Cannabis drug provider GW Pharmaceuticals (NASDAQ: GWPH) reported earnings that severely disappointed against investor’s expectations

The market will likely be nonplussed by these results and will look for positive color on future clinical trials before bidding the stock up any more than the broader cannabis market, which faces its own headwinds.

Revenue came in at $109 million, 3% better than consensus of $106 million and in-line with guidance of $108 million.

Revenue was up 16% from last quarter and is on a $436 million run-rate compared to consensus for revenue of $534 million in 2020.

The EPS loss of -$0.07/sh was almost double the -$0.03/sh loss analysts were expecting and will likely not be taken well by the market.

Moving farther up the income statement, the EBITDA loss of $11 million also missed the analyst estimates for a loss of $10 million.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]We expect GW Pharma will continue to follow the ups and down of cannabis producers like Canopy Growth, unless additional positive clinical trial results are released. There are potential catalysts on the horizon but the stock is still priced like a speculative biotech stock and should be treated with caution. Be prepared to lose 50% of any money you put into this name if the clinical trials dissapoint[/su_panel]

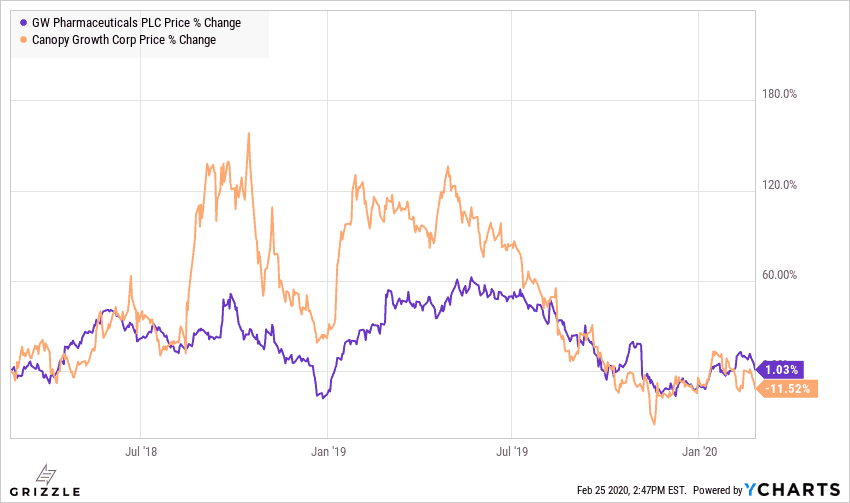

GW Pharma had a solid stock market run from the middle of 2017 to the middle of 2018 as investors and regulators were just beginning to acknowledge the pharmaceutical potential of cannabis.

However, since that point this stock has begun trading in lockstep with the broader cannabis industry which is currently in an acute downturn.

We expect GW Pharma will continue to follow the ups and down of cannabis producers like Canopy Growth, Cronos and Aphria unless additional positive clinical trial results are released.

GWPH Price Performance vs Canopy Growth

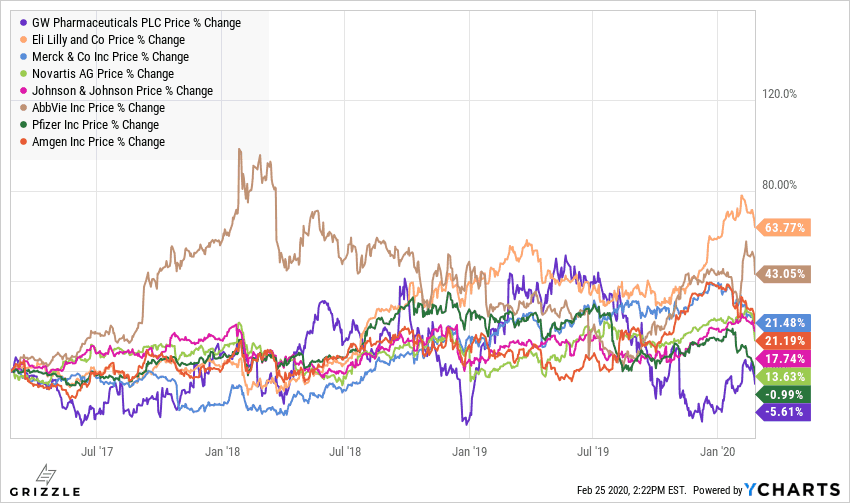

When comparing GW Pharma to the pharmaceutical giants, performance has been the worst in the group over the last three years even with significant clinical breakthroughs.

We think this is due to the market’s understanding that GW’s blockbuster drug Epidiolex still is too niche of a drug to drive revenue much higher on its own.

