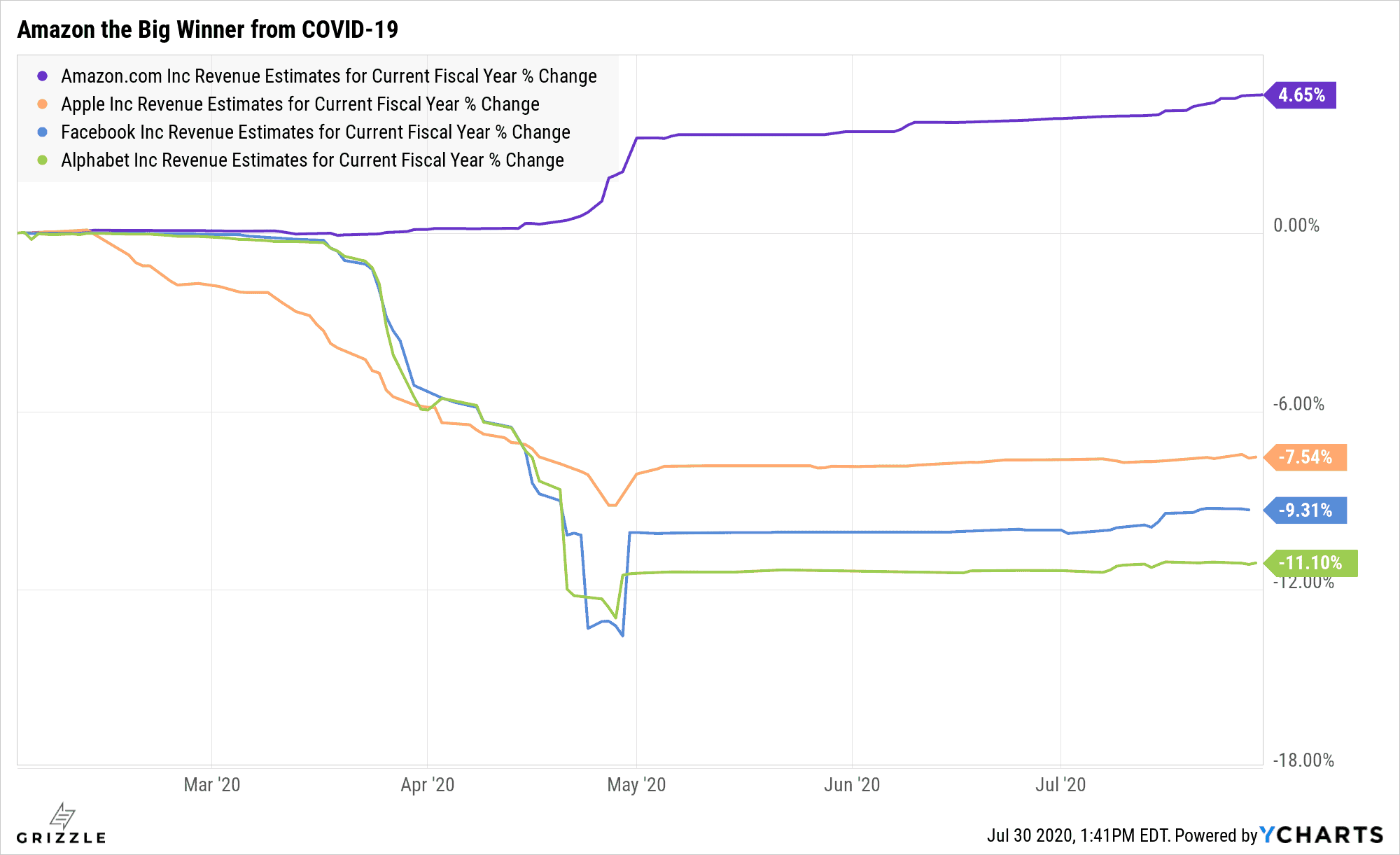

- Amazon is the only company on a re-acceleration of growth out of the mega-cap tech stock bucket.

