Bottom Line:

Over the last three years, a majority of capital in the cannabis industry has gone to fund growers, retailers, and extractors, but there may be an underappreciated investing opportunity to own companies operating in the middle of the market.

If we think of cannabis growers as the gold miners of the industry, the equipment providers are the middlemen selling the picks and shovels (dirt and lights) that make cannabis cultivation possible.

The two biggest U.S. providers of equipment and supplies for the cannabis industry are GrowGeneration (NASDAQ:GRWG) and Scott’s Miracle-Gro (NYSE:SMG).

In this deep-dive report, we compare GRWG and SMG to each other and the greater industry to see if investors are missing two gems among a cave full of trinkets.

Everyone Loves A Good Origin Story – GrowGeneration Corp (GRWG)

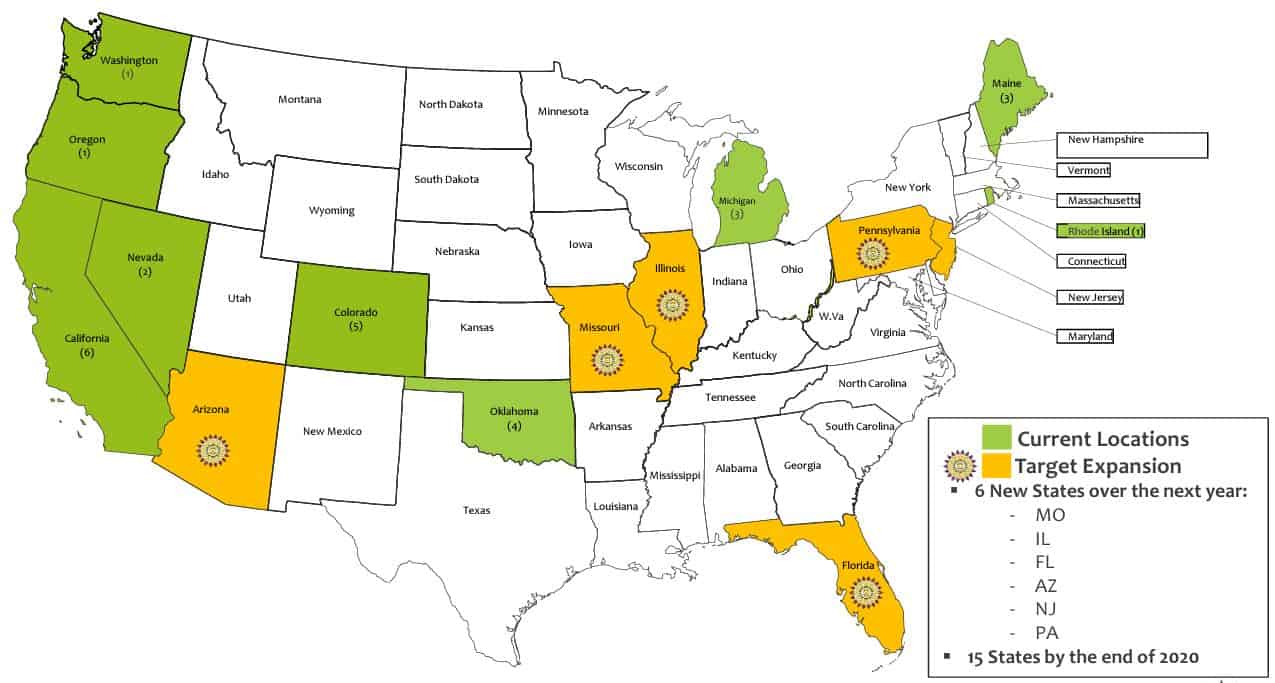

GrowGeneration Corp, based out of Denver, Colorado, is a supplier of hydroponic equipment in the United States.

Starting in Colorado, GRWG has grown to a 9-state footprint with stores in Nevada, Oregon, California, Washington State, Oklahoma, Michigan, Rhode Island, Maine, and New Hampshire.