Performance of GWPH vs Big Pharma

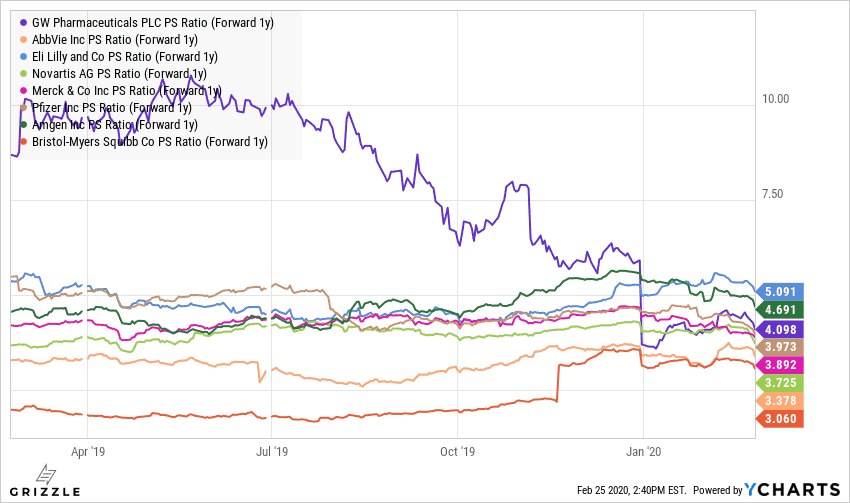

From a valuation perspective, GW Pharma looks fairly priced if we look at the price to sales vs pharma peers, however, sales do not tell the whole story.

GWPH Price to Sales vs Peers

GW Pharma is still generating cashflow losses, while big pharma peers are solidly profitable.

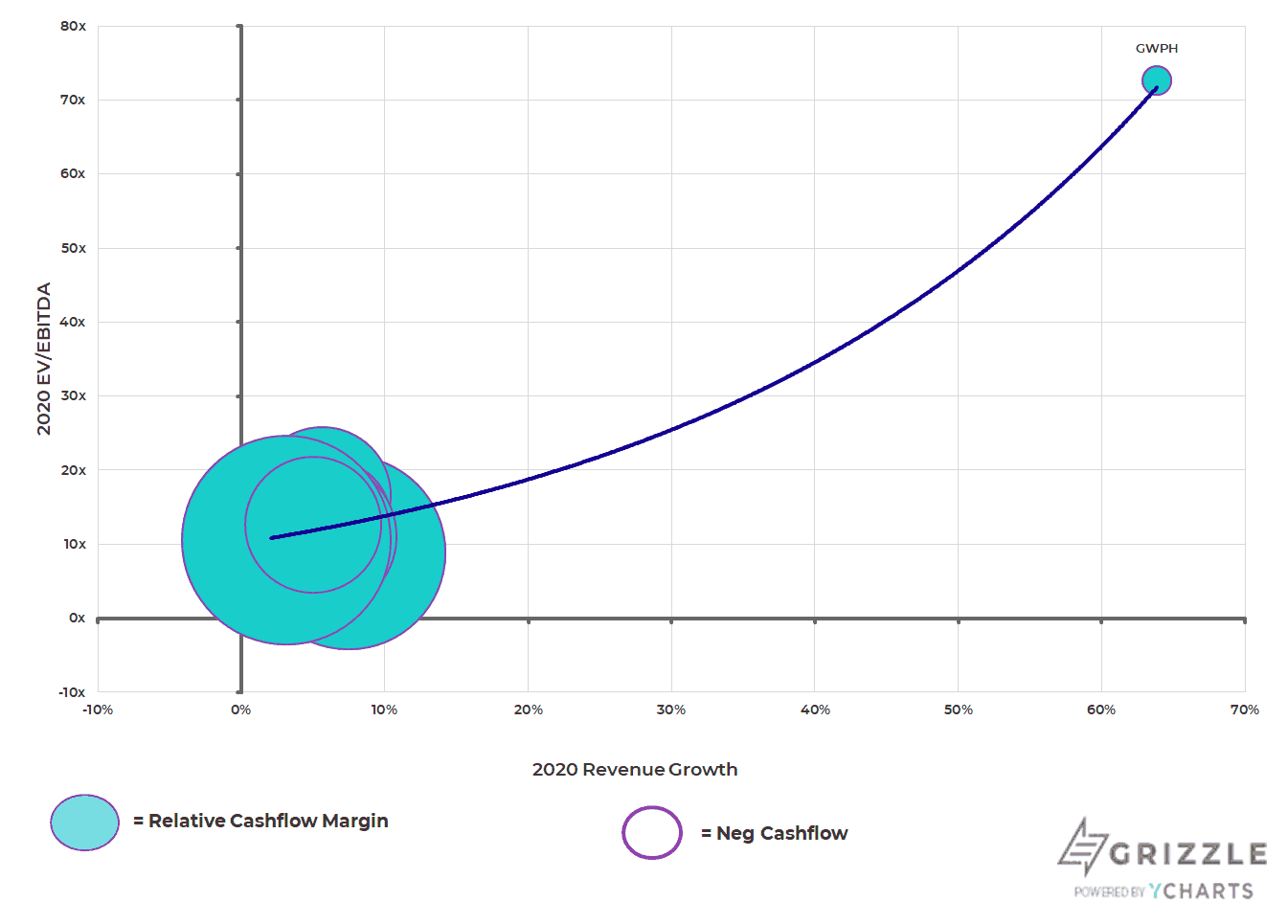

On a price to cashflow basis (also called EV/EBITDA), GW is priced right for its growth today.

