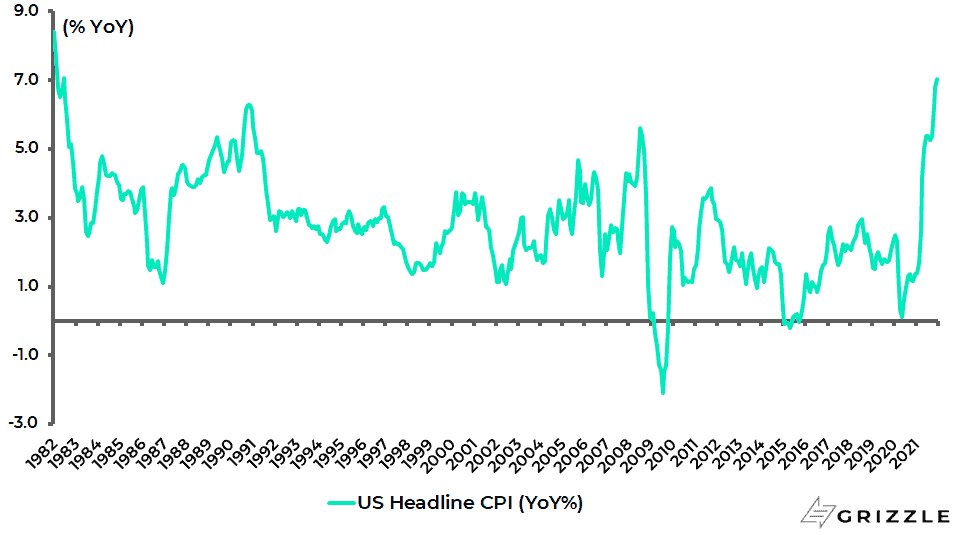

The change in equity market leadership looks ever more pronounced in terms of the shift from growth to value stocks as investors have continued to discount more rate hikes following last week’s 7.9% YoY US CPI report for February.

US CPI inflation

Source: Bureau of Labor Statistics

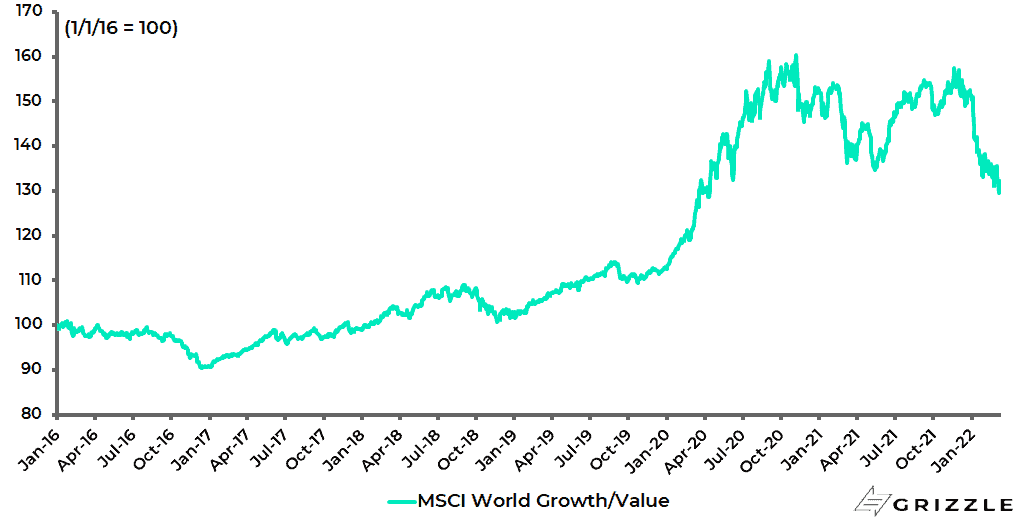

Value stocks have now outperformed growth stocks by 21.2% since mid-November.

