https://youtu.be/_yT4U0x1NP4

How Grizzleton Works

We built the Grizzleton concept to show consumers they can recreate the amazing Peloton experience for a fraction of the cost.

Like many consumers, we love the Peloton equipment and classes but couldn’t stomach the costs.

With Grizzleton you can get the full Peloton experience, no compromises, for 70% off.

Here’s how it works.

Step 1: Buy a Sunny Exercise bike, the best reviewed third-party bike on the market.

Step 2: Buy a wireless cycling computer and heart rate monitor to mimic Peloton’s analytics

Step 3: Sign up for Peloton Digital for $19.99 per month which you can then stream to any device in your home.

You’ve now recreated a no compromise Peloton experience for only $37 a month compared to $112 a month from Peloton.

Over three years Grizzleton will save you $2,700 or 70%. This is not chump change.

| Peloton | Grizzleton | Savings | |

| Bike | $2,592 | $335 | 87% |

| Year 1 Classes | $480 | $240 | 50% |

| Cycling Computer | $0 | $250 | |

| Heart Rate Monitor | $0 | $30 | |

| Year 1 Cost | $3,072 | $855 | 72% |

| Year 2 Cost | $480 | $240 | 50% |

| Year 3 Cost | $480 | $240 | 50% |

| Total | $4,032 | $1,334 | 67% |

Grizzleton + A Digital First Strategy = A Stock in Trouble

Grizzleton may not be a real product, but it vividly demonstrates one of the many risks facing the company.

The Peloton experience is easy to copy.

For one, any consumer can pay $19.99 per month for Peloton digital and with a few additional pieces of equipment recreate 99% of the experience for much less money.

Peloton digital deprives Peloton of fat margins on the bike and the $39.99 monthly fee for on-bike classes.

Competitors are also hot on Peloton’s heels.

Flywheel offers the same quality equipment and a similar digital experience for 15% less.

Technogym, provider of gym equipment to the Olympics, is rolling out a similar digital experience for gym owners, making the purchase of a home bike harder to justify when you can have the same experience by buying a cheaper gym membership.

Here at Grizzle we realized early on the Peloton IPO was never going to go well at a $10 billion valuation ($28/sh).

This is an exercise equipment company after all.

Looking at all the competitor products out there got us thinking.

What if Peloton ultimately becomes a revolutionary digital exercise app, but not the preferred equipment provider.

Peloton would now look more like Netflix than BowFlex.

So we went on an analytical adventure to see if Peloton, the streaming service, is actually a bargain even though Peloton in its current form looks like a dud.

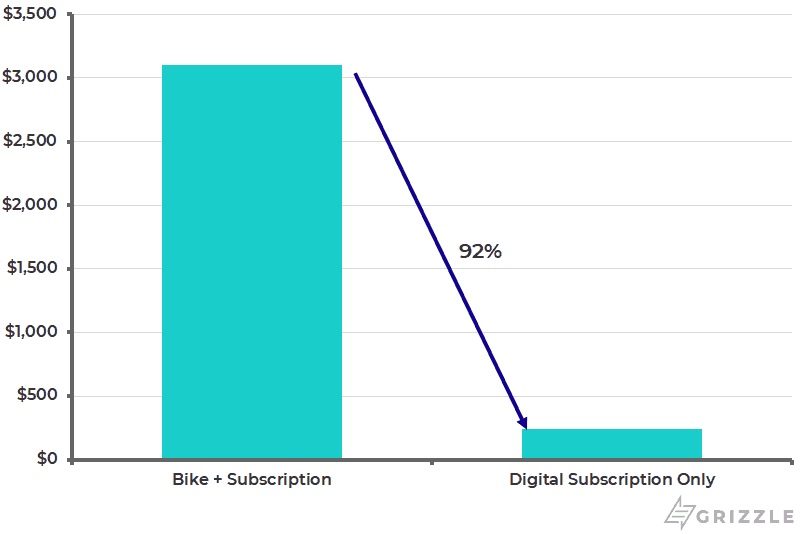

Right now, a new Peloton member pays $2,600 for the bike and another $40 a month for the digital classes, generating ~$3,100 for Peloton in year 1.

If consumers start using Peloton for the digital classes only and buy equipment elsewhere, year 1 revenue would fall to $240 or 92% less.

Peloton could become a victim of its own success.

Year 1 Cost of a Bike + Membership vs Peloton Digital

Be Careful What you Wish For

Peloton CEO John Foley has gone out of his way to sell Peloton as a tech-heavy disruptor.

Foley wants us to think of Peloton as a media company, technology platform, and even an experience.

