Bottom Line

Canadian cannabis stocks are separated into two buckets in investors’ minds.

On one hand, you have the players with multiple assets all over the globe, high-profile partnerships, or large-growing capacities.

On the other hand, you have producers with large but not massive growing capacity, a Canadian footprint, and lower profile partnerships or none at all.

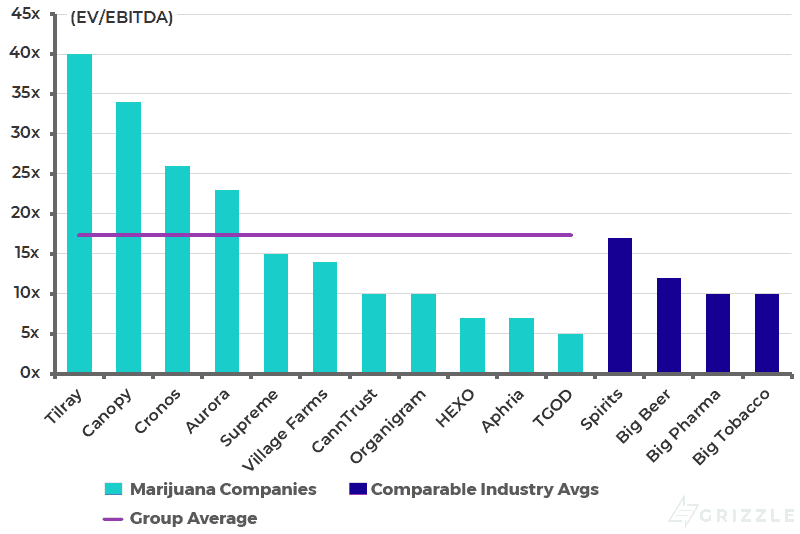

The first group is trading at nosebleed multiples because investors expect these companies to become the global titans of the industry.

The second group trades at what we would consider depressed multiples even though they are currently profitable or close to it, have lower growing costs than the big guys and are scaling much more smoothly.

HEXO (TSE: HEXO) falls into the second bucket with a low multiple, strong supply agreements in Quebec, and the second lowest production costs in the industry.

If expensive companies keep burning cash while the cheap companies turn a profit, we think there will be a wholesale re-rating of the sector.

This would benefit names like HEXO, Organigram, Supreme, Canntrust, and Aphria.

Cannabis demand is growing slowly in Canada increasing the risk that expensive companies let down their investors over the next year or so.

We think it is prudent for investors to own a basket of the low-priced names, especially after strong cannabis stock performance so far this year, and HEXO should most definitely be a member of that value portfolio.

Estimated 2020 Enterprise Value to EBITDA

What Happened in the Quarter

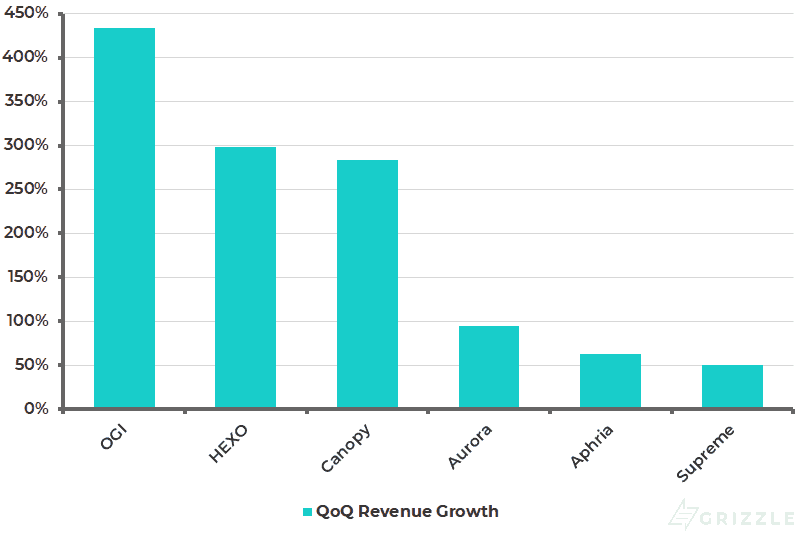

In the first full quarter of recreational sales, Hexo grew revenue 300% from last quarter to $13.4 million after excise taxes. This was the fastest quarterly growth in the industry behind only Organigram.

Revenue Growth in First Quarter of Legalization

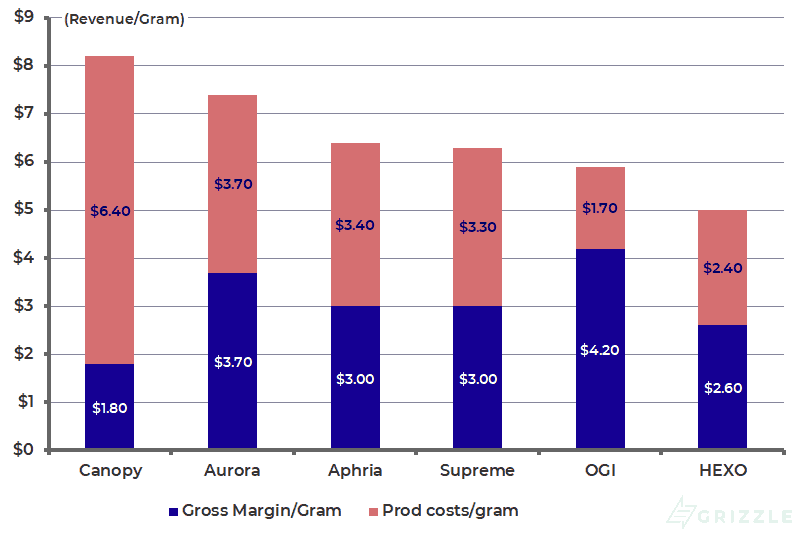

Net revenue per gram was stable at $5 per gram, while production costs fell 5% to $2.40 per gram.

HEXO generates the lowest revenue per gram in the group and even though the company has good cost control, the gross margin of $2.60 per gram is 15% below the large-cap average.

Each LP Ranked on Revenue and Gross Margin per Gram

General and administrative costs saw another big decrease this quarter down to $4.80 per gram from $15 per gram last quarter.

HEXO is still losing money, generating negative EBITDA, a measure of cashflow, of $6 million.

[su_panel background=”#150093″ color=”#ffffff” border=”0px solid #cccccc”]Based on the current gross margin, HEXO will need to sell 5,100 kg a quarter to break even, an increase of 90% from the 2,700 kg sold this quarter.[/su_panel]Unless consumer demand picks up or the company grows its market share, HEXO may not turn a profit until 2020.

Liquidity

HEXO has good liquidity especially when we include the $100 million of cash they are picking up through the acquisition of NewStrike Resources.

They also opened a $65 million bank borrowing facility in February and currently have no debt.

The pro-forma cash balance of $270 million gives them about a year of runway to reach profitability.

Based on their current sales trajectory and the coming legalization of edibles and infused beverages, we think it is likely the company begins generating a profit without needing to raise any more money from the market.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.