MSCI World Value Index relative to MSCI World Growth Index

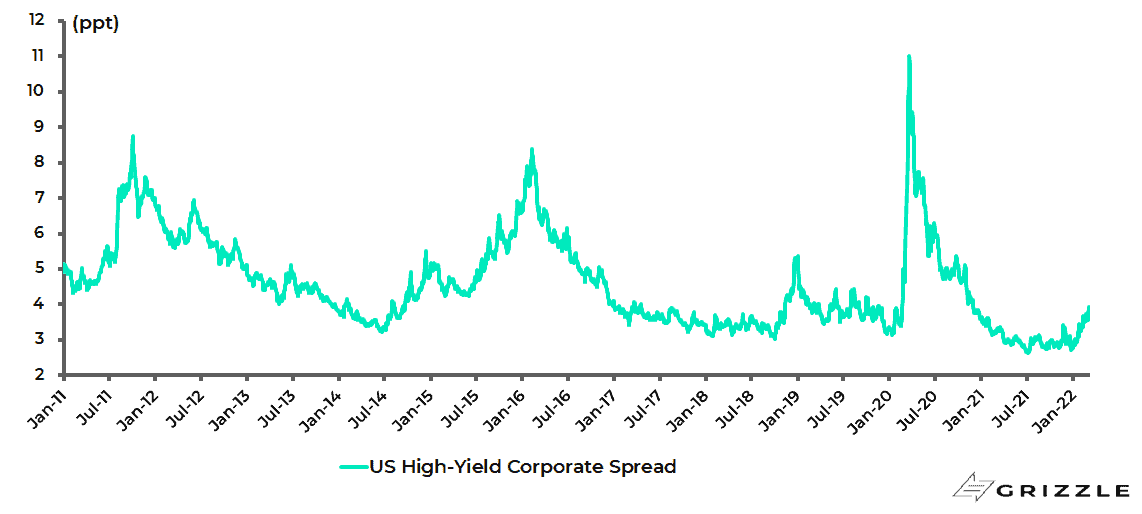

Money markets are now discounting 168bp of Fed tightening in 2022 while credit spreads have continued to widen, a process that surely can continue so long as the Fed is perceived to be behind the curve.

The US high-yield corporate bond yield spread has now risen from 2.71% in late December to 3.94%, the highest level since December 2020.

US high-yield corporate bond yield spread

Overall, the current situation can best be summarised as the inverse of Goldilocks.

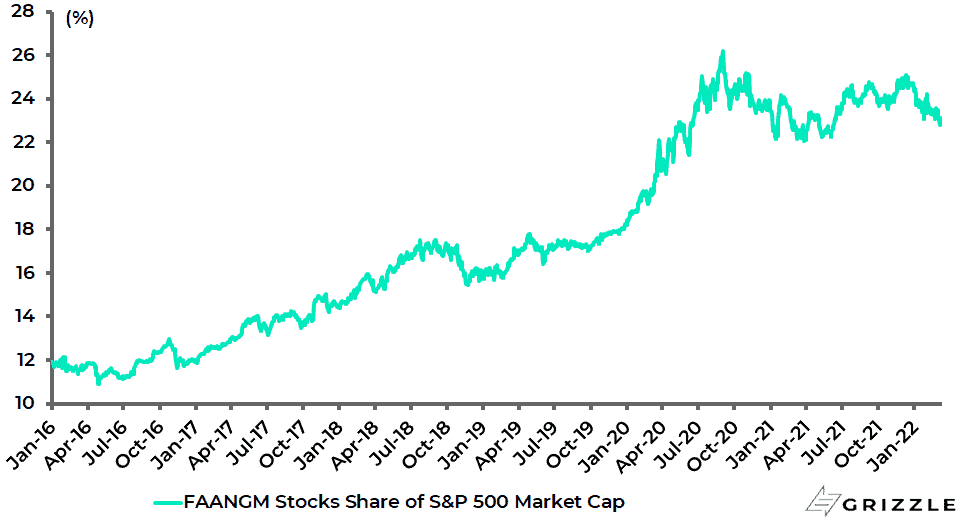

It also continues to look ever more the case that the FANG stocks peaked as a percentage of S&P500 market cap back in the summer of 2020.

In this respect, the rotation out of growth stocks will probably not be completed until the leaders of the bull market (i.e. the FANG stocks) succumb in a more decisive fashion.

US Big Tech’s share of S&P500 market cap

The 2000 Nasdaq rout could be a useful precedent here since the dotcoms collapsed first, with the Nasdaq Composite turning down from March 2000.

But it took another six months before the S&P500 started to decline.

