A constructive view is maintained on energy despite concerns on demand destruction and related recession fears.

The first point to note is that, aside from China, there is very little evidence of demand destruction.

The International Energy Agency (IEA), which has a long history of underestimating demand, particularly in the developing world, again made various upward demand revisions in its monthly Oil Market Report (OMR) released last month.

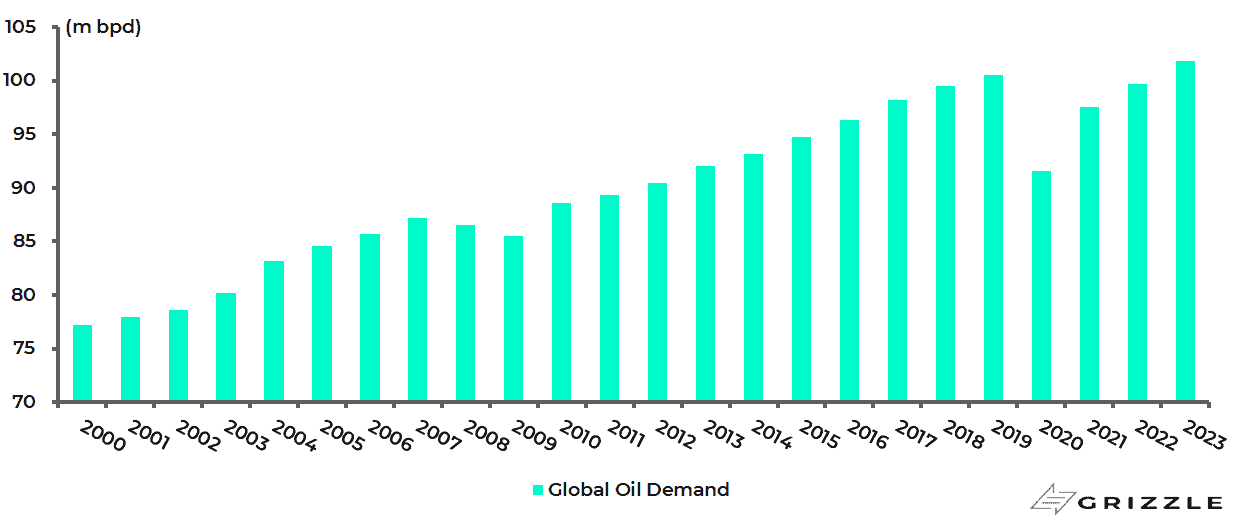

The IEA raised its estimate for 2022 global oil demand growth by 380,000 barrels/day to 2.1m b/d.

World oil demand is now forecast to rise to 99.7m b/d this year and by another 2.1m b/d to 101.8m b/d in 2023, surpassing the pre-pandemic peak of 100.6m b/d reached in 2019.

Global oil demand with IEA forecasts

In terms of concrete data, world oil demand for 2Q22 rose by 2% YoY to 98.5m b/d, though down from 100.8m b/d in 4Q21.

