As the media focuses on the closely contested US presidential race, as well as, of course, the Covid “second wave”, investors should also be thinking about the impact of a return to normal in terms of economic activity.

This is because it is still assumed here that the virus will either have burnt itself out by the middle of next year or, by then, a vaccine should be widely available.

On the latter point, the bottleneck seems to be less coming up with a vaccine itself but rather ramping up production on the scale required.

Still, one way or another a return to normal is coming sooner or later, as has already happened in the Chinese economy.

At that point, the key question will become how the G7 central banks, led by the Fed, will react.

A Cyclical Recovery Usually Leads to Higher Rates but This Time is Different

For in the circumstances where markets are clearly signaling cyclical recovery, be it in terms of yield curve steepening or rising inflation expectations, why should the Fed at that point impose yield curve control in line with this writer’s base case as argued here previously?

This is indeed a legitimate question.

For in such circumstances the Fed should be thinking of tightening, thereby giving Fed chairman Jerome Powell another chance to engage in another pivot.

And certainly, if Powell does decide to pull back on easing in such circumstances it is likely to trigger a car crash in stock markets, which is likely to make the so-called “taper tantrum” of 2013 look like a picnic.

But that is not the base case here precisely because the Fed, as of its FOMC meeting in mid-September, has now given itself licence to overshoot its inflation target via the formal softening of that target.

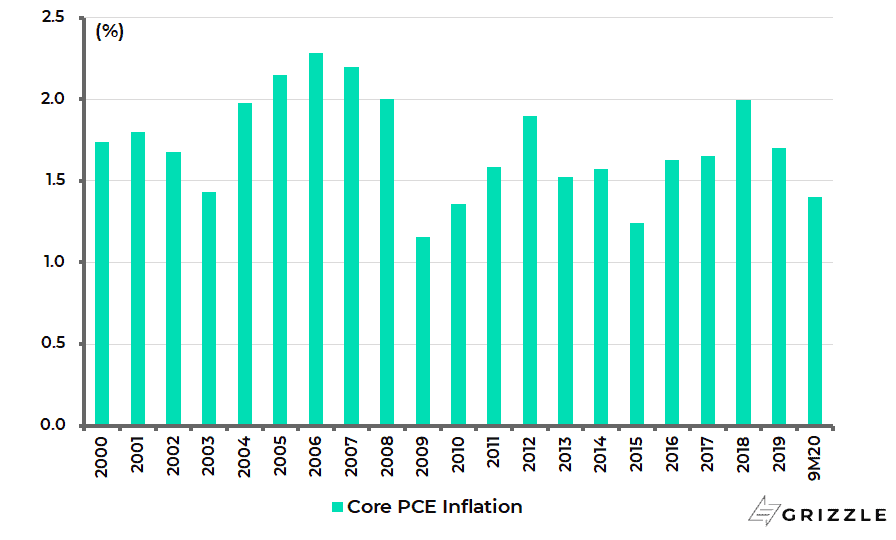

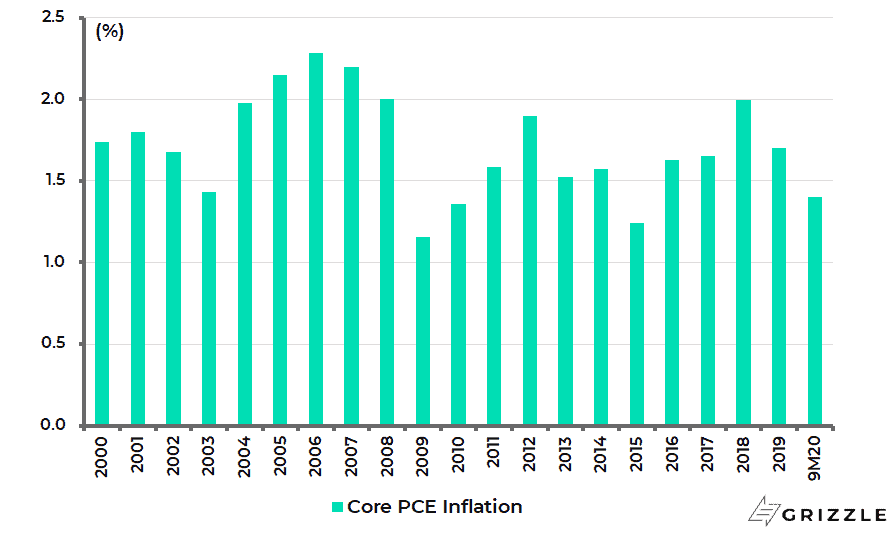

This is because the Fed has undershot the 2% inflation target on its favored inflation indicator, core PCE inflation, for 11 of the past 12 years.