Currently, the company makes about $80 million in revenue as of December and is expected to grow 70% in 2020.

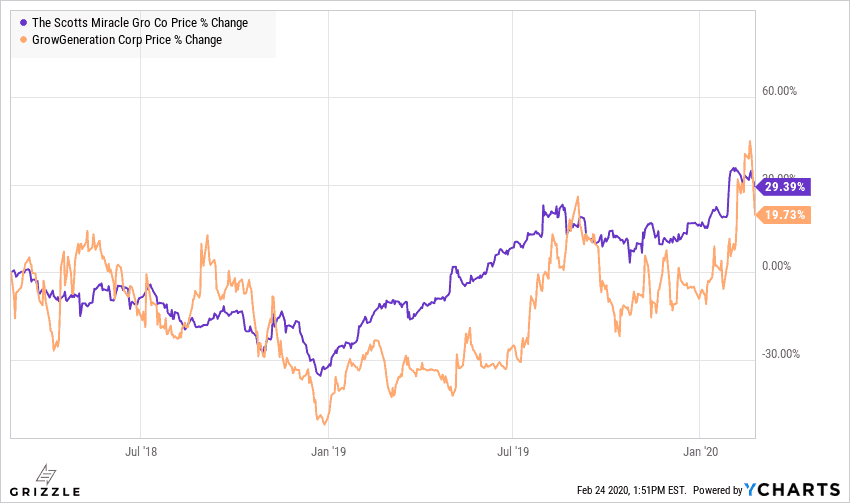

The stock has performed well and has almost doubled since the same time last year.

This is especially impressive given that during the same time the cannabis growing industry has been absolutely decimated in the stock market; with the Horizons Marijuana Life Sciences ETF (TSE:HMMJ) declining by more than 50% since the same time last year.

GrowGeneration has been matching Scott’s stock performance over the past two years, which is impressive given the meltdown in the cannabis sector and GrowGeneration’s inferior access to capital (cash and debt).

Stock Performance (SMG vs GRWG)

Established and Diversified – Scott’s Miracle-Gro (SMG)

Scott’s Miracle-Gro is one of the oldest companies in America. It was founded in Marysville, Ohio in 1868 and originally focused on selling lawn seeds.

Throughout the years, the company has tried to diversify its business and has recently delved head-first into the cannabis industry by establishing a subsidiary, the Hawthorne Gardening Company, which caters to cannabis growers by selling them hydroponic and other related equipment needed for cannabis.

In contrast to GRWG, Scott’s Miracle-Gro is a much larger company and the cannabis industry is not the only market they serve.

The cannabis-focused Hawthorne segment represents slightly more than half of the company’s revenues.

So while Scott’s cannabis supply segment is growing 14% compared to the legacy business at 2%, the overall exposure to cannabis won’t exceed 65% over the next 3 years compared to GRWG which is 100% focused on cannabis all day every day.

The market has applauded Scott’s move into the cannabis space, driving the stock up more than 50% in the last year and 30% since they purchased the largest hydroponic distributor in North America.

GRWG vs. SMG, By the Numbers

Now let’s compare these two companies on all the metrics that matter to figure out which one is the better buy.

The first metric is growth.

Over the long term over 60% of a stock’s price movement can be explained by its revenue growth, making this a key metric to understand.

The law of large numbers is clearly visible in the comparison between these two companies. When a company is small, it is easy to put up insanely high growth rates, but that growth will inevitably slow down as the company gets larger and larger.

GRWG is a far superior company when we look at growth.

Analysts estimate GRWG will grow 73% in 2020 compared to Scott’s at an anemic ~5%.

GRWG will continue to be the hands-down winner on growth.

