In America of late, I was in situ long enough to catch a lot of the impeachment proceedings and the relevant media coverage. It is not news. But it remains truly remarkable how polarized the political debate and the related media coverage is, with CNN and Fox TV the relevant outliers.

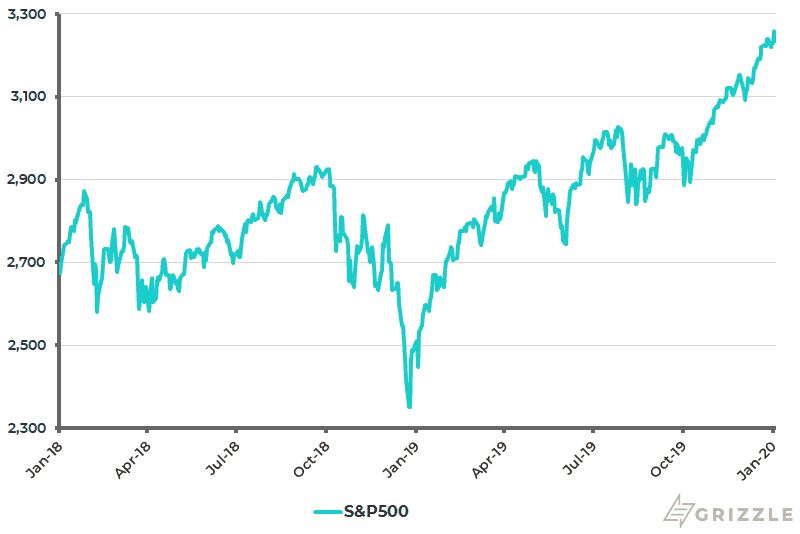

The coverage of the impeachment is a good example of these parallel universes. The New York Times’ front page coverage on Nov. 21 of the testimony of America’s EU ambassador Gordon Sondland, with the banner headline “We followed the President’s orders”, implied that some great historical moment had arrived. I have remained underwhelmed, as has the American stock market (see following chart), while there remains scant evidence of Republican support for the President wavering.

Indeed, some reports have suggested that the strategy of the 45th president is to go on the offensive when the impeachment proceedings reach the Senate this month with the Republican head of the Senate Judiciary Committee, Lindsey Graham, acting as the Donald’s pit bull. This could lead to intense focus on the activities of Joe Biden’s son Hunter in Ukraine.

S&P500

With the Congressional testimony focused on the issue of the alleged “quid pro quo”, there is no doubt that the Donald has made himself somewhat vulnerable to such allegations as a result of his transactional view of foreign policy. But this is more a reflection of his modus operandi rather than constituting a reason to impeach. Indeed the Donald clearly thinks he has done nothing wrong, which is why he was so quick to release the original transcript of his July telephone call with Ukraine President Volodymyr Zelensky.

Meanwhile, the testimony of the professional U.S. diplomats, and the questions of the Democratic Congressmen, make it sound like Ukraine is some completely independent country threatened by a hostile Russia. While this is the Washington narrative, the realpolitik of the situation is that Ukraine is as much in the Russian sphere of influence as, say, Puerto Rico is in America’s. This is obvious to anyone who has ever visited Kiev, which is full of Russian Orthodox churches.

