There is no doubt that investors’ focus of late has been on the stagflation story.

Still, it should be emphasized that this writer is talking more about a stagflation scare, with the potential to trigger a risk-off move in Wall Street-correlated world stock markets, rather than necessarily predicting a stagflationary outcome.

The trigger for such a correction would be a further surge in energy prices if there is not some sudden evidence of near-term relief provided on two possible fronts.

- The first, as regards natural gas prices, is whether the Eurozone can agree to a deal with Russia on the Nord Stream 2 pipeline.

- The second is whether OPEC+ will cut the world some slack by deciding to pump more oil.

But this did not happen at its meeting on 4 November.

Rather OPEC agreed to stick to its existing schedule.

The OPEC+, which includes OPEC, Russia and their allies, decided to reaffirm the production plan agreed in July and raise output by only 400,000 barrels per day in December.

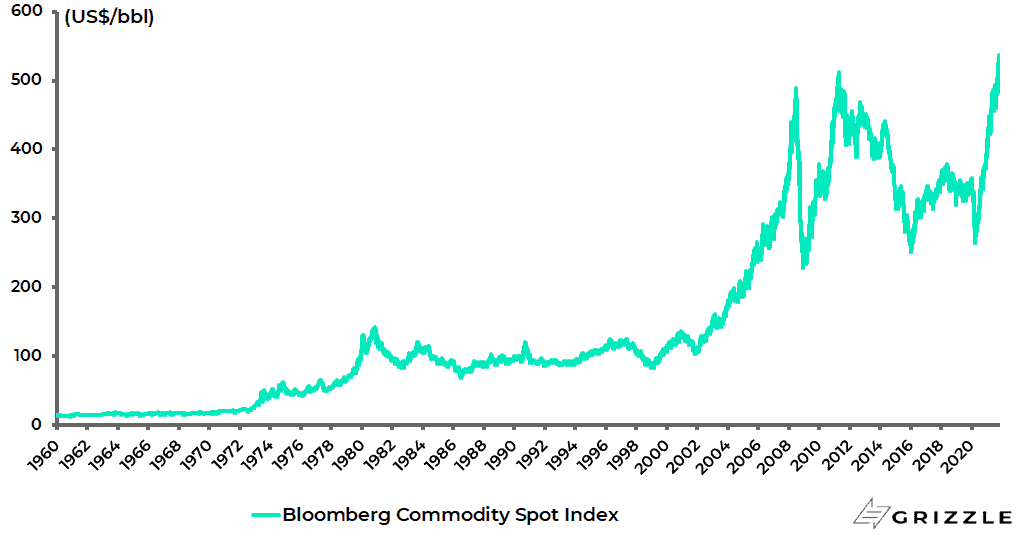

Meanwhile, it is worth noting that the Bloomberg Commodity Spot Index, which comprises 23 commodity prices, has risen by 36% from the start of this year to a record high on 25 October, though it has since declined by 3%.

Bloomberg Commodity Spot Index

Stagflation Needs Weak Consumer Demand – Consumers are Still Flush with Cash

If these are the near-term issues, the case for a stagflationary outcome, as opposed to a further stagflation scare, is, for now at least, not overwhelming.

This is because of the increased savings of American households as a result of the surge in transfer payments during the pandemic, most of which has not been spent.

This means they have a certain buffer against the impact of rising prices.

Americans have received US$2.2tn more in transfer payments since March 2020 compared with pre-Covid levels, with personal savings increasing by US$2.3tn over the same period.

US Personal Income and Savings

| US$bn, saar | Feb-20 (Pre-Covid) |

Sep-21 | Mar20-Sep21 (Average) |

Mar20-Sep21 Chg vs Feb-20 |

| Personal income (excl. transfers) | 17,287 | 18,177 | 17,248 | (61) |

| Personal current transfer receipts | 3,208 | 3,913 | 4,617 | 2,231 |

| Disposable personal income | 16,735 | 17,882 | 18,025 | 2,042 |

| Personal outlays | 15,342 | 16,546 | 15,162 | (285) |

| Personal saving | 1,392 | 1,336 | 2,862 | 2,327 |

| Personal saving/disposable income (%) | 8.3 | 7.5 | 15.9 | 7.6 |

Note: Personal income includes compensation of employees, proprietors’ income, rental income, interest and dividend incomes. Source: Bureau of Economic Analysis, Jefferies

While the New York Fed consumer surveys suggest that Americans have spent so far only 25-29% of their three rounds of stimulus cheques received during the pandemic.

