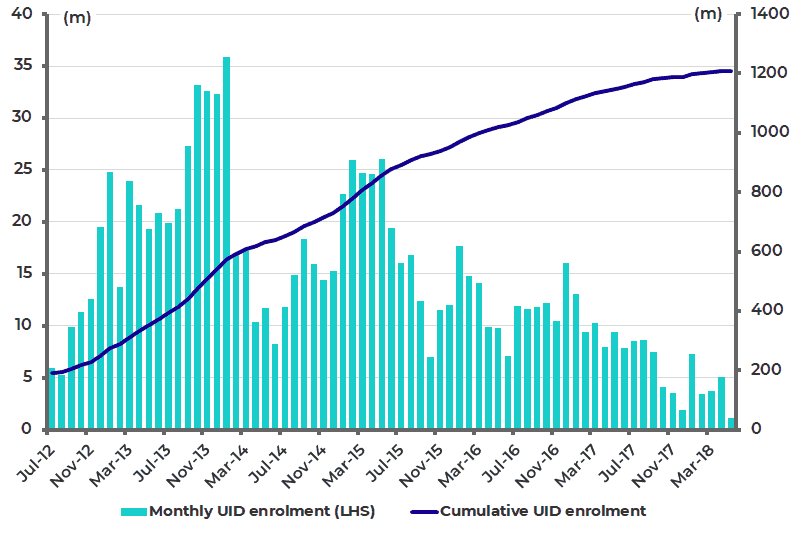

India has long been this writer’s favourite stock market in Asia. It also has a feature unique in emerging markets: an electronic ID card system in which 1.2 billion of its citizens (92% of the population) have been issued with such cards (see following chart).

India Monthly UID and Cumulative UID Enrolments

Aadhaar: Creating a theme of digitalization and development

The electronic ID card system, known as Aadhaar, is not without controversy. Some 84 cases have been filed in India’s Supreme Court against it. The cases seem to be politically driven against the current BJP Government of India Prime Minister Narendra Modi with one of the litigants former Congress finance minister P. Chidambaram, a lawyer by profession.

The litigation raises issues of invasion of privacy and Big Brother. This is somewhat ironic since Aadhaar was originally a Congress Government-supported initiative launched in 2009 by Infosys co-founder and former CEO Nandan Nilekani, who has now returned as the famous software company’s chairman. Congress is the party associated with India’s most famous political family, the Gandhis.

As Big as Google and Facebook

There is a fundamental difference between Aadhaar and the likes of Google and Facebook which is worth highlighting. Google, Facebook, and Aadhaar are the only three user systems in the world with more than a billion users each. This difference was spelled out in an interview in April with Ajay Bhushan Pandey, chief executive officer of India’s Unique Identification Authority (UIDAI).

Apart from the difference that Aadhaar is in the public sector, and Google and Facebook are not, Aadhaar performs primarily an ‘enabling role’ collecting minimum data at the time of enrolment and at the time of identification. This data comprises basic demographics (e.g. name, age, gender) and basic biometrics (e.g. fingerprint).

Aadhar is About Empowerment, Not Big Brother

It is not in the business, so beloved by Facebook and Google, of collecting all sorts of personal information to feed the inquisition algorithms. Indeed collecting such information is illegal under the Aadhaar Act, according to Pandey (see Business Standard article “Aadhaar is for empowerment, not Big Brother”, April 17, 2018).

The above is a critical distinction which is why, in this writer’s view, sooner or later the focus will return on how to regulate the social media giants. At the very least, the companies will be made to pay for the data they collect assuming, as is now required in Europe, that people agree to the processing of their data for marketing purposes. Clearly, collecting data on users to enable targeted advertising is central to the business model of these companies.

Building the World’s Largest Health Care Program

Meanwhile, the existence of Aadhaar has allowed the Modi Government to develop so-called Direct Benefit Transfer (DBT) whereby transfer payments are made to recipients electronically, thereby preventing ‘leakage’ to unscrupulous middlemen.

Aadhaar provides an opportunity to build a different kind of welfare system from the ground up. Thus the latest Indian budget, announced in February, contained an interesting proposal to start a National Health Protection Scheme to cover over 100 million poor families that would provide health coverage up to Rs500,000 (US$7,500) per family per year for secondary and tertiary care hospitalization. This will, if implemented, be the world’s largest government-funded health care program.

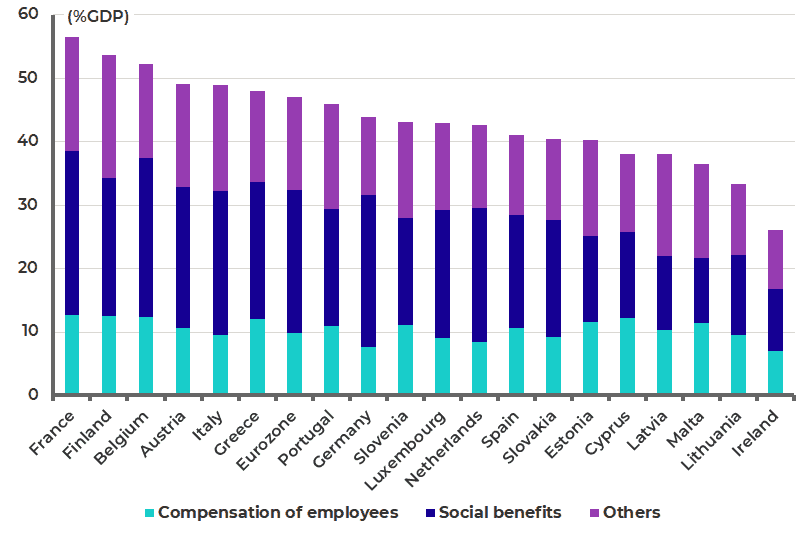

Welfare systems can be extremely expensive, as any observer of the developed economies can attest, with the average government spending in Eurozone countries now running at 47% of GDP (see following chart). But Aadhaar offers India a chance of building a much sounder system while replacing the waste (in the form of leakages) in the current system.

Eurozone General Government Expenditure as % of GDP (2017)

India Stock Market

