Bottom Line

iAnthus is the poster child for a company in transition.

Management has proven themselves to be financially agile and willing to move quickly to stay neck and neck in the race to own the U.S. medical market in anticipation of nationwide legalization.

There are so many moving parts operationally for this company that it would be foolish for investors to draw any conclusions from the final two quarters of 2018.

Based on retail locations alone, iAnthus will be triple its current size by the end of next year.

The U.S. market may be changing too rapidly for investors to clearly pick a winner today, but by hitching yourself to a U.S. management team that is aligned with investors you increase the chances of a positive outcome.

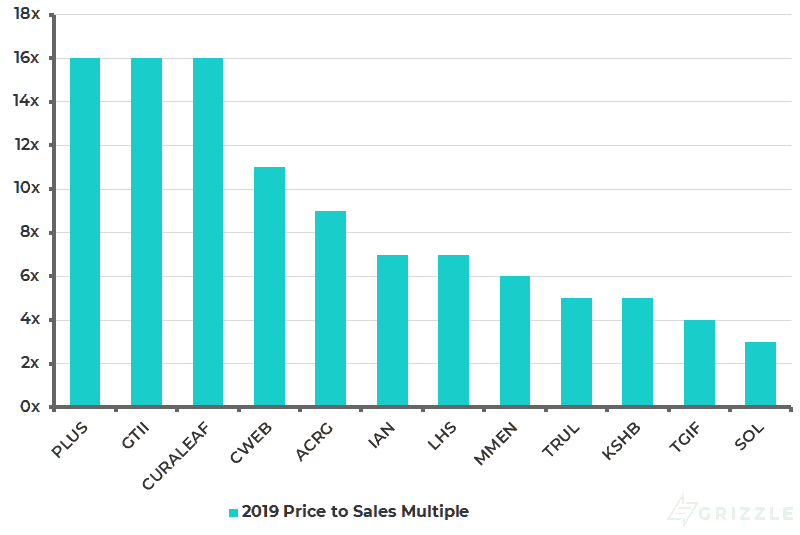

iAnthus is currently being overshadowed by new multi-state operator listings in Canada, but all this is doing is providing an attractive entry point for investors (30% discount to peers) with a multi-year time horizon.

Own iAnthus today for the best management team and shareholder voting structure in U.S. Cannabis, not for financial results over the next 3-6 months.

Operational Review

Revenue increased 267% over last quarter due to a new store opening in Boston and an increased patient count in Florida.

Total non-cash assets increased by 5% to $122 million, driven by an 11% increase in the value of property plant and equipment to $23 million.

iAnthus should see significant asset and revenue growth in the quarter ending December as two stores in Florida and one in Brooklyn, New York will open.

The purchase of MPX is still on track for a shareholder vote in early January and should close by February or March at the latest.

2019 Price to Sales by U.S. License Holder

Conclusion

iAnthus was one of the first U.S. operators to list on a Canadian exchange and is now being overshadowed by new multi-state operators who are making headlines for their famous board members and large reverse mergers in Canada.

Even though iAnthus may not be top of mind for investors, management is still working hard under the radar to build a business that can effectively compete with any other larger operator in America.

Retail investor disinterest has only made iAnthus a more compelling value.

iAnthus trades for $30 per retail store license while competitors MedMen, Green Thumb, Acreage and Curaleaf trade for 50% more at $45 per retail license.

With a strong management team and compelling valuation, iAnthus is one of Grizzle’s preferred ways to invest in the U.S. cannabis market.

In the interest of full disclosure, employees of Grizzle personally purchased and currently own stock in iAnthus. See the Content Disclosure section here on our Terms and Conditions page for more details.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.