High Tide (CNSX:HITI; OTCQB:HITIF) reported their Q4 2019 earnings today.

Revenue came in at C$11.4 million which beat analysts’ estimates of C$11.01 million. This represents a YoY growth of 267.68% and a QoQ growth of 38%. EPS was -$0.13.

High Tide has been hammered in the stock market for the past year, much like the rest of the marijuana industry.

The problems that plague Hide Tide seem to follow the common theme of high cash burn coupled with decreasing margins and too much focus on growth at the expense of profitability.

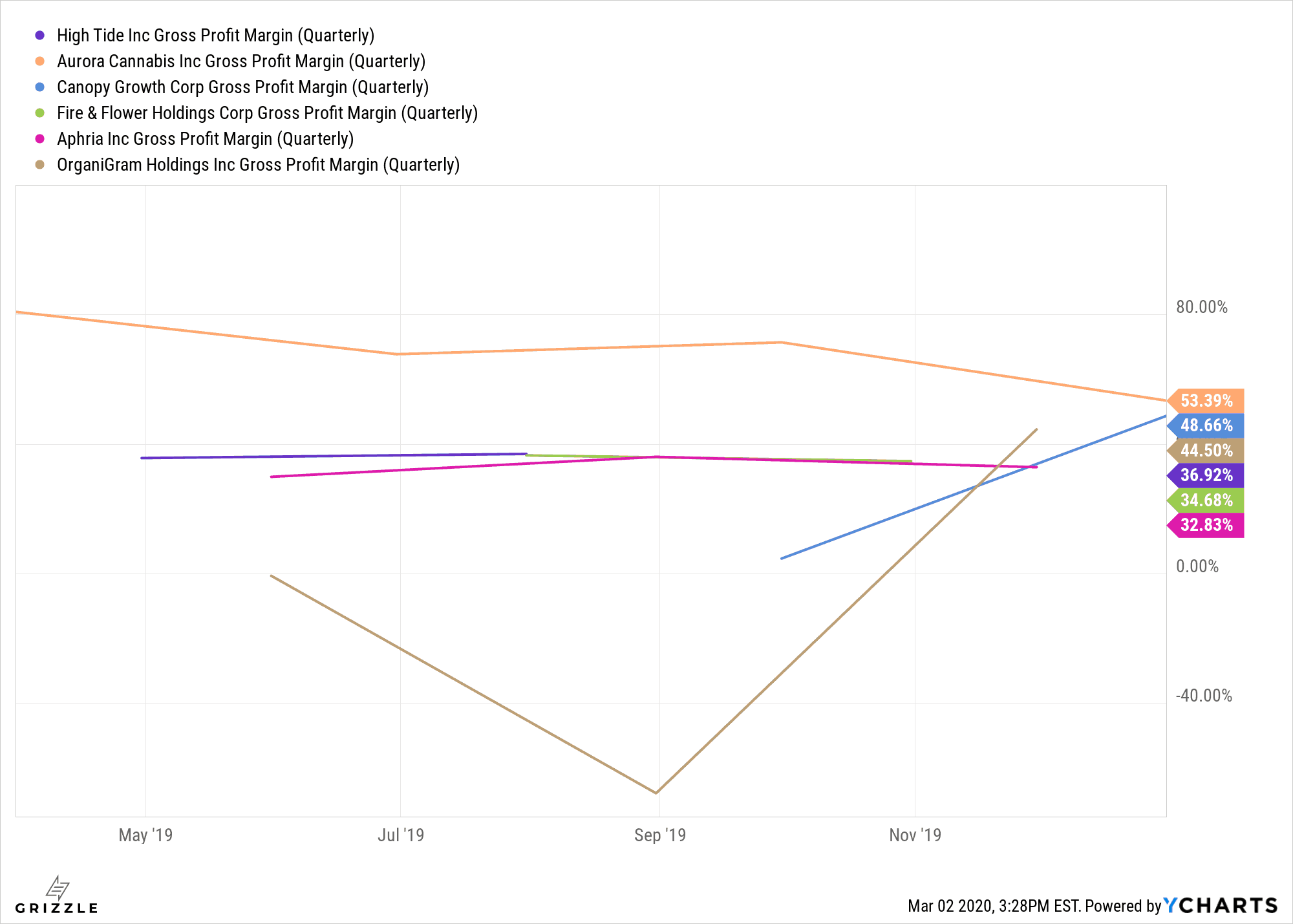

Margins for Retailers Are Generally Worse Than for Growers

We see that High Tide’s gross margin usually hovers at around the mid-30s percentage-wise.

This is compared to cannabis growers like Aurora Cannabis and Canopy Growth that have margins in the high 40s or low 50s percentage-wise.

Gross Profit Margins of Retailers vs. Growers

Without mergers and acquisitions, growers can theoretically get up to 70-80% gross margin, but for retailers it seems like gross margin will max out at around 30-40%.