Amazon Only Stock with Increasing Estimate Since COVID-19 Hit

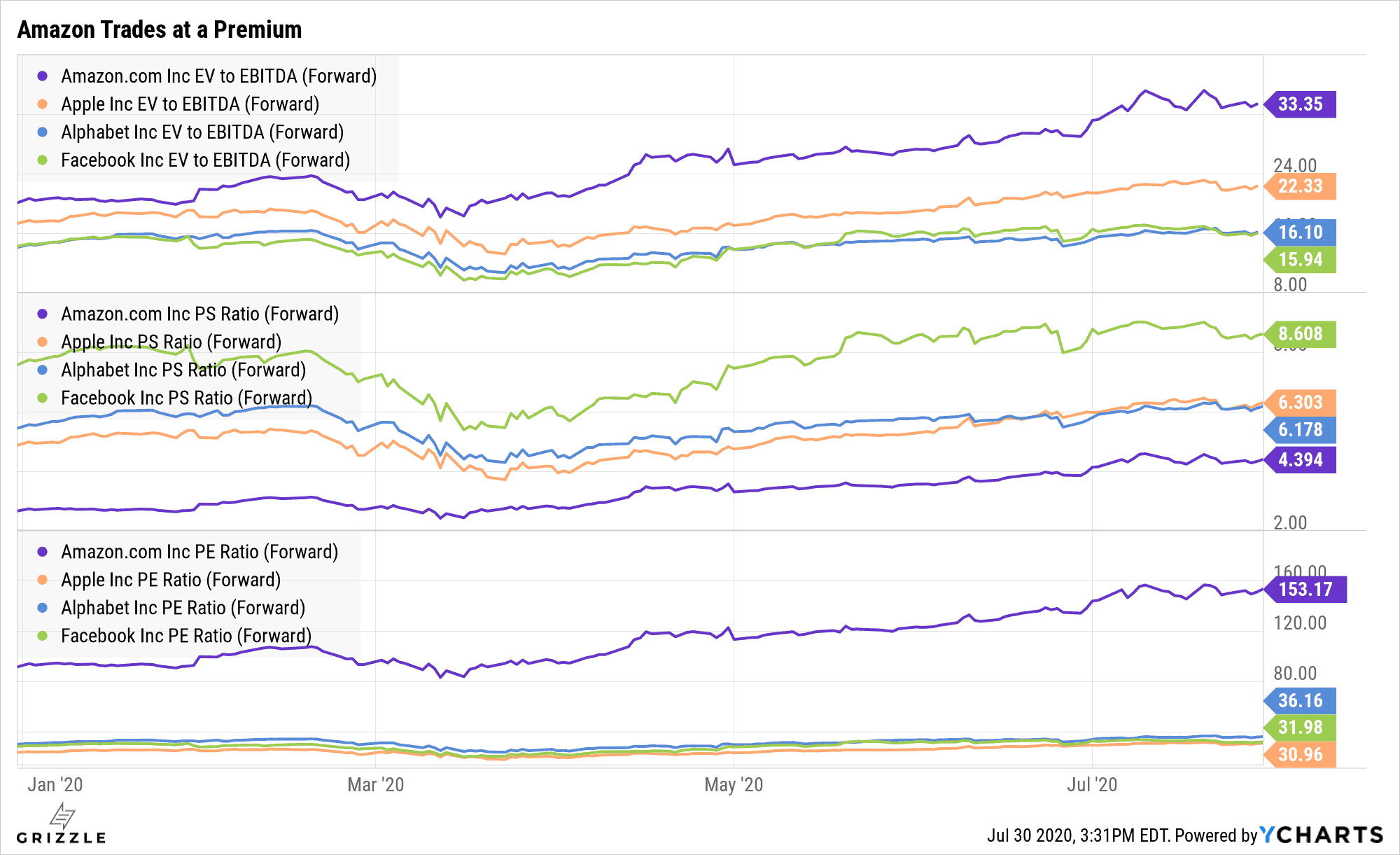

3 Ways to value Amazon – EV to EBITDA, Price to Sales, Price to Earnings

- P/E: Amazon looks ridiculously expensive, thing is Bezos makes decisions on how he spends money. Bezos chooses to re-invest most cashflow back into the company rather than paying it out to shareholders – this is good for the company’s growth and profitability long-term, but artificially reduces earnings to shareholders in the short-term. Why stock looks expensive on P/E

