Bottom Line

After digging through the earnings of HEXO it’s clear this company is not in a good place.

Here at Grizzle we’ve been so focused on Aurora and Canopy, HEXO’s problems just kind of snuck up on us.

For simplicity we’ve made a list of the issues HEXO faces below.

- Second-lowest revenue per gram behind only VFF which sells almost exclusively wholesale.

- Production costs went up 8%, not down, in the quarter.

- Gross margin down to $1.00/gram, the lowest among the 12 largest producers.

- Only 4.5 months of cash left if they don’t use their debt facility or 6 months if they do.

- If HEXO grows production 400% a year it will still take 5 years to turn a profit.

I think you get the picture.

HEXO is in an unenviable position. The one brand it owns that is resonating with consumers, Original Stash, is sold at a $3/gram loss.

Even if they ramp sales to the full 50,000kg, they still would lose ~$0.50 on every gram sold.

The cost structure looks broken without significant margin improvement.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]HEXO has until April to turn things around or else investors are looking at more expensive debt, dilutive stock issuance and further stock market losses. [/su_panel]HEXO needs to grow annual sales from 17,000 kg to 90,000 kg, cut headcount by another 50% or hope the rollout of vape pens and edibles will double or triple gross margins.

Until investors see some hard decisions being made by management, we would not stick around to see how this horror movie plays out.

Quarterly Earnings in Charts

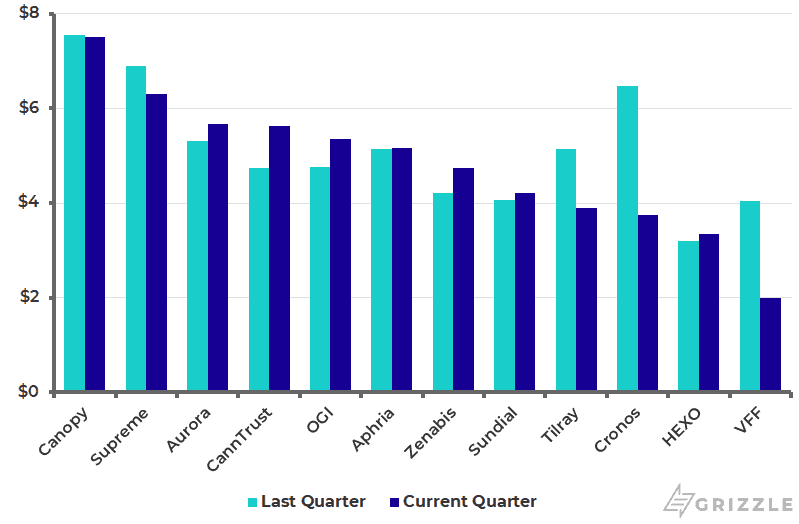

Revenue per gram is second-lowest among the 12 largest producers. HEXO saw pricing fall 8% this quarter which is a whopping 30% on a yearly basis.

Let’s hope the price slide reverses with cannabis 2.0.

Revenue per Gram

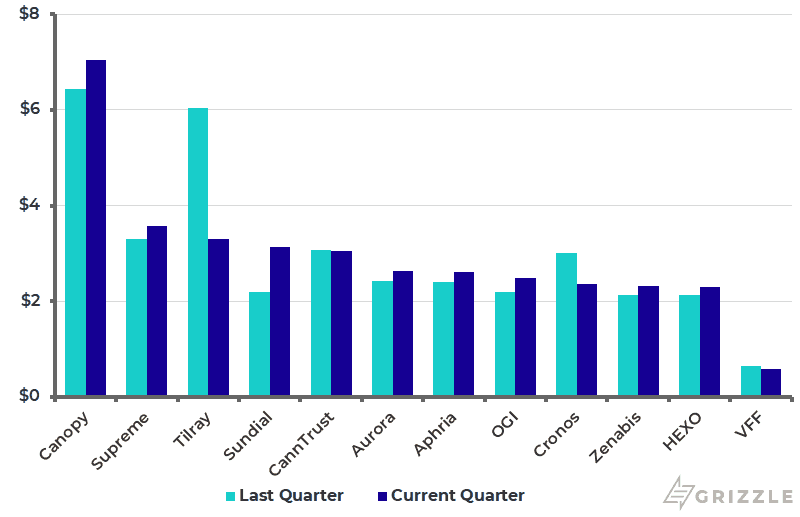

Production costs are only slightly below peers, but they have to be to turn a profit given how low revenue has fallen.

