GrowGeneration (NASDAQ:GRWG) has posted their annual results early for fiscal 2019.

Revenue was $79.7M which beat analysts’ estimates of $76.1M

Adjusted EBITDA was in-line with estimates, coming in at $6.6M

GrowGeneration manufactures and sells hydroponics equipment mainly used for the cultivation of cannabis and is a leading supplier in the US which does business with many marijuana producers across the country.

GrowGeneration has been deemed an “essential” service in the current COVID-19 outbreak and its facilities remain open and operational in midst of the shutdown of businesses across the US.

The company has issued the following guidance for 2020, which has been updated to reflect the changing conditions that have occurred in recent times:

- Revenue guidance: $130M-$135M

- Adjusted EBITDA guidance for 2020 is $11.5M-$13.5M

- Revenue guidance for Q1 2020 is $31.5M-$32.5M

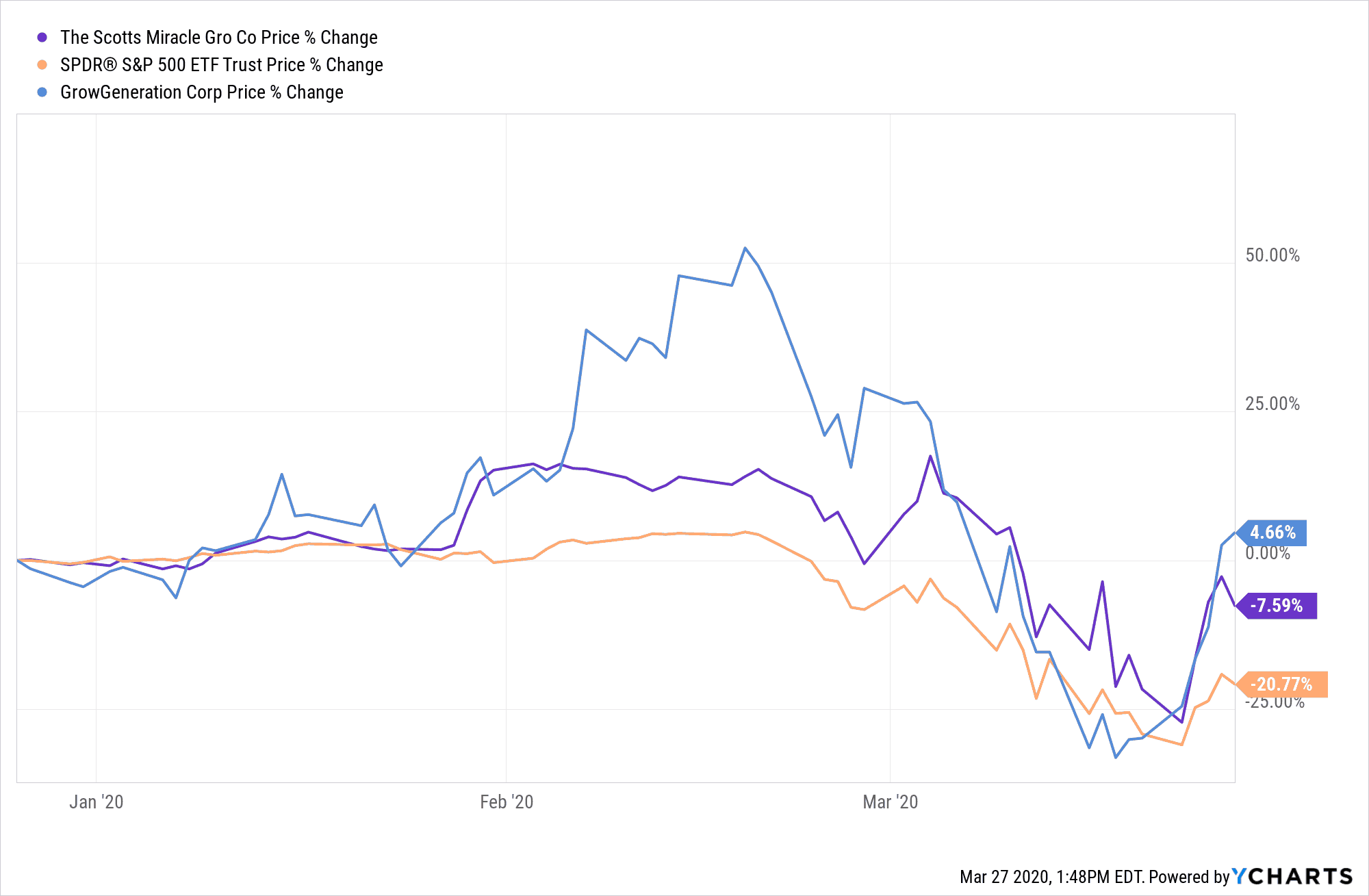

GRWG Has Fared Well In The Current Crisis So Far

Taking a look at the price chart for GRWG, we see that in terms of stock price, it has outperfomed the S&P500 as well as competitors like Scott’s Miracle Gro (SMG) (which owns Hawthrone Gardening) since the crisis began.

Last month, we did a detailed deep dive comparing GRWG to Scott’s Miracle Gro and it is clear that GRWG although being a much smaller company than SMG, is growing much faster rates.

This report shows that GRWG is able to beat expectations and continue their rapid rate of growth during normal times.

However, we will have to see how well GRWG will fare after recent events.

If the current crisis turns into a drawn out recession, it may hit smaller companies like GRWG harder than a bigger company like SMG who has more cash on hand.

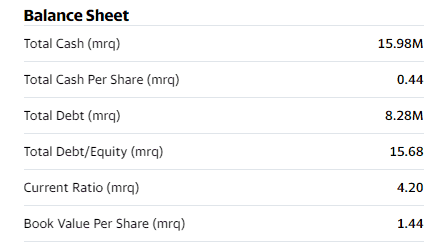

Although GRWG is not in any immediate danger of running out of cash as the company still has almost $16M of cash on hand which at first may not sound like a lot, but is actually a decent amount for a company of its size.

Keep in mind that this amount of cash represents more money than their total debts. And its current ratio sits at above 4.

It is another positive sign that they will be able to weather any immediate danger for now.

Earlier we saw Scott’s Miracle-Gro’s preliminary report on their latest quarter which has just ended now.

In the press release, SMG stated that their Hawthrone Gardening segment, the part of the business which directly competes with GRWG, is expected to have a 55% sales increase compared to last quarter.

This is a positive sign for next time GRWG releases their results for this current quarter, as the past has proven that market is big enough to be a non-zero sum game, meaning that there is room for growth for both companies, and if one does well, usually that means so will the other.

Commenting on the plan going forward in midst of the coronavirus crisis, the management has stated that they will pause external expansion and for now and only focus on internal growth by expanding deployment private label products building out their “Buy Online, Pick Up In-Store” service.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.