The Time “person” of the year award is often something easy to make fun of in the way that magazine covers are usually, but not always, useful contrarian indicators.

Witness the award in 2020 to Joe Biden and Kamala Harris or that matter the 2009 award to Ben Bernanke, though it has to be admitted that Bernanke’s activities were very helpful for the US stock market and, of course, Wall Street.

In that narrow sense the latter award was well-timed.

The 2021 award to Elon Musk may well prove similarly well-timed, and in this writer’s view far more deserved than most of the other recipients this century, though whether the iconoclastic Tesla founder will particularly welcome it is another matter given his refreshing shunning of traditional media outlets.

Musk, like the now silenced 45th American president, has used Twitter as a remarkably effective tool for getting out the message to his 68m followers directly, thereby disintermediating conventional media and the whole of the public relations industry along with it.

Time Person of the Year

| 1927 | Charles Lindbergh | 1959 | Dwight D. Eisenhower | 1991 | Ted Turner |

| 1928 | Walter Chrysler | 1960 | U.S. Scientists | 1992 | Bill Clinton |

| 1929 | Owen D. Young | 1961 | John F. Kennedy | 1993 | The Peacemakers |

| 1930 | Mahatma Gandhi | 1962 | John XXIII | 1994 | John Paul II |

| 1931 | Pierre Laval | 1963 | Martin Luther King Jr. | 1995 | Newt Gingrich |

| 1932 | Franklin D. Roosevelt | 1964 | Lyndon B. Johnson | 1996 | David Ho |

| 1933 | Hugh S. Johnson | 1965 | William Westmoreland | 1997 | Andrew Grove |

| 1934 | Franklin D. Roosevelt | 1966 | The Inheritor | 1998 | Bill Clinton & Ken Starr |

| 1935 | Haile Selassie | 1967 | Lyndon B. Johnson | 1999 | Jeff Bezos |

| 1936 | Wallis Simpson | 1968 | The Apollo 8 astronauts | 2000 | George W. Bush |

| 1937 | Chiang Kai-shek & Soong Mei-ling | 1969 | The Middle Americans | 2001 | Rudy Giuliani |

| 1938 | Adolf Hitler | 1970 | Willy Brandt | 2002 | The Whistleblowers |

| 1939 | Joseph Stalin | 1971 | Richard Nixon | 2003 | The American soldier |

| 1940 | Winston Churchill | 1972 | Richard Nixon & Henry Kissinger | 2004 | George W. Bush |

| 1941 | Franklin D. Roosevelt | 1973 | John Sirica | 2005 | The Good Samaritans |

| 1942 | Joseph Stalin | 1974 | Faisal | 2006 | You |

| 1943 | George C. Marshall | 1975 | American women | 2007 | Vladimir Putin |

| 1944 | Dwight D. Eisenhower | 1976 | Jimmy Carter | 2008 | Barack Obama |

| 1945 | Harry S. Truman | 1977 | Anwar Sadat | 2009 | Ben Bernanke |

| 1946 | James F. Byrnes | 1978 | Deng Xiaoping | 2010 | Mark Zuckerberg |

| 1947 | George C. Marshall | 1979 | Ruhollah Khomeini | 2011 | The Protester |

| 1948 | Harry S. Truman | 1980 | Ronald Reagan | 2012 | Barack Obama |

| 1949 | Winston Churchill | 1981 | Lech Wałęsa | 2013 | Francis |

| 1950 | The American fighting-man | 1982 | The Computer | 2014 | Ebola fighters |

| 1951 | Mohammad Mossadegh | 1983 | Ronald Reagan & Yuri Andropov | 2015 | Angela Merkel |

| 1952 | Elizabeth II | 1984 | Peter Ueberroth | 2016 | Donald Trump |

| 1953 | Konrad Adenauer | 1985 | Deng Xiaoping | 2017 | The Silence Breakers |

| 1954 | John Foster Dulles | 1986 | Corazon Aquino | 2018 | The Guardians |

| 1955 | Harlow Curtice | 1987 | Mikhail Gorbachev | 2019 | Greta Thunberg |

| 1956 | The Hungarian freedom fighter | 1988 | The Endangered Earth | 2020 | Joe Biden & Kamala Harris |

| 1957 | Nikita Khrushchev | 1989 | Mikhail Gorbachev | 2021 | Elon Musk |

| 1958 | Charles de Gaulle | 1990 | George H. W. Bush |

Source: Time Magazine, Wikipedia

The reason why the award should be well-timed is that 2022 is the year that it should become much clearer how much legacy carmakers can compete, or not compete, with the Tesla phenomenon.