Growth

| Grow Generation (GRWG) | Scott’s Miracle-Gro (SMG) | Hawthorne Gardening Company Only | |

| Revenue Growth 2020 (Expected) | 72.68% | 4.75% | 12%-15% |

| EBITDA Growth 2020 (Expected) | 120% | 2.63% | N/A |

Cash Flow + Liquidity

Taking a look at the numbers for cash flow, we see that GRWG is still free cash flow negative on a trailing 12-month basis.

This is not uncommon for a small-cap cannabis startup, however, in contrast to SMG generating positive cashflow, GRWG is definitely a riskier bet.

But does GRWG’s revenue growth potential overshadow the balance sheet risk?

We think the answer is yes.

At the current cash burn rate GRWG has 1 year before it would need to raise more money if it continues to buy up other companies.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]If GRWG shuts down the acquisition pipeline it will have 3.5 years of cash left, more than enough time to generate positive cashflow. [/su_panel]Cashflow Measures for GRWG and SMG

| GrowGeneration (GRWG) | Scott’s Miracle-Gro (SMG) | |

| Annual Cashflow | ($3.8M) | $114M |

| Cash Flow from Operations % of Revenue (LTM) | (2.40%) | 4.40% |

| Free Cash Flow % of Revenue (LTM) | (4.7%) | 3.50% |

| Gross Margin | 27% | 32% |

| Debt/EBITDA (LTM) | 2.2x | 2.7x |

| Years of Cash Left | 1 (w M&A), 3.5 (No M&A) | Profitable |

It is extremely unlikely GRWG will cut their investment spending anytime soon as they depend on the acquisition pipeline and building new stores to fuel their growth rates.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Current stores are growing sales at 36% and the company estimates these same stores can grow revenue 20% a year looking forward. This tells us GRWG’s overall revenue growth rate would fall to 20% next year, from the 62% the market expects, if they stopped buying or building new stores.[/su_panel]In the base case we should assume that they at least keep their current M&A spend rate which would give them about a year of cash runway.

If GRWG starts running low on cash, they will have to raise money with new debt or issue more shares which dilutes current shareholders.

Shareholders need to keep the dilution risk in mind when choosing to buy GRWG over SMG.

SMG is already profitable so cash flow is not a problem.

SMG’s liquidity profile is its strongest selling point against GRWG.

Valuation

From a valuation standpoint, GRWG looks like the hands-down winner as well.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Though GrowGeneration’s price to earnings multiple is 20% more expensive than Scott’s Miracle-Gro based on next year’s earnings, by 2022 GrowGeneration will be 20% cheaper than Scott’s if both stocks stay flat from now until then. GRWG looking like a bargain for those willing to look more than a few months into the future. [/su_panel]The higher growth of GRWG is worth taking on a bit more risk.