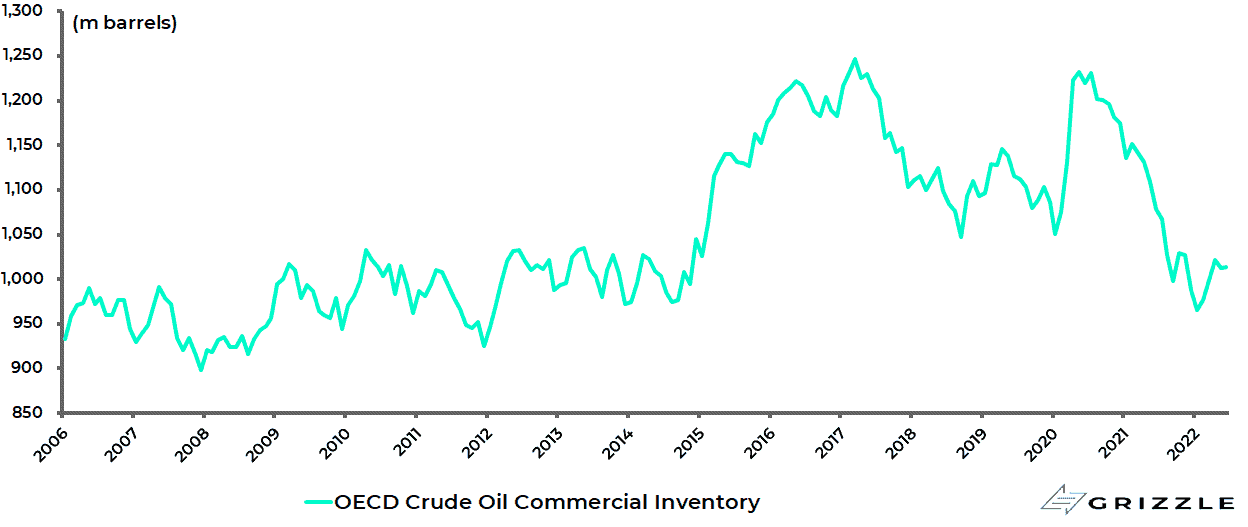

OECD crude oil inventories declined to 966m barrels in January, compared with the 2007 low of 898m barrels, and were still only 1.01bn barrels in June.

OECD crude oil commercial inventories

US Petroleum Reserve Releases End in October, What Then?

This is despite the fact that inventories have been boosted this year by the release of oil from the Strategic Petroleum Reserve (SPR) in America and from similar government oil reserves in other IEA member countries.

President Joe Biden announced at the end of March the release of 1m barrels of oil per day for six months through October, or over 180m barrels, from the US SPR.

While IEA member countries also announced in early April the collective release of 120m barrels over a period of six months from their emergency oil stock reserves, including 60m barrels from the US as part of Biden’s oil release plan.

This followed a similar agreement on 1 March by the IEA member countries to release 60m barrels of oil, including 30m barrels from the US.

This raises the obvious, though little discussed, issue of what is going to happen when the SPR releases come to an end as scheduled, at the end of October, just in time for the European winter.

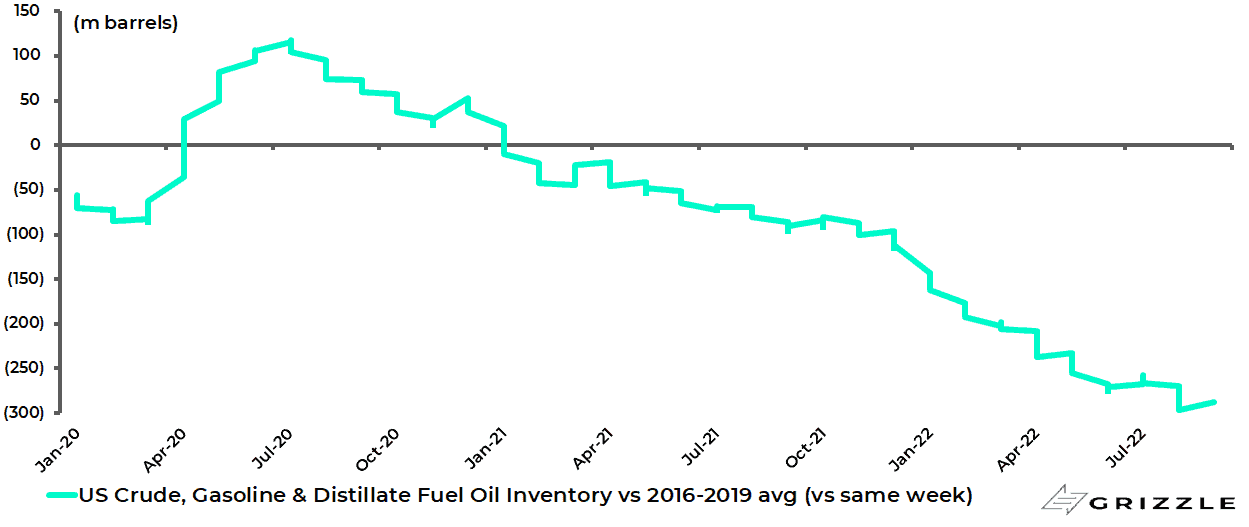

Meanwhile, the US so-called “Big 3” inventories (including SPR), which include crude oil, gasoline and distillate fuel, are now running at a new low relative to the pre-pandemic four-year average.