Balance Sheet Expansion and M2 Growth

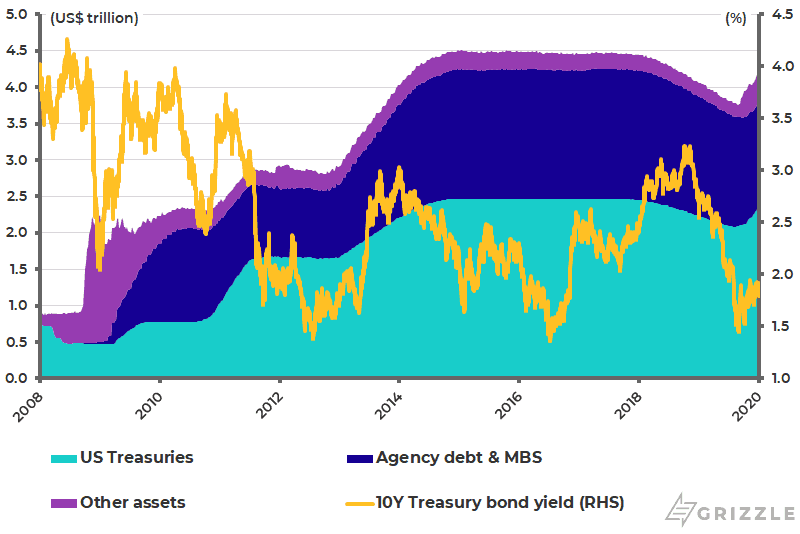

The American stock market has completely ignored the impeachment noise and continued to rally, supported by the Federal Reserve’s renewed balance sheet expansion. After contracting the balance sheet by US$711 billion or 16% between September 2017 and August 2019 to US$3.76 trillion, the Fed’s balance sheet has already risen by US$414 billion or 11% to US$4.17 trillion since bottoming in late August (see following chart).

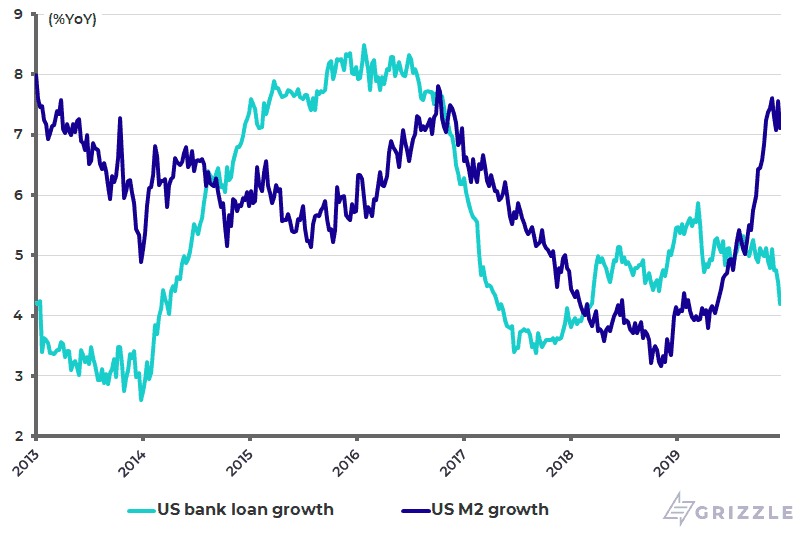

It is also worth highlighting that US M2 growth has accelerated from 4.0% YoY to 7.1% YoY in the past seven months (see following chart), though at present there has not been a related pick up in loan growth. Indeed bank loan growth slowed from 5.3% YoY to 4.2% YoY over the past seven months (see following chart).

U.S. M2 Growth and Bank Loan Growth

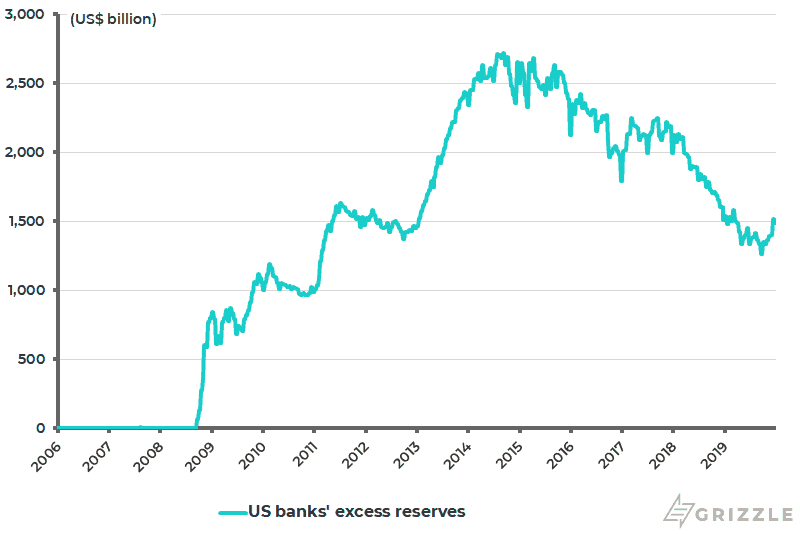

The main driver of this pick up in M2 growth has been banks buying more assets such as treasury securities as their excess reserves have declined. U.S. bank holdings of Treasury and agency securities rose by 11.3% YoY in late December, while banks’ excess reserves have declined by 45% from a peak of US$2.72 trillion in September 2014 to US$1.49 trillion in late December, though up from a recent low of US$1.26 trillion reached in late September (see following chart).

