Harvest Health (CNSX: HARV, OTCMKTS: HRVSF) has posted their results for Q4 2019.

Revenue came in at $37.8M which missed analysts’ estimates of $39.45M

Adjusted EBITDA came in -$6.8M which missed estimates of -$3.23M

The company posted the following highlights for the Full Fiscal 2019 year:

- New capital raised during 2019 included short-term debt, unsecured convertible debt,

real estate backed debt, and senior secured debt totaling approximately $295 million. - Harvest added 21 retail locations through a combination of organic store openings,

acquisitions of operational retail locations, and addition of stores through managed

service agreements. At year end, Harvest owned, operated, or managed 31 retail locations

in six states, including 11 in Arizona. - Harvest was awarded licenses allowing for up to 10 additional revenue generating

facilities including cultivation and manufacturing facilities and retail dispensaries.

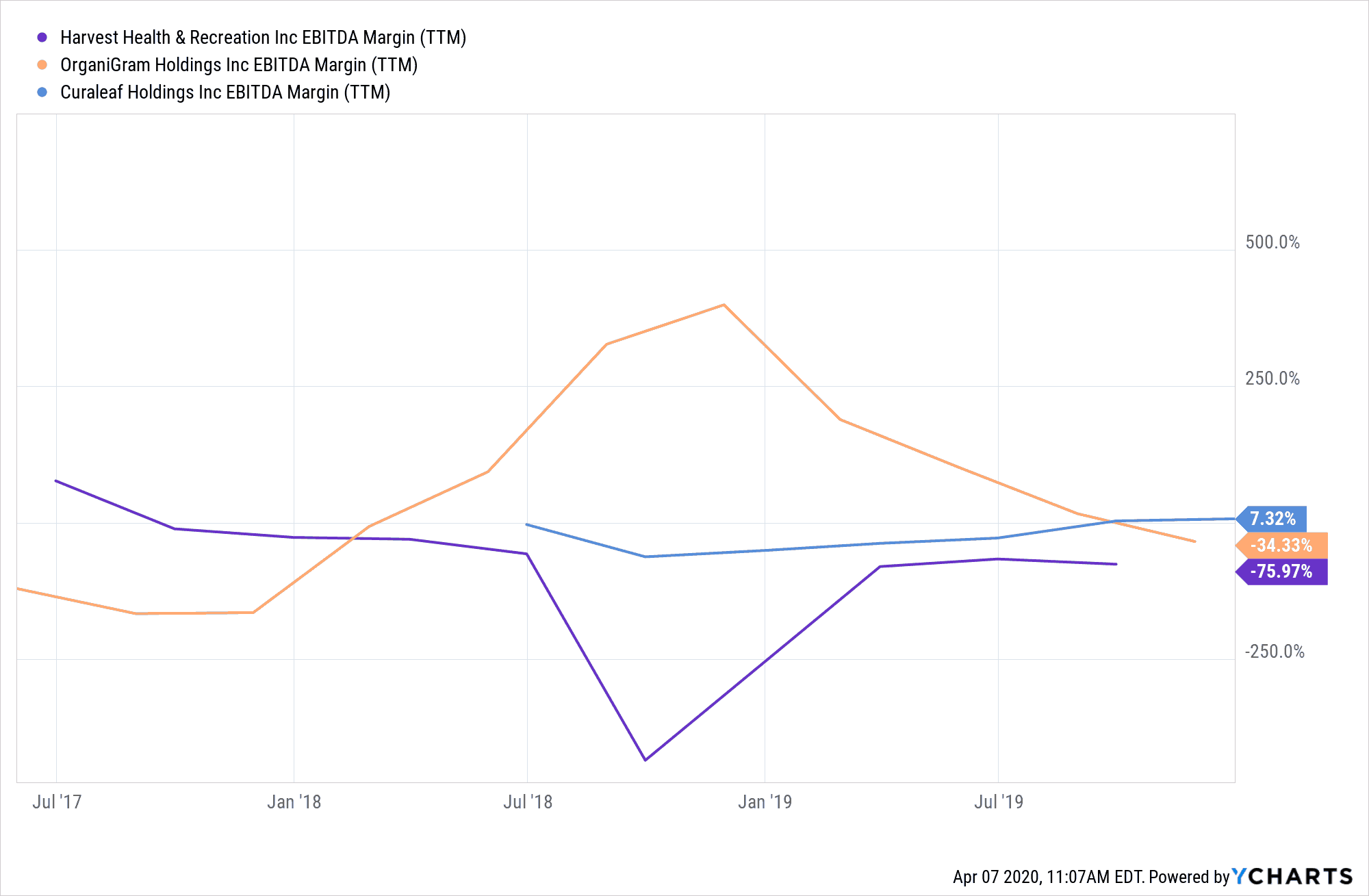

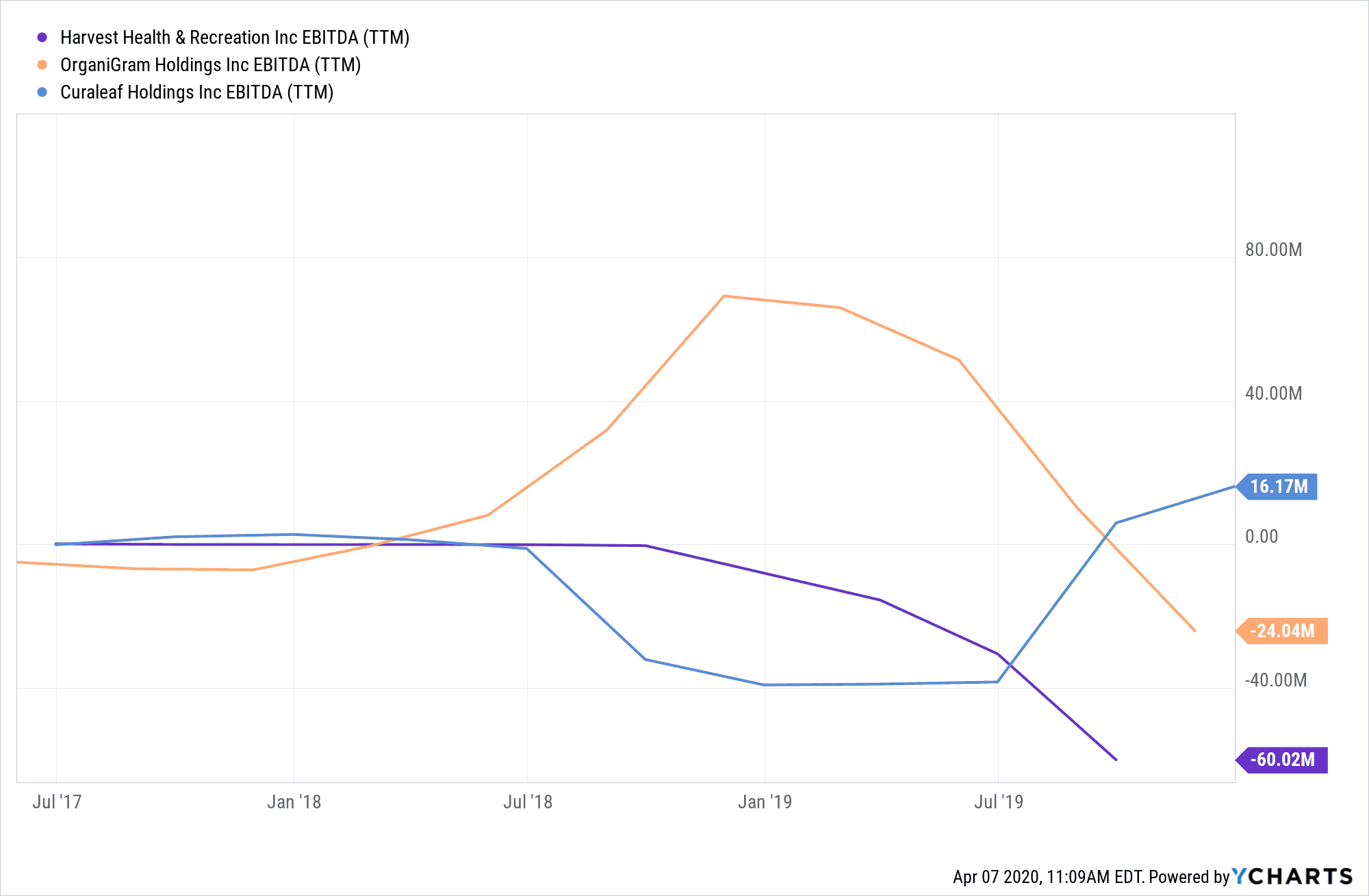

The stock has been obliterated in the markets for the past year, down more than 90% since a year ago. Unfortunately, looking at Harvest Health’s EBITDA Margin and EBITDA, it appears that the company is far from profitability, which may be part of the reason why investors have fled the stock.

EBITDA Margin

Trailing Twelve Months EBITDA

Failed Acquisitions Signal Uncertainty, And Investors Don’t Like That

Just a few weeks ago, Harvest Health announced that it had mutually agreed with Verano to terminate their previously planned merger valued at $850M.

Had this deal gone through, it would’ve been one of the largest mergers in the cannabis industry ever.

The company has cited the recent COVID-19 pandemic and the financial crisis that followed it as the main reason why it has agreed with Verano to terminate the deal.

The company also named some notable other reasons to terminate the deal, including:

- Prolonged obstacles in meeting requirements for state and local regulators needed to transfer ownership and operational license.

- Adverse capital market conditions.

- A challenging environment for asset sales.

Previously, we reported on Harvest Health’s lawsuit against Falcon International. In the lawsuit, Harvest Health alleged that Falcon had failed to provide them with auditable financial statements, and that multiple other legal obligations have failed to be met.

However, some analysts have speculated that the true reason for Harvest Health’s decision to backtrack on acquiring Falcon, was due to the tough operating environment and deterioration in market fundamentals in the cannabis industry in California.

Falcon then countersued Harvest Health, denying the allegations and suing for a $50M break free fee as described in the original contract.

The original lawsuit against Falcon was eventually dismissed by Harvest Health and instead the parties had agreed to send the dispute to the American Arbitration Association as of February 26, 2020, and the details of what came next remains unclear.

One of Harvest’s other planned acquisitions, a firm named CannaPharmacy, was scaled back to only include Franklin Labs, a subsidiary of CannaPharmacy in a deal valued at $25.5M

With this news on Verano dropping, none of the three of Harvest’s previously planned acquisitions happened the way that they originally intended them to.

Harvest hopes to break its string of bad luck with acquisitions as it has announced the completion of some smaller acquisitions including Interurban Capital Group which was completed on March 13, 2020 and Arizona Natural Selections which was completed on February 18, 2020, adding three open retail locations, an indoor cultivation facility, and a greenhouse cultivation facility.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.