There are apparently more than 400 new EV models due to be launched in the coming years as legacy carmakers, motivated by a combination of government-induced sticks and carrots as well as the Tesla phenomenon itself, struggle to meet the challenge of disruption.

Whatever the exact number of new models, as someone who used to cover the auto sector journalistically, this writer remembers that product launches always generated a certain degree of hype after the traditional five-year gestation cycle.

Still, the odds are that this time the sheer number of products will confuse the customer, contrasting with the Tesla approach of selling a few highly popular products in order to build scale as the company prepares to move into the mid-market segment with the yet to be confirmed Model 2.

The key differentiating factor, given Musk’s background, appears to be that Tesla is the only carmaker where hardware and software are truly integrated – the computer on wheels analogy.

On this point, this writer has to admit to never having met a customer who did not like driving their Tesla which also explains why the company, with the up to 12 months waiting list for its vehicles, can, in another disruptive act, afford to bypass completely the traditional auto dealer network.

Indeed the satisfied customers seem to perform the role of brand ambassadors.

2022 Will be the Year of EV Production at Scale for Tesla

If 2022 is the year when legacy carmakers will scale up on their EV offerings, it is also the year when Tesla production should scale up with the pending opening of the Giga factories in Austin, Texas and Berlin, the latter after a six-month delay, as well as the further expansion of the Shanghai plant.

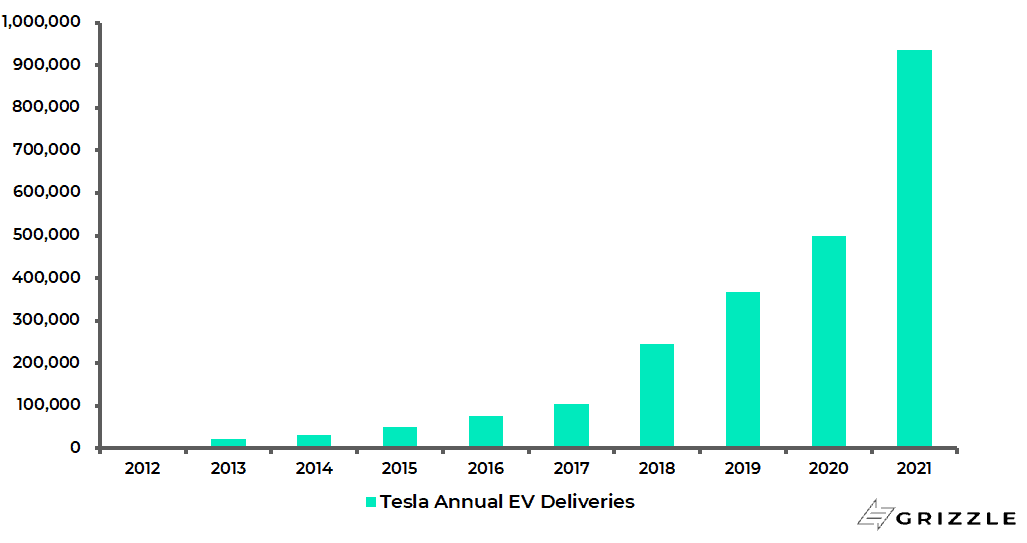

Analysts are forecasting sales of 1.375m this year following reported sales of 936,172 in 2021.

But this writer has seen forecasts of 1.6m units delivered in 2022. And the more vehicles produced, the greater the decline in fixed costs per sale and the greater the resulting operating leverage.