Thus, the US Big-3 petroleum inventories were 296m barrels below the 2016-2019 average in the week ended 26 August and were 288m barrels below the four-year average in the week ended 2 September, compared with 274m barrels in mid-June.

US Big-3 petroleum inventories

Source: US Energy Information Administration (EIA)

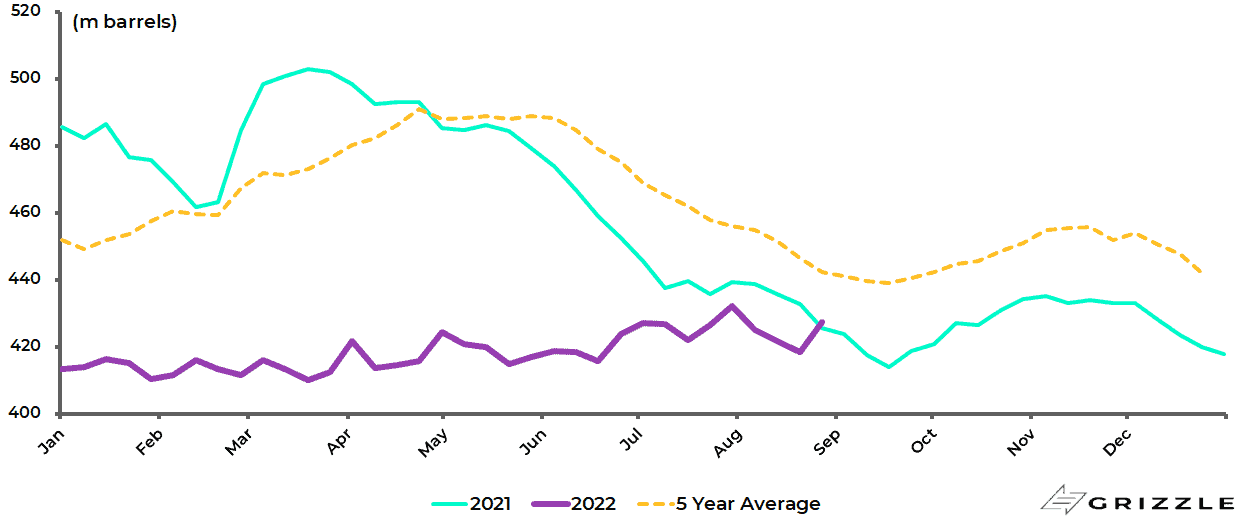

As for US commercial crude oil inventories (excl. SPR), they remain 3% below the average level of the past five years.

US commercial crude oil inventories (excl. SPR)

Source: US Energy Information Administration (EIA)