US Annual Core PCE Inflation

The Government Can’t Afford Not to Implement Yield Curve Control

If this will be the rationale for remaining doveish in the face of evidence of cyclical recovery, a similar rationale will also be articulated if the Fed decides, in line with the base case, to lock in bond yields in some version of the Bank of Japan’s yield curve control in response to rising yields at the long end of the Treasury curve.

Still, if the stated rationale for such a move will be not to threaten the 2% inflation target by pre-emptive tightening, this writer, as well as many other market participants, will also conclude that the Fed’s desire to lock in bond yields will be driven by another more basic motive.

That is that the central bankers understand that the system cannot afford higher interest rates, which makes formal policies of financial repression a growing necessity in the G7 world.

Obviously, this point will not be admitted to by the likes of Powell, the “reverse Volcker”, in his official statements.

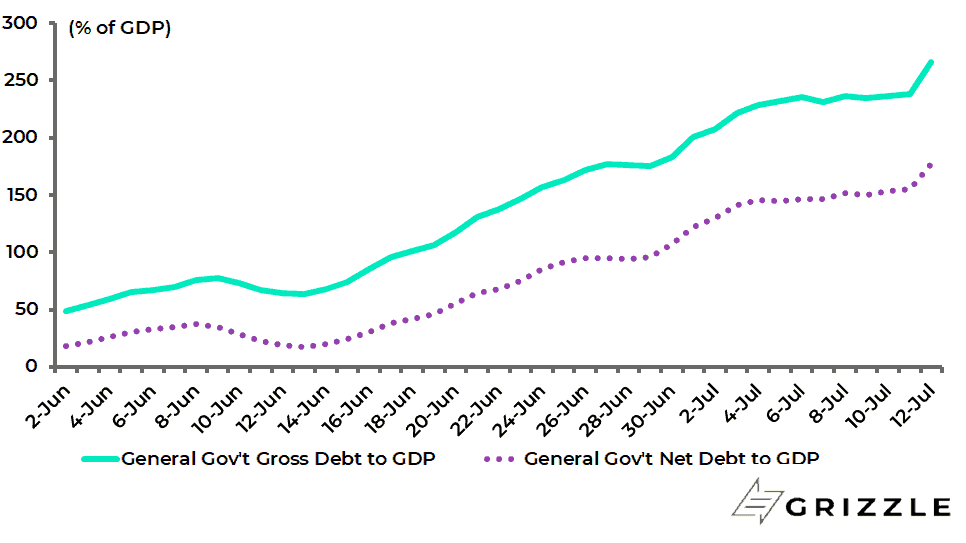

In this respect, it has long been understood that Japan has reached a level of indebtedness in its government sector which has made higher interest rates not an option; though the passive nature of Japanese investors has allowed seemingly unimaginable excesses to have been reached in terms of government debt to GDP even if, to be fair, the numbers look more manageable on a net rather than gross basis.

Japan’s gross general government debt to GDP rose to 238% of GDP at the end of 2019 and is projected by the IMF to reach 266% by the end of this year, while general government net debt to GDP was 155% of GDP last year and is projected to reach 177% this year.

Japan Gross and Net General Government Debt as % of GDP

Indeed, the debt servicing ratio of the Japanese government has actually fallen in recent years courtesy of ultra-low interest rates.

Japan’s national debt service, as a percentage of government tax revenues, has declined from 47.8% in FY12 ended 31 March 2013 to 37.4% in FY19 and a budgeted 37.8% this fiscal year.