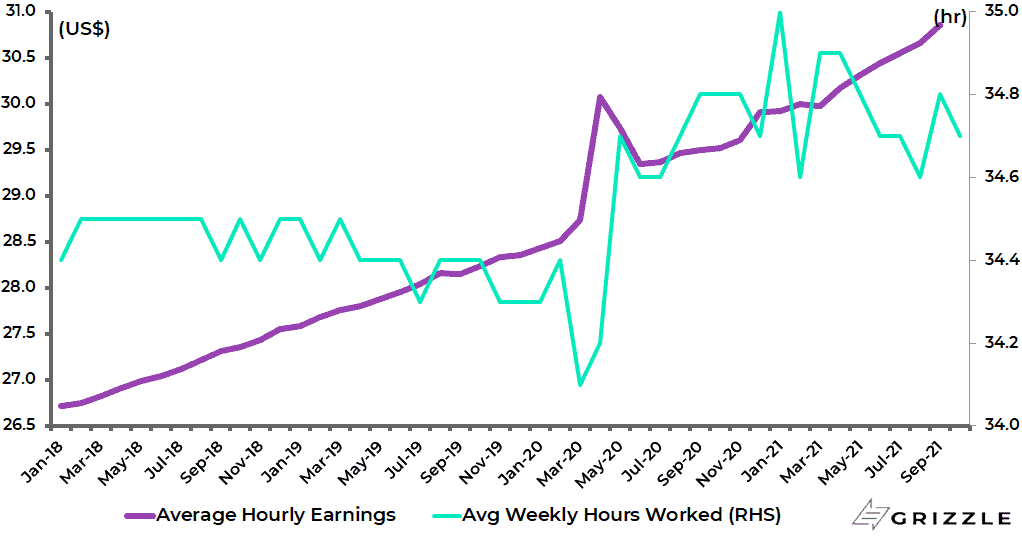

Higher wages and a longer workweek have also helped to more than offset the 4.2m jobs which have gone missing since the pandemic.

Wages have risen by 8.9% since the start of the pandemic and the workweek has lengthened by 1.2%.

US average hourly earnings and average workweek of private employees

Wage Gains Could end up Being a Big Driver of Inflation

Still, this increase in wages is one of the potential drivers of inflation going forward, most particularly if American households become more confident the pandemic is over.

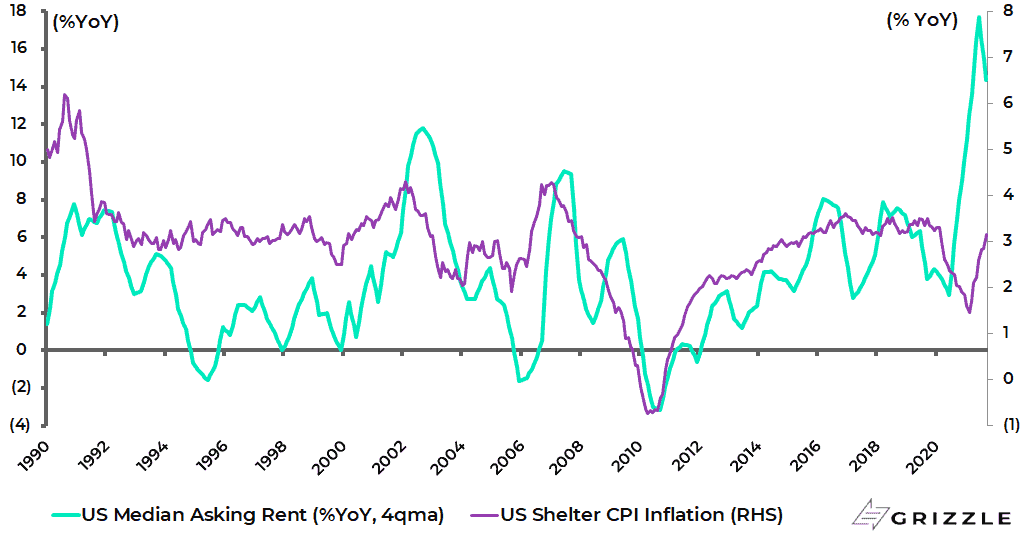

If rising wages can be one driver of inflation going forward once the Covid lockdown-triggered supply chain disruptions have peaked, in terms of congested roads/ports and the like, and they presumably have to peak at some point, the other driver of inflation in America will be rents, given the 41% weighting of the shelter component in America’s core CPI.