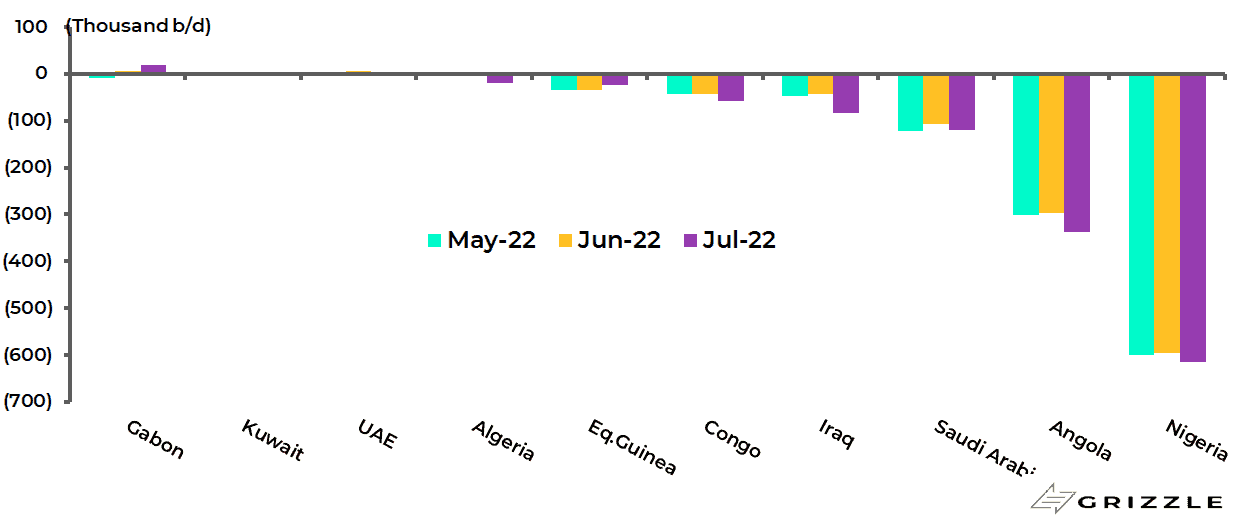

Another way of highlighting the underlying lack of supply is that OPEC data released last month shows that only three OPEC countries exceeded their production targets in July.

Actual oil production in Gabon, Kuwait and UAE exceeded their agreed production targets by 19,000 b/d, 4,000 b/d and 4,000 b/d respectively in July, while the other seven OPEC countries missed their targets by a combined 1.26m b/d

OPEC-10 countries crude oil production exceeded/missed their monthly targets in May-July 2022

As a result, the ten OPEC countries which agreed to raise production by 412,000 b/d in July missed their production targets by 1.2m b/d in July.

OPEC is Tapped Out: What Happens When China Demand Returns?

Meanwhile, it is worth noting that UAE energy minister Suhail Al-Mazrouei warned in June that it will be hard for OPEC to meet its production targets in 2023.

Al-Mazrouei was quoted as saying that oil prices were “nowhere near” their peak and that without more investment across the globe, OPEC cannot guarantee that supply will meet demand.

The OPEC+ group also noted in its post-meeting statement on 3 August that “the severely limited availability of excess capacity necessitates utilizing it with great caution”.

This suggests, as argued by the IEA last month, that substantial further OPEC+ output increases are unlikely in the coming months.

All this is why President Xi Jinping is doing the rest of the world a huge favour, in terms of the continuing Covid suppression policy, as China is the only country where there is real tangible evidence of demand destruction.

OECD Europe oil demand, for example, rose by 6.6% YoY to 13.52m b/d in 2Q22, according to the IEA.

By contrast, China oil demand declined by 6.5% YoY to 14.58m b/d in 2Q22.

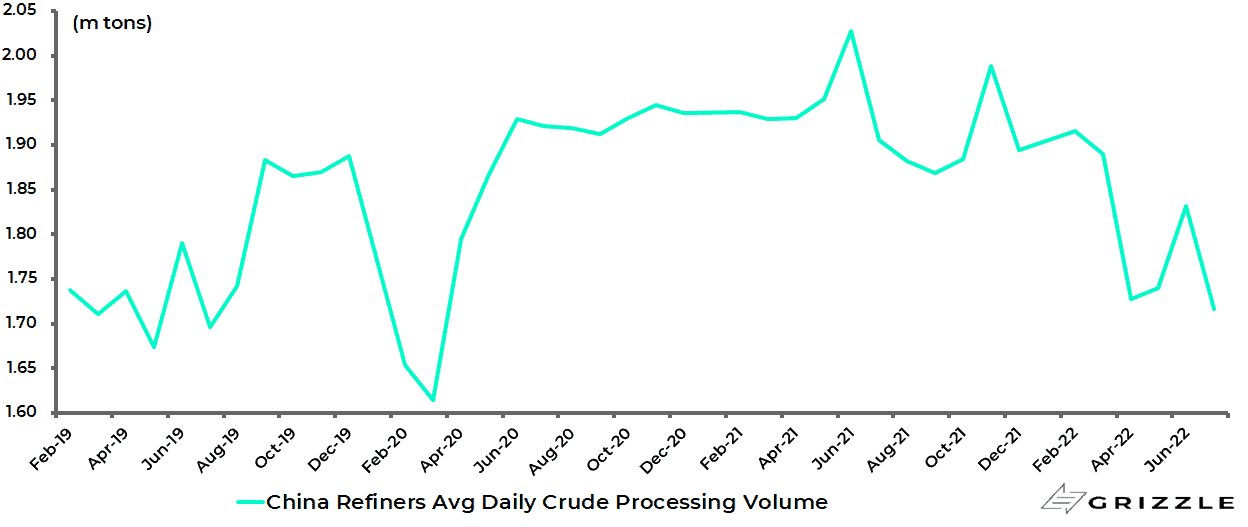

It is further the case that China refinery output fell by 8.8% YoY to 53.21m tons or 1.716m ton per day in July, the lowest level since March 2020.