Exercise equipment is just an afterthought.

Peloton’s Message to Investors

If CEO Foley has his way Peloton will become a media streaming service, just like Netflix, Amazon Prime, Disney+, and the rest.

So lets say Foley’s dream comes true; what does Peloton the media streaming juggernaut look like?

Read on to find out.

As a Major Streaming Service, Peloton is Only Worth $6.00/sh

What if John Foley pulls off the greatest fitness company transformation in history, remaking Peloton into the largest fitness streaming service in the world.

This sounds like a win at first glance, but in reality Peloton would be leaving one tough business for another.

The streaming market is already competitive and will only heat up this winter with both Apple and Disney launching new streaming services to rival Netflix.

Looking at the pricing of rival streaming services, Peloton’s $19.99 price point will have to fall.

How could Peloton justify charging customers 50%-180% more than Netflix, Amazon Prime, and Disney when these services match or exceed Peloton in content quality and quantity.

At best we think Peloton’s digital pricing would eventually fall to match streaming competitors at $12.99 per month.

Peloton Prices are Too High for a Streaming Service

| Streaming Provider | Monthly Cost | Subscribers (mm) |

| Peloton | $19.99 | 0.6 |

| Netflix | $12.99 | 151 |

| Amazon Prime | $12.99 | 105 |

| Hulu | $11.99 | 31 |

| Disney+ | $6.99 | 29 |

| Apple TV | $4.99 | ? |

| ESPN+ | $4.99 | 2 |

| Subscribers Needed to Justify an $11.5 Bn Valuation | |

| Current Market Cap (mm) | ~11,500 |

| Mature P/E Multiple | 16x |

| Implied Net Income (mm) | $714 |

| Net Income Margin | 8% |

| Implied Revenue (mm) | $5,980 |

| Streaming Cost/Month | $12.99 |

| Total Subscribers (mm) | 55 |

55 million people would represent 91% of gym memberships in America and 83% of the total addressable market (TAM) for Peloton according to management.

The probability that Peloton goes from 610,000 members to becoming a larger streaming service than Hulu and Disney+ is so remote, its not even worth betting on.

Even if we assume Peloton increases their market share from 1% today to 15% or 10 million subscribers, 16x more than they have today, the stock is only worth $6.00/sh as a mature exercise streaming company.

As a result of our new analysis we think the downside for Peloton is even more significant than the $14.00 target we listed previously in our IPO guide.

*Detailed assumptions are at the bottom of the article

| Value of Peloton with 10 million Digital Subscribers | All in Millions |

| Subscribers | 10 |

| Monthly | $12.99 |

| Revenue | $1,558 |

| Gross Margin % | 45% |

| Gross Margin | $701 |

| Payroll | $62 |

| Research & Development | $124 |

| Marketing | $342 |

| Net Income | $128 |

| Steady State P/E | 16x |

| Steady State Market Cap | $2,091 |

| Steady State Stock Price | $6.00 |

Peloton’s Stock Price is in Trouble No Matter What

If Peloton remains an exercise equipment company, it must sign up 40% of U.S. households with a gym membership just to keep the stock price flat.

If Peloton reorganizes into a content first exercise streaming platform, the bar is just as high.

Either they add 38 million subscribers, 60% of the entire addressable market, or the stock is going lower.

If you challenge Peloton management on the current stock price, they no doubt will tell you you’re looking at the company the wrong way.

All we can say is Grizzle looked at Peloton every which way and we still couldn’t find a business model worth anywhere near the current stock price.

We recommend investors hop on a bike, take a class and feel the burn, but stay far away from your brokerage account.

Peloton is shaping up to be a fitness investing fad for the ages.

Assumptions

Payroll: In line with Netflix G&A as a % of revenue

Marketing Expenses: Similar acquisition cost per subscriber to Netflix ($100) however the churn rate in fitness is much higher than for streaming services (up to 50% in the first year, we assume 35% a year for Peloton Digital) making the overall marketing costs per subscriber about twice as high as Netflix as a % of revenue.

Research and Development: In line with Netflix as a % of revenue

Tax Rate: 25% corporate tax rate

Mature P/E Multiple: While some tech companies like Netflix and Amazon trade at P/E multiples as high as 50x, they are also growing revenue at 20%+ a year. A mature Peloton would no longer be growing and we think will have a P/E ratio of 16x at that point, in line with a no-growth tech company like Apple.

Gross Margin: We assume Peloton generates a 45% gross margin, 20%-50% higher than Netflix because of lower content costs. Netflix hires movie stars while Peloton can hire unknown fitness talent for much less, giving them a cost advantage.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.