The latest data shows rents continue to rise and, as a consequence, there is significant potential for shelter to play catch up in coming months.

Shelter CPI inflation rose from 2.8% YoY in August to 3.2% YoY in September, the highest level since February 2020.

Meanwhile, the Census Bureau’s median asking rent rose by 17.7% YoY in the four quarters to 2Q21 and was up 14.3% YoY in the four quarters to 3Q21, sharply up from the 3% YoY increase recorded in the four quarters to 2Q20.

US shelter CPI inflation and median asking rents

Will NordStream 2 be Approved in Time for Winter?

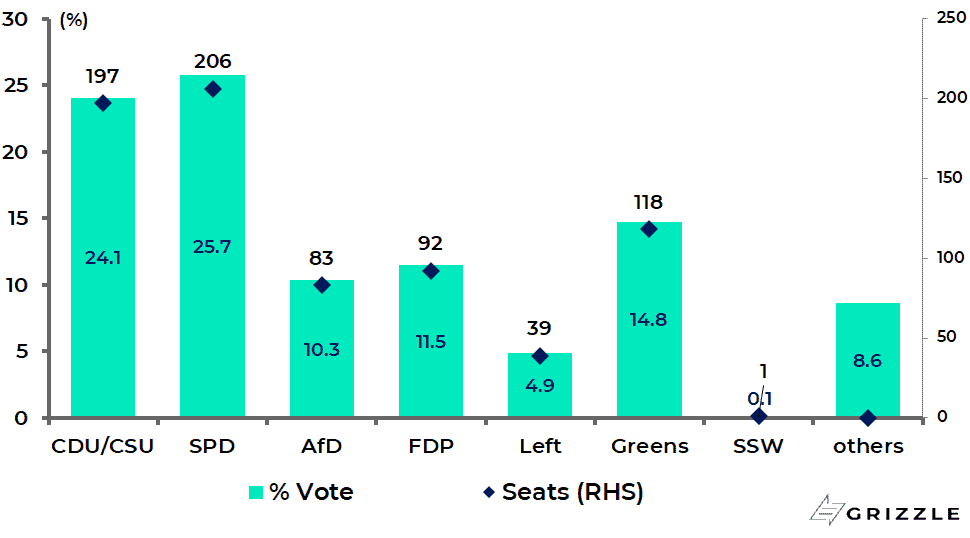

Meanwhile returning to Europe and the topical subject of gas, one issue is whether the Nord Stream 2 pipeline issue, with a capacity of 55bn cubic metres of gas per year, can be resolved on the watch of Germany’s veteran leader Angela Merkel who is due to step down as Chancellor before the end of this year following the completion of coalition discussions for a new government.

Technically, the pipeline was completed in terms of construction on 10 September last year and Gazprom, in a form of kabuki, began on 4 October filling the pipeline with gas. The Russian gas giant finalized its application with the Bundesnetzagentur (BNetzA), the German regulator responsible for electricity and natural gas, on 8 September.

From that date the regulator has four months to issue a certification or deny it.

The technical complication is that, as a result of pressures from the likes of Ukraine, Brussels amended in 2019, during the construction of the pipeline, its so-called “Gas Directive”.

This means that the decision made by BNetzA also needs to be approved by Brussels, which can also take up to four months.

The above raises the issue of whether Merkel will use her final months in power to try and push her favoured project through.

Germans dependent on gas heating this winter will certainly hope so.

It should be remembered that Merkel resisted huge American pressure during the Trump administration in terms of her continuing support for Nord Stream 2.

The situation would be straightforward for the veteran German leader if it was just a domestic German issue.

But Brussels’ involvement certainly complicates matters.

The other point to note is that, by the end of this year, three more German nuclear plants will be closed down.

By the end of next year the last remaining three plants will also be closed down.

The Greens’ presence in the next federal government means that these deadlines will likely be enforced.

The current six plants still contribute about 12% of German electricity.

At its peak, Germany had 19 nuclear plants in 2000 generating about 30% of the country’s electricity.

And there were still 17 nuclear plants operating before Merkel took her precipitous decision to exit nuclear post Fukushima in May 2011.

Meanwhile part of the initial agreement of the new coalition government is that 2% of the German land area should be devoted to windmills.

Germany Federal Election Results 2021

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.