China refiners’ average daily crude oil processing volume

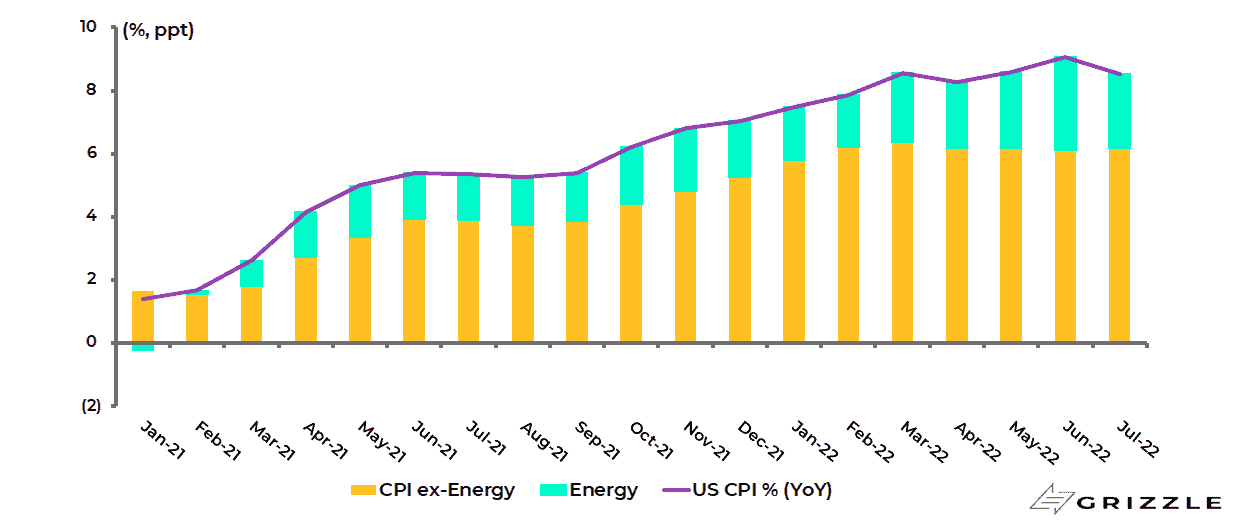

By keeping the spot price of oil down, China is helping the case for a near-term peaking out of inflation.

So far, the decline in inflation in the US since peaking in June is entirely down to the decline in the price of energy.

US headline CPI inflation slowed from 9.1% YoY in June to 8.5% YoY in July, while energy CPI inflation slowed from 41.6% YoY to 32.9% YoY, contributing 3.0ppts and 2.4ppts respectively to headline CPI.

Indeed CPI excluding energy has been flat at 6.6% YoY since April.

US CPI inflation contributed by energy and non-energy

Fundamentally, however, the macro environment remains stagflationary while investors also appear to be in danger of forgetting that wars are inflationary.

The renewed seemingly successful offensive by Ukraine, and the recent attacks on Crimea, are a reminder of the weaponry being provided by NATO to Ukraine and represent escalation in what arguably remains essentially a proxy war between America and Russia.