But if the company isn’t able to show additional clinical successes and win more patents, slowing revenue growth would cause the multiple to shrink significantly.

GW Pharma is a speculative biotech stock offering investors big potential upside but also significant downside if everything doesn’t go right.

GWPH Price/ Growth Compared to Peers

The Stock Will Trade with the Broader Cannabis Market

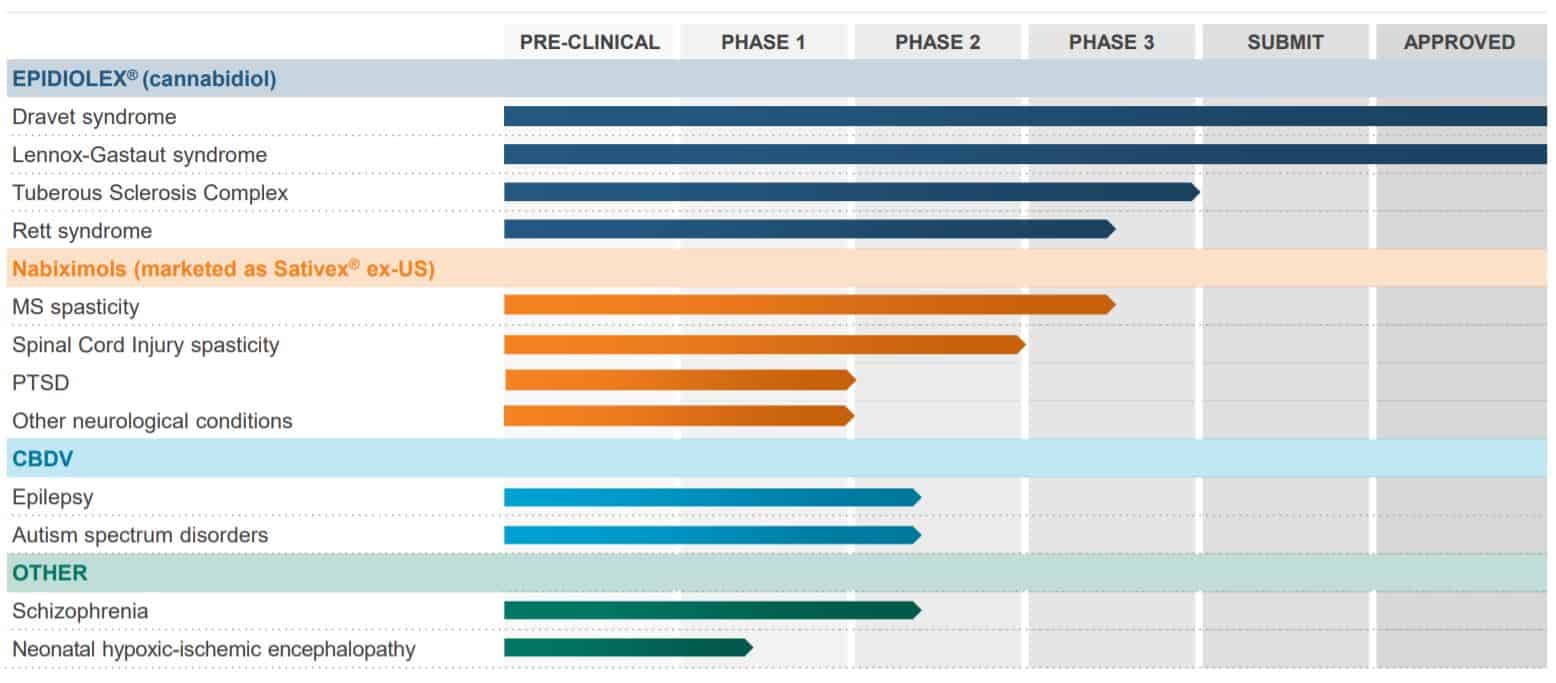

GW Pharma does have some promising clinical trial catalysts on the horizon, but trials take time.

In the meantime, this stock will follow the stock prices of the broader Canadian cannabis industry.

The cannabis industry is working through an oversupply and falling retail prices.

GW Pharma will fail to generate long term gains until the company can prove to investors, Epidiolex or Sativex can broaden their appeal to a wider range of patients than just those suffering from childhood epilepsy.

GW Pharma Clinical Trial Pipeline

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.