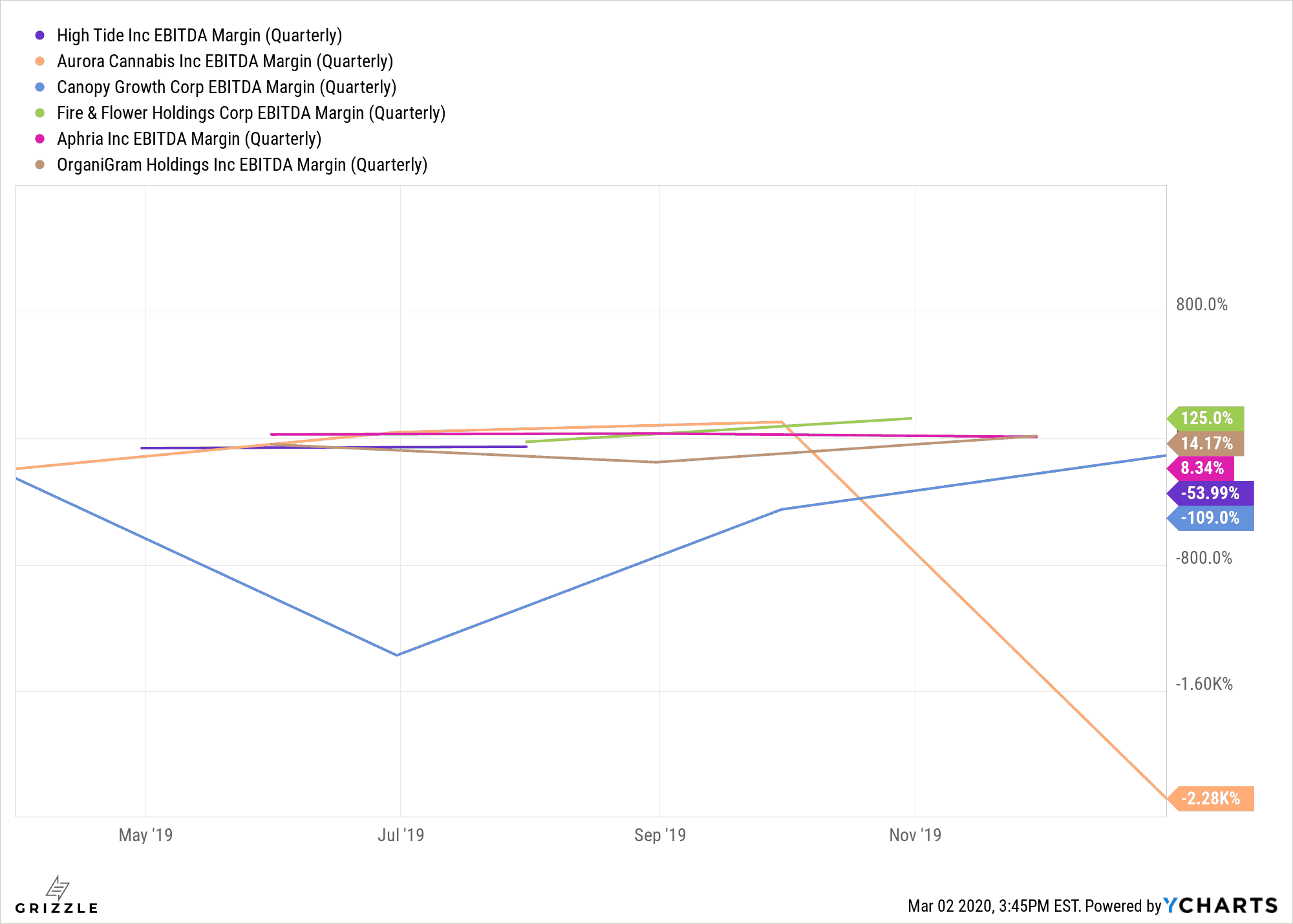

When it comes to EBITDA margins, it really varies wildly from company to company.

EBITDA Margins of Retailers vs. Growers

Some of the big cannabis growers like Aurora Cannabis and Canopy Growth have margins that are deeply in the red as they spend on growth and High Tide looks no different with less than negative 50% EBITDA margin.

High Tide, like many other retailers, remains far from profitable.