Tesla annual EV deliveries

Meanwhile in another Tweet recently from another account known as “Tesla Opinion”, Tesla followers were reminded that the company repaid in 2013 a US$465m loan with interest from the Department of Energy, due in 2022, nine years ahead of schedule (see The Verge article: Tesla repays $465 million government green energy loan ahead of schedule, 22 May 2013).

The purpose of the tweet was also to remind people that similar loans from the Department of Energy designed to encourage electric vehicle development remain mostly unpaid many years later, namely US$5.9bn extended to Ford, US$1.45bn to Nissan and US$529m to the now-forgotten Fisker.

The same tweet also referred to the 2008 taxpayer-funded bailouts of GM and Chrysler to the tune of US$17.4bn and $13.4bn, respectively.

This writer has to admit to having been somewhat put off by the whole electric vehicle story in recent years because of the interventionist policies designed to promote it, such as carbon offsets or carbon emission targets.

On that point, it is also worth recording that Musk in November declined the German government offer of €1.1bn subsidies to build the Berlin plant.

Tesla said in late November that it had withdrawn its application for state funding for its Berlin factory.

Gov’t ESG Programs Could be Highly Inflationary

The Tesla success demonstrates, of course, that most of these government programmes are unnecessary and worse anti-competitive, as would definitely be the case if the US$12,500 tax credit for electric vehicles built in unionised factories in America which was part of the proposed Build Back Better legislation ever becomes law.

But on the other hand, many of the current government efforts to force energy transition may well end up, as previously argued here (Inflation Ain’t Falling While Rents, Wages and Commodities Are On The Rise, 3 November 2021), proving highly inflationary, most particularly if they are indirectly financed by central banks pursuing politically fashionable green agendas.

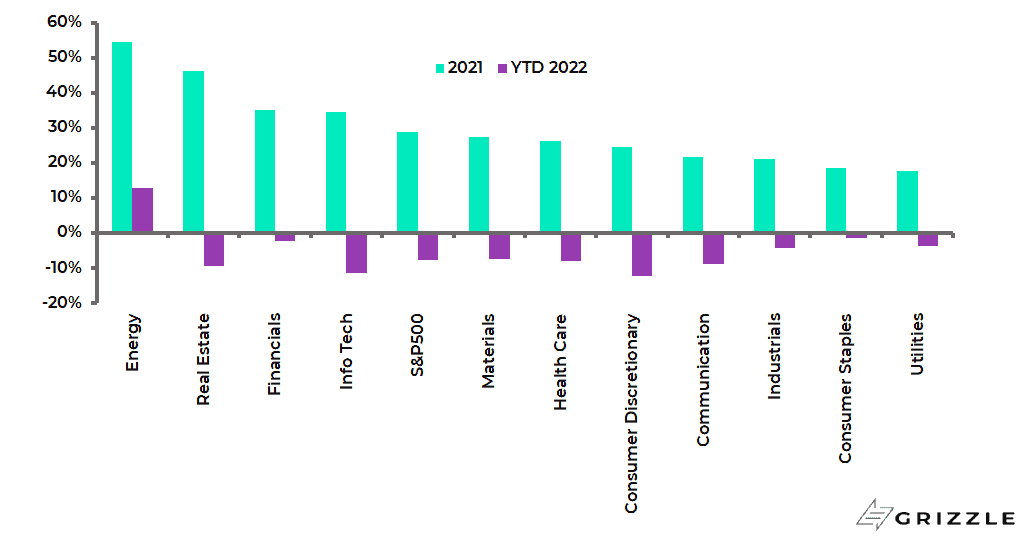

In that respect, this writer remains positive on energy and energy stocks in 2022 even though this was the best performing S&P sector in 2021 (up 55% on a total-return basis compared with a 29% gain in the S&P500) and is again the best performing sector year to date (up 13% compared with an 8% decline in the S&P500).

The biggest risk to that trade in energy stocks remains not Fed tightening but the meanderings of the pandemic.

S&P500 sector performance 2021 and Year-to-date 2022 (total-return basis)

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.