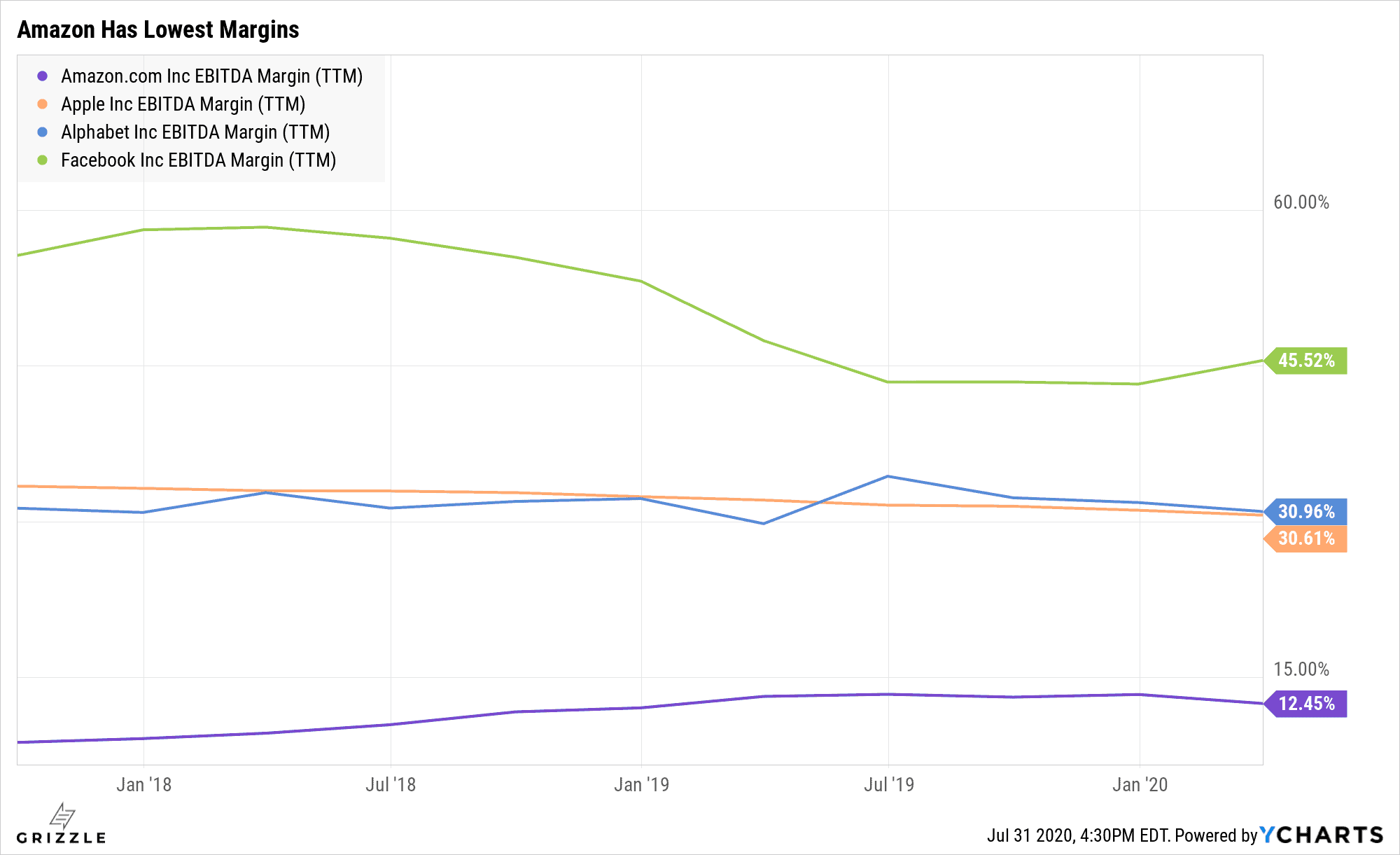

- P/S: Amazon is the cheapest – not really being valued on sales, as Amazon has the lowest margins among peers, therefore it’s invalid to use this measure to value the company.

- EV/EBITDA: Best measure in this situation because it looks at cash flow from core operations, Amazon trades at a good premium, justified by accelerating and faster growth than peers. Not a ridiculous multiple relative to peers.

Traditional Value Investing is out of fashion

- Remaining value managers scared out of positions, hiding in Amazon.