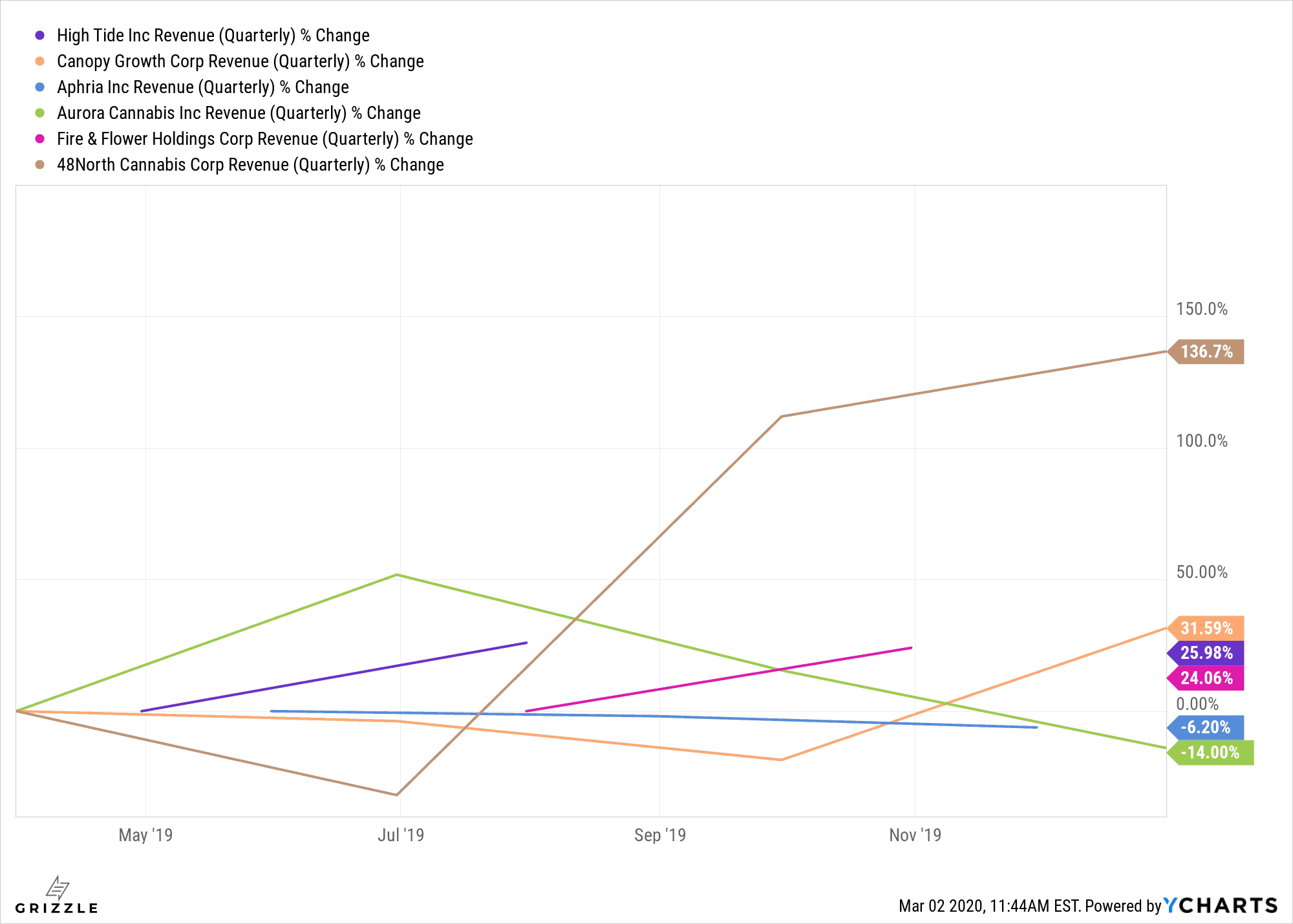

So What If You Are Willing to Give Up Profit for Growth?

Looking at a one-year chart for revenue growth, we see that there has been a decent increase in revenue for High Tide and that it is approximately in-line with Fire & Flower, another big cannabis retailer.

However, 26% revenue growth might still not be enough for a company burning cash this fast.

Revenue Growth of Retailers vs. Growers

Taking a look at the cash balance, as of last quarter the company only has US$600,000 of cash on hand.

This compares to a cash burn rate of $4.55 million per quarter when spending on operations and new locations are combined.

However, the silver-lining is that High Tide is not in any immediate danger of running out of cash seeing as they have issued approximately $11.5 million of debt and has a further $10 million as a term credit with Windsor Private Capital out of which $6 million the company has immediate access to.

All of these new debts allow High Tide about another 10 months of cash before they would run out at their current burn rate.

Still, this is not good news for investors since the debt that High Tide has issued are at some pretty steep interest rates (for example, the $10 million term credit with Windsor Private Capital is at an interest rate of 11.5% per annum).

We should continue to expect the company to issue more debt or dilute shareholders further by issuing more shares.

Betting long on High Tide stock just doesn’t seem like it’s worth the risk right now given the company’s cash issues.

Investors watching High Tide should sit and wait until the company either builds a much higher cash position or gets far closer to break even.

The company is far away from achieving either of these.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.