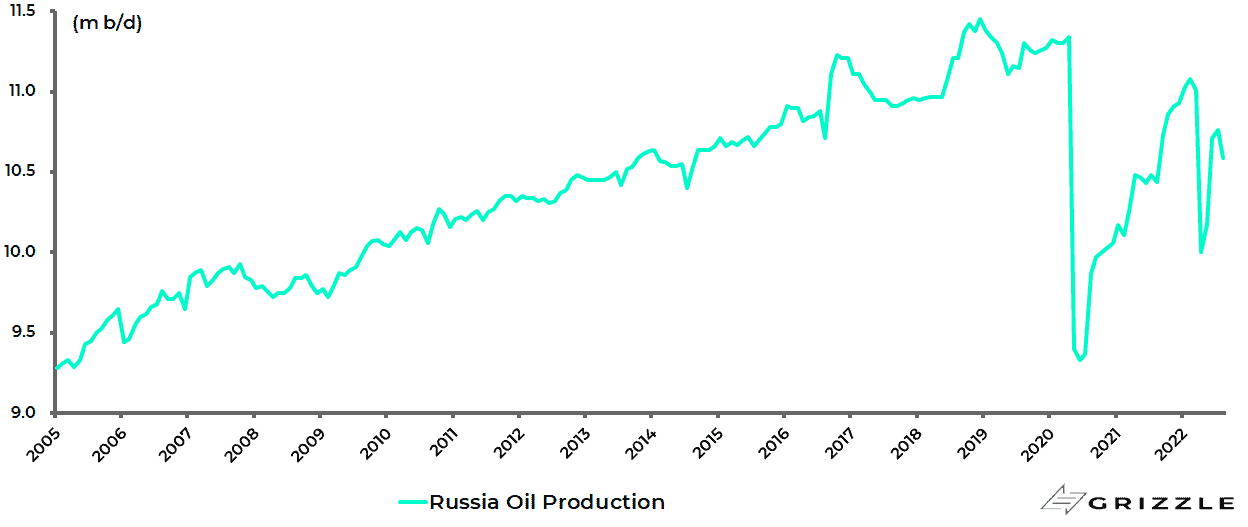

Meanwhile, the one area where oil production has rebounded strongly in recent months is Russia after the sharp decline triggered by the invasion of Kiev in March and the resulting imposition of sanctions.

Russian crude oil production has risen from a recent low of 10m b/d in April to 10.76m b/d in July and 10.59m b/d in August, compared with the recent high of 11.08m b/d in February.

Russia crude oil production

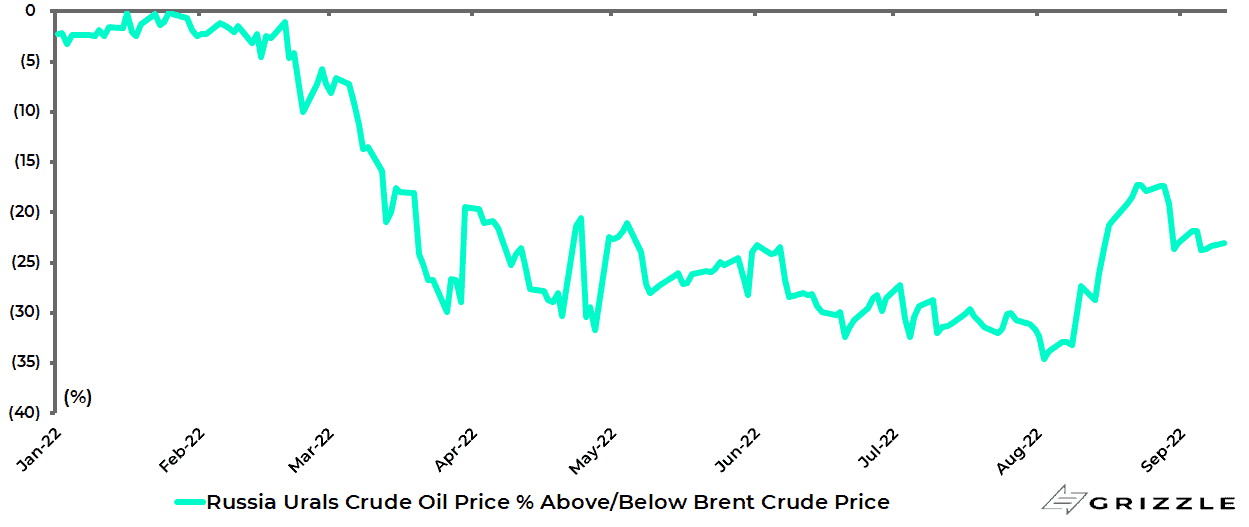

This shows that Russia has found new customers for the some 1m b/d that European oil refiners stopped purchasing due to self-sanctioning, though Russian oil is currently selling at a 23% discount to Brent.

Russia Urals crude oil price % above/below Brent crude oil price

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.