- Not smart enough to find the next $ETSY. Basically managers want to keep their jobs out of incompetence.

- Dead Money/Old Economy stuck in the value bucket and that’s why value is underperforming. It’s not that there are value tech stocks that are underperforming.

- Value managers (such as Warren Buffett) missed out completely on Technology (SaaS), problem with value as a concept: you just get focused on things like “52 week low, oh there’s an opportunity here” – you miss the justified 52 week highs.

- Old industries dying out, new industries coming up. Your traditional value stocks are dead. Value Growth isn’t working because of that factor.

Energy:

- Energy Economy is dead, if a manager tells you in January 2020 that they were bullish on Energy, you should unfollow them because they’re clueless – same goes for if a hedge fund manager says that the world is going to need more oil/energy in 5 years, still clueless. Ignore it. Happens every cycle. There will never be a shortage in oil.

- US Shale will only get bigger, more and more supply. It’s a lose/lose situation for absolutely everybody.

- $XOM is not looking as great as tech stocks.

- $40/Barrel is a suicide price for oil companies – exact price that makes all companies not great, but high enough where everyone can survive, keeping supply high.

Apple:

- 4-1 Stock Split – Take advantage of Robinhood Investors – more accessible to broader base of investors.

- 3Q Revenue – 59.7B – up 11% Y/Y – Impressive everything considered.

- Blew through estimate of $52.3B.

- Service Revenue up 50% Y/Y – largest improvement.

Agnico Eagle Mines $AEM

- Played out incredibly well since the call.

- Probably too late to be buying call options on it now, should only be buying call options when there’s blood in the streets, now is not that time.

- Buying Stock is still feasible because the risk is reduced and there is still runway on this trade.

- The management team has the longest proven track record of success and defensibility.

- EPS beat by 20%, Operating Income by 30%, Production by 8%, all good stuff.

- Gold Sector was down while $AEM had a comeback today. Ironclad safety trade.

- Credits to @BullishBearz for the early tip on the trade.

- AEM is a AAA 5 Star gold mining company.

- Fund managers are not comfortable with mid/low-cap gold mining stocks, there are only 3-5 large-cap gold miners that have a solid reputation which is why all the institutional money has gone into them.

- $AEM should not be trading at the same Price / Cash Flow as Barrick Gold (a huge gold company that has done everything wrong in the last 10 years). The trade here is the 40-50% catch up trade – catching up to the premium it deserves relative to its peer.

- Dividends: AEM will be gushing FCF, high chance that they could raise their dividend. There is a massive community of income funds that need to get to safety in Canada/USA – a large-cap gold miner with high dividends is VERY attractive for income funds right now – this helps push AEM’s stock price higher.

Looking at Sources of Information / Fundamental Research

- Stop referring to broker research – don’t listen to any hedge funds.

- Learn from your past experiences, do your own due diligence.

- Sell-Side Research is trash because those firms need to maintain relationships with the companies they cover because those companies pay their firms through other services.

- It is not in a sell-side firm’s best intentions to take a stance against a company. They will always put arbitrary numbers based on how the stock has done in the last quarter.

- Only ones who talk with conviction are buy-side analysts because they have skin in the game, money on-the-line.

- Beauty of Financial Twitter, there are two sides to every coin and you can research both angles.

Sentiment vs. Fundamental Research:

- Thomas was playing sentiment, reading what the market thinks and is going to think – really hard to do.

- Guided by risk management.

- Reason why you do fundamental research – even if you’re a trader – because it puts you in the right ballpark. You’re on the right management team, right assets, it’s harder to get your trades completely wrong.

- The market is geared towards going long stocks. It’s expensive to short or bet against stocks.

- Don’t follow people who are only short investors. It’s very hard to make money off short ideas such as fraudulent companies, etc. If they don’t have a long book they aren’t real investors.

Options:

- Think of it as an investment toolkit, you need to use the right tool.

- Options can’t be used on every trade, you’ll blow your account up.

- Key is to stay around as long as possible, but put up real money when you have very high conviction opportunities. You have to be very patient.

- There is a limited number of good companies. Investors that do really well have a maximum of 30-40 stocks that they’re watching. Focus on what you’re good at and what’s working.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.