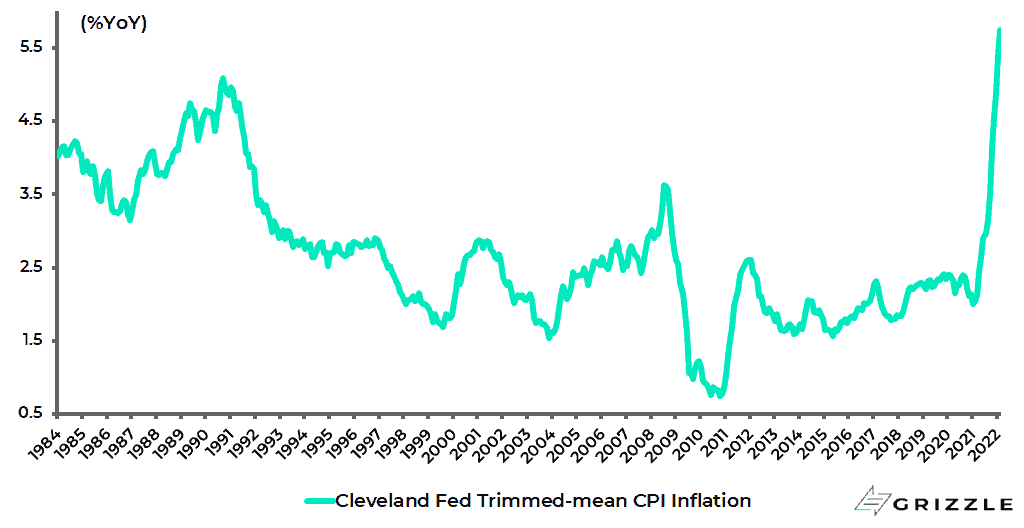

As for the details of the latest CPI inflation print, the Cleveland Fed’s trimmed-mean CPI remains a useful indicator of broadening inflationary pressures.

The trimmed mean CPI inflation rose from 5.42% YoY in January to 5.75% YoY in February, the highest level since the data series began in December 1983.

Cleveland Fed’s US trimmed-mean CPI inflation

Monetary Tightening Not Just About Rates Anymore

Investors should also remember that monetary tightening is not only about rate hikes but also about balance sheet reduction.

And, as discussed here previously (see Bond Investors Should Zig When the Fed Zags, 7 February 2022), quantitative tightening is in many respects a blunter instrument and a process more likely to spook markets.

On this point, it is worth highlighting a speech made by Esther George, president of the Federal Reserve Bank of Kansas City, on 31 January.

The speech, in this writer’s view, provides the clearest summary of the argument for moving forward with balance sheet reduction sooner than in the previous monetary tightening cycle in 2017-19 (see Esther George’s speech to the Economic Club of Indiana: “The Economic Outlook and Monetary Policy”, 31 January 2022).

In her speech, George noted that the potential costs associated with an “excessively large” balance sheet should not be ignored.

She cited, first, the “distortive” effects in the financial system.

Second, maintaining a large balance sheet reduces the “available policy space” in the next downturn and, third, a large balance sheet has the potential to “intertwine fiscal and monetary policy in the public’s eyes”.

In this writer’s view, such an outcome has already happened, which is why it has long been concluded here that the Powell Fed implemented a policy of MMT lite during the pandemic.

Still, it is interesting that George went on to state that the above risk would become more apparent as “interest paid on the large stock of reserve liabilities grows”.

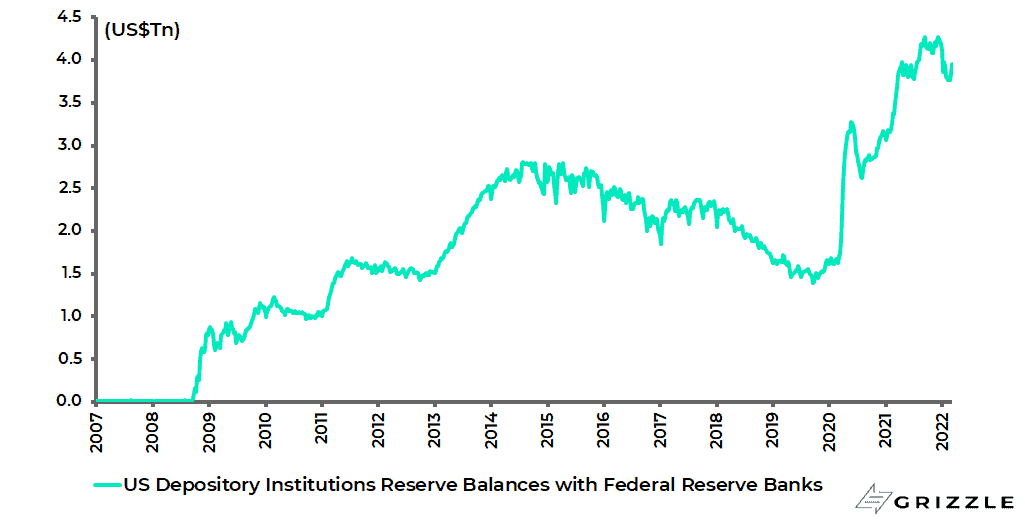

This is a reference to the potentially politically explosive issue of commercial banks being paid a rising amount of interest on their reserves in a Fed tightening cycle.

Thus if, say, the Fed hikes 150bps this year, in line with current money market expectations, that means by the end of the year the banks will be receiving an annualised US$65bn in interest income based on their current reserves of US$3.96trn and an assumed Interest of Reserve Balance (IORB) rate of 1.65% (the current IOBR rate is 0.15%).

US Bank Reserves at the Fed

Shrinking the Fed Balance Sheet Could be Preferred to More Interest Rate Increases

As discussed here previously (see When Does The Stock Market Trigger The Infamous Fed “Put”?, 28 February 2022), George also noted that more aggressive action on the balance sheet could allow for “a shallower path for the policy rate”.