Japan National Debt Services as % of Government Tax Revenues

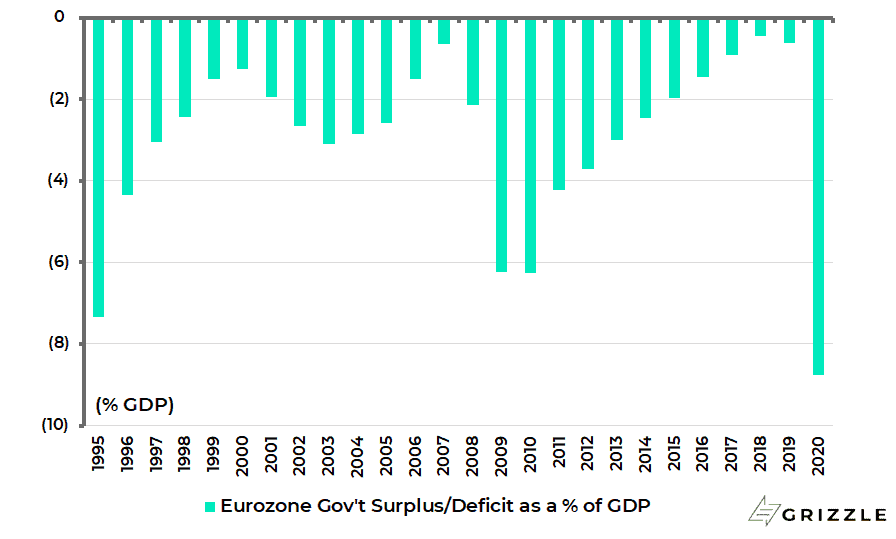

Eurozone government bond investors have also similarly remained remarkably passive in the context of the now six-year experiment in negative rates.

Meanwhile, Eurozone governments now forecast the Eurozone fiscal deficit to reach 9% of GDP this year as a consequence of stimulus efforts triggered by the pandemic, up tenfold from the 2019 level.

Eurozone Government Surplus/Deficit as % of GDP

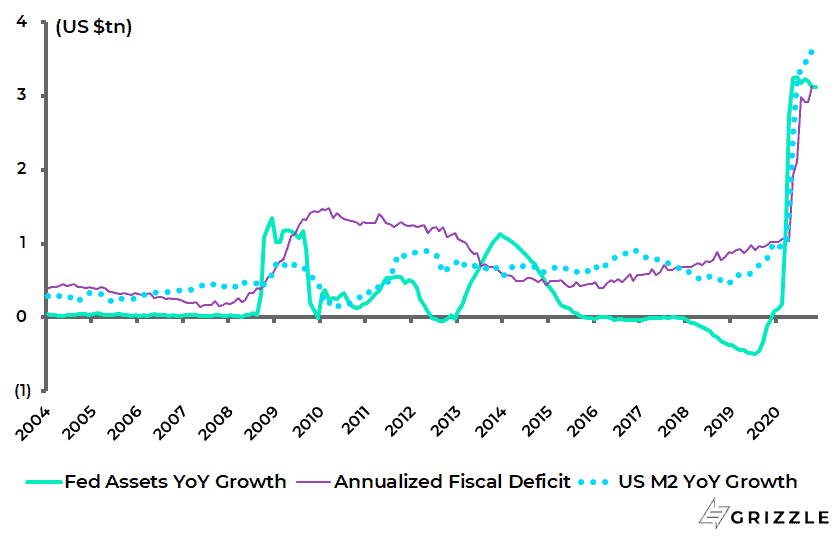

As for America, the annualised fiscal deficit was running at US$3.1tn or 15.2% of GDP in the fiscal year ended 30 September, while the convergence of monetary policy with fiscal policy is highlighted dramatically by the chart below showing the trend in the Fed balance sheet expansion, the annualised US fiscal deficit and US M2 growth.

US Annualised Fiscal Deficit and YoY Change in US M2 and Fed Assets

But if the Fed is planning to do this it probably needs to move relatively early in the yield curve steepening cycle triggered by any anticipated cyclical recovery.

For such reasons, the key issue for financial markets in the next several months is not who wins the presidential election, nor the state of US-China relations, but how the Fed reacts to the cyclical return to normal.

As for the other G7 central banks, they will most likely follow the path set by the Fed.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.