Valuation of SMG vs GRWG

| GrowGeneration (GRWG) | Scott’s Miracle-Gro (SMG) | |

| Revenue (TTM) | $80M | $3,224M |

| Price/Earnings 2020E | 25x | 21x |

| Price/Sales 2020E | 1.5x | 1.9x |

| P/E 2022E | 15x | 19x |

| P/S 2022E | 0.9x | 1.9x |

Comparison to Canadian LPs

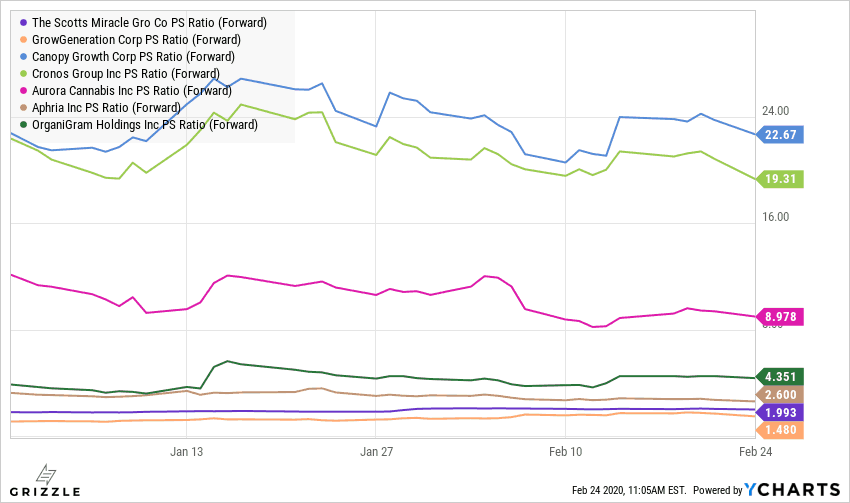

The valuation of GRWG against SMG is one thing, but we also need to compare them both to the cannabis growers to see if these equipment suppliers are really a bargain.

We see that the cannabis equipment sellers, GRWG and SMG, trade at some of the lowest forward P/S ratios in the entire cannabis industry.

This is further evidence that investors have been unjustifiably ignoring the equipment manufacturers and focusing more attention on the growers.

Investors should also keep in mind that unlike growers, equipment manufacturers are somewhat shielded from the price wars that have plagued the cannabis industry.

A crash in cannabis prices will not affect the equipment providers half as much because every grower that is still solvent still needs lighting, fertilizer, and dirt.

Forward Price to Sales

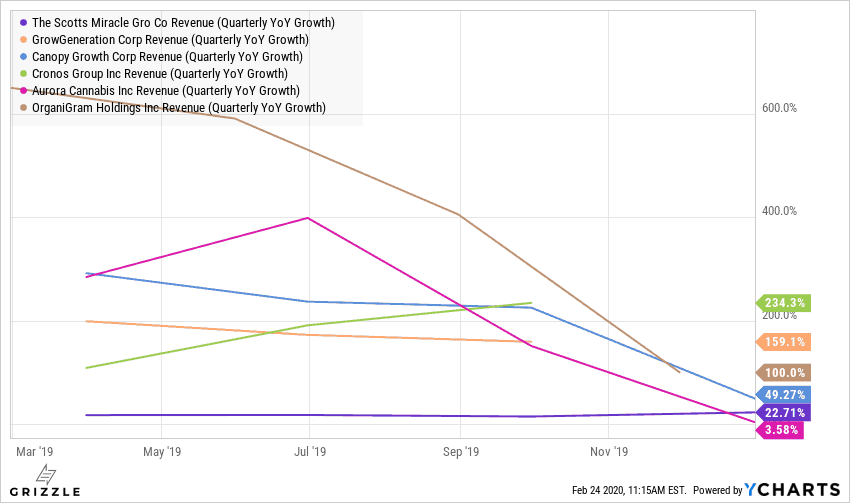

The price to sales ratio discount could easily be explained if GRWG and SMG’s growth rates were much worse than the cannabis growers, however, that doesn’t seem to be the case.

The growth rate of GRWG actually exceeds many of the growers who are dealing with declining prices and a stubborn black market.

Even Scott’s Miracle-Gro has caught up to some of the Canadian LPs who are stuck fighting among themselves for a piece of the painfully slow-growing legal market.

Sales Growth vs the Cannabis Growers

So Which Do I Buy? SMG or GRWG

After looking at all the angles, we think GRWG offers far more promise due to its higher growth rate and cheap future multiple.

However, the risk of further stock issuance from dwindling cash reserves or ramped up capital spending is not a joke, which speaks to the value of owning a profitable, although slower growing Scott’s as well.

Our preferred way to invest in both is to split your capital 70/30 between GRWG and SMG for a good balance of liquidity, cashflow, and growth.

Both stocks are a compelling play on the eventual legalization of cannabis in America.

Regardless of what happens with prices, as long as medical and recreational legalization marches forward, demand for growing equipment will as well.

With GRWG down 12% as we write this, investors who look past the negative headlines in Canada may have just found a discounted way to buy into the most promising consumer goods market in the world.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.