U.S. Banks’ Excess Reserves at the Fed

The above development is something to monitor. Combined with the renewed Fed balance sheet expansion where the Fed is buying US$60 billion of short-term Treasury bills a month, it means more money in the system which supports “risk on”. It also means the benefit of the doubt should for now probably be given to a further steepening of the yield curve.

Federal Reserve Balance Sheet and 10-year U.S. Treasury Bond Yield

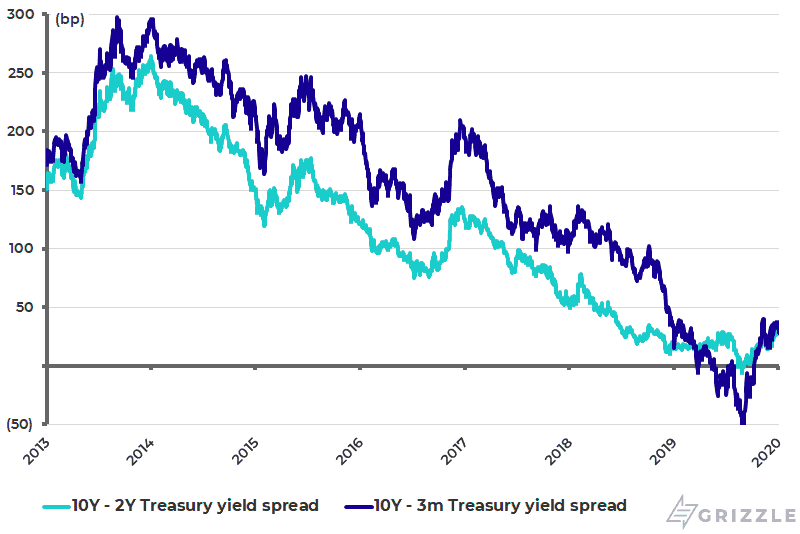

In this respect, it is worth remembering that quantitative easing is bearish for Treasury bonds in the first instance because it involves a loosening of monetary policy. Similarly, quantitative tightening is bullish for Treasury bonds because it involves monetary tightening. This counterintuitive dynamic can be seen in the attached chart (see previous chart). It is counterintuitive because the Fed is buying Treasury bonds during quanto easing, or in the case of its recent renewed balance sheet expansion short-term Treasury securities, and the Fed was selling Treasury bonds during the recent experience of balance sheet contraction. It is also the case that the Fed’s renewed buying only at the short end helped lead to yield curve steepening. The spread between the 10-year Treasury bond yield and the 3-month Treasury bill yield rose from a low of negative 50bp in late August to 0bp on Oct. 10 prior to the Fed announcement of renewed Treasury bill purchases. It has since then risen to 28bp.

U.S. Yield Curve

“Risk On” Depends on the Trade Deal Closing

Still the case for continuing “risk on” is subject to a US-China trade deal being concluded. For now, the so-called “phase one” deal is a marginal positive because more tariff hikes were avoided, as expected, and some existing tariffs were moderated. It is also a positive for market sentiment that Donald Trump tweeted on Dec. 31 that the deal will be signed on Jan. 15. This is because the text of the agreement has not yet been published, let alone signed.

It needs to be remembered that America will still be left imposing 7.5-25% tariffs on US$370 billion of Chinese goods. Markets will be hoping that these tariffs will be removed in the mooted “phase two” deal. But the key word here is hope. It is also the case that “phase one” does not address the national security issues, such as Huawei and 5G. Yet these tensions probably pose a greater longer term threat to the US-China relationship than the argument over trade.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.