Production Costs Per Gram

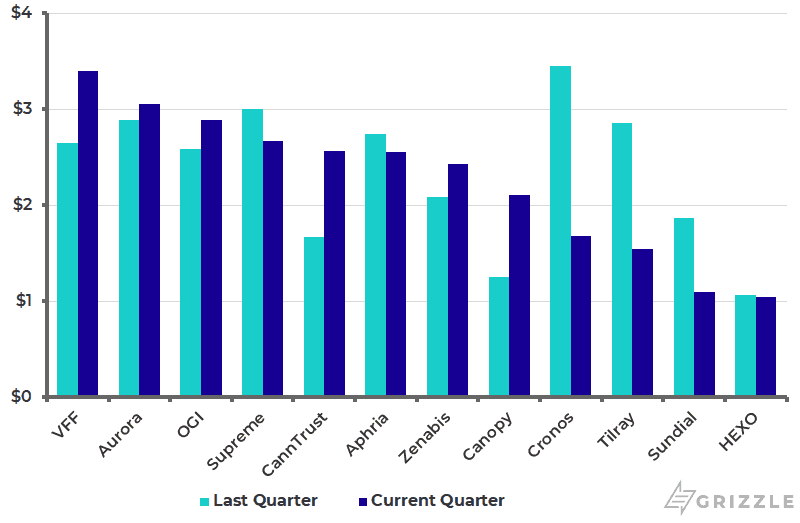

HEXO has growing costs only slightly below peers but significantly lower revenue.

As a result, gross margins are a full 33% below its worst peer, Tilray.

Gross margins determine how much money management has to pay corporate employees, rent, marketing, and all the other costs of running a corporate office.

HEXO is just barely breaking even on the business of growing cannabis and is deep in the red when corporate overhead costs are included.

Gross Margin per Gram

With only 4-6 months of cash left at the current burn rate HEXO has to make some tough decisions sooner than later.

Costs need to be cut significantly or else the company has to see an explosion in margins or volumes.

Years of Cash Left

A Full Review of HEXO Earnings

Canadian packaged cannabis goods company HEXO Corporation (TSE: HEXO) (NYSE: HEXO) announced its fiscal 2020 first quarter financial results today.

The maker of HEXO Cannabis and Up Cannabis products had revenue of $19.3 million compared to $6.6 million in the same period last year.

It reported a net loss of $62.4 million, almost 5-times the amount of the loss reported a year ago.

Loss from operations, however, improved quarter over quarter from $60.7 million to $58.5 million.

Operating expenses increased from the first quarter of fiscal 2019 from $22 million to $35 million, but improved quarter over quarter. The company recorded $3.7 million in one-time restructuring costs for the quarter, which included severance and other payroll expenses that were not part of the reported operating loss.

Grams Sold Only Marginally Higher

Grams sold increased 5% from the fourth quarter to 4,196 kg while revenue per gram decreased from $4.74 to $4.35 due to unfavourable price changes and provisions for sales returns.

The introduction of the premium line of Up cannabis products which brought in revenue of $7.03 per gram on dried flower in the first quarter helped boost results.

HEXO’s current annualized production is around 90,000 kg of dried cannabis, about half of which is dried flower. It is aiming to increase production to over 100,000 kg per year.

Operational Expenses Fall as Cost-Cutting Efforts Unfold

The company managed to significantly reduce costs in the recent period which investors like but the expenses still far exceed the gross margin.

Operational expenses of $35.1 million were 25% lower than last quarter driven by a 30% drop in G&A expenses and a 35% decrease in marketing expenditures.

CEO Sebastien St-Louis said, “We have done some pretty heavy lifting on our operations, as we work towards profitability in 2020. The choices that we have made and implemented have already led to a 25% reduction in our operating expenses. Cost control combined with our multi-brand approach, an updated strain mix, as well as the introduction of new products, will help us increase our market share and total revenue, leading us towards great results in 2020.”

HEXO is in the process of reducing its costs companywide to become a more efficient, profitable business.

The company is attempting a balancing act between cost control measures and expenses associated with international expansion efforts, including costs tied to its new facilities in Greece.

Convertible Debt Financing Bolsters Cash Balance

We estimate HEXO has cash and cash equivalents of $130 million which includes money left to borrow on a term loan and the recently closed C$70 million financing.

The remaining cash will be used to keep the lights on as well for expansion and improvements at its Gatineau and Belleville facilities, respectively.

HEXO has 4.5 months of cash left at the current burn rate of $87 million a quarter. If they max out the credit line it would buy them time until early May.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.