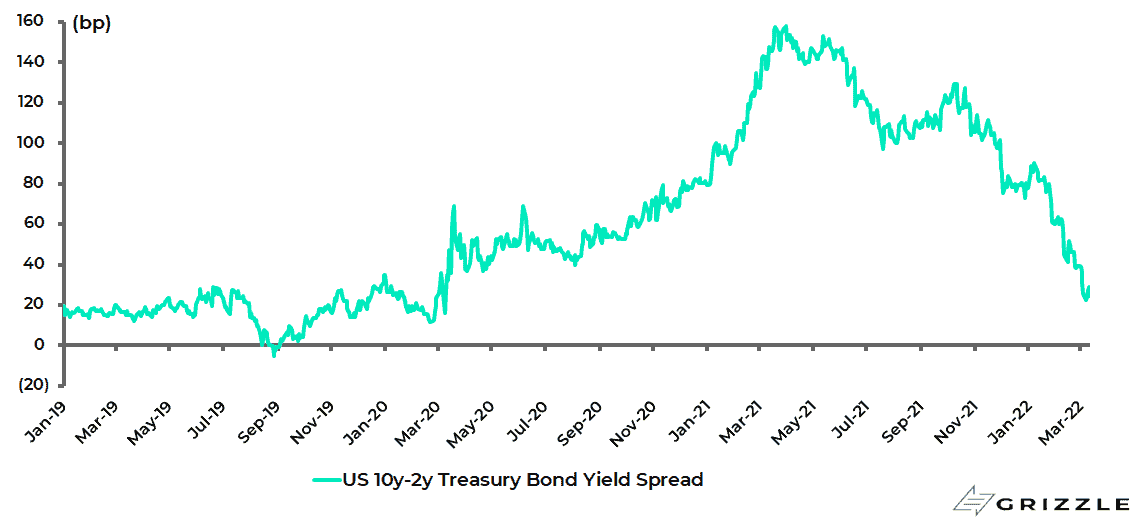

It certainly is the case that the yield curve has been flattening of late.

The spread between the 10-year and the 2-year Treasury bond yields has declined from 90bp on 7 January to only 24bp.

US 10Y-2Y Treasury bond yield spread

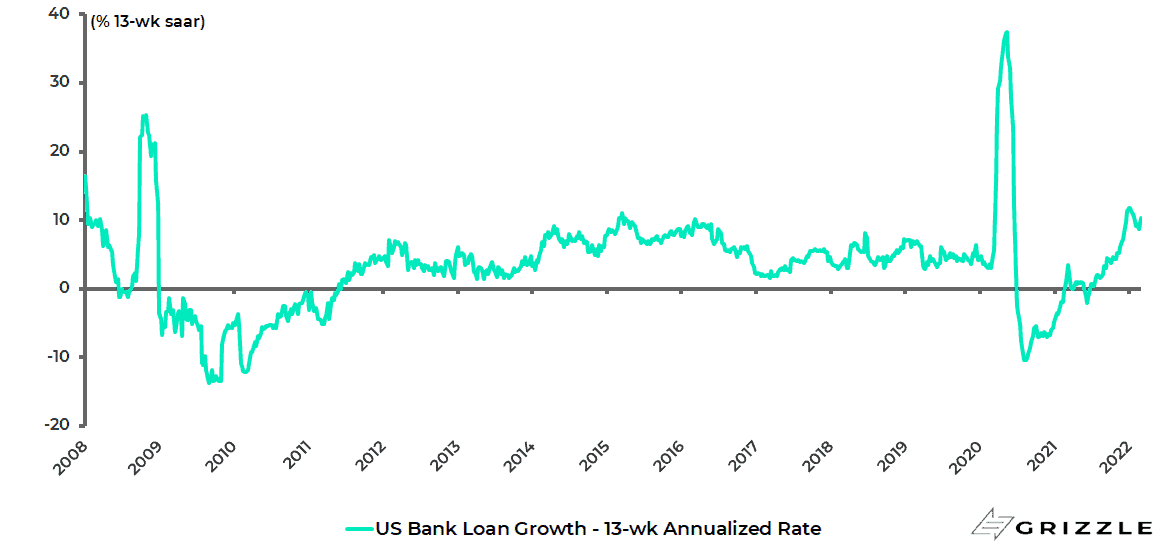

Still, it is also true that US bank lending has been picking up in recent months, though it has slowed somewhat of late.

US bank loans rose by an annualised 11.8% in the 13 weeks ended 29 December, the highest annualised growth rate since 2008 if the pandemic-triggered surge in 2020 is excluded, and were up an annualised 10.3% in the 13 weeks ended 2 March.

US bank loan growth: 13-week annualised rate

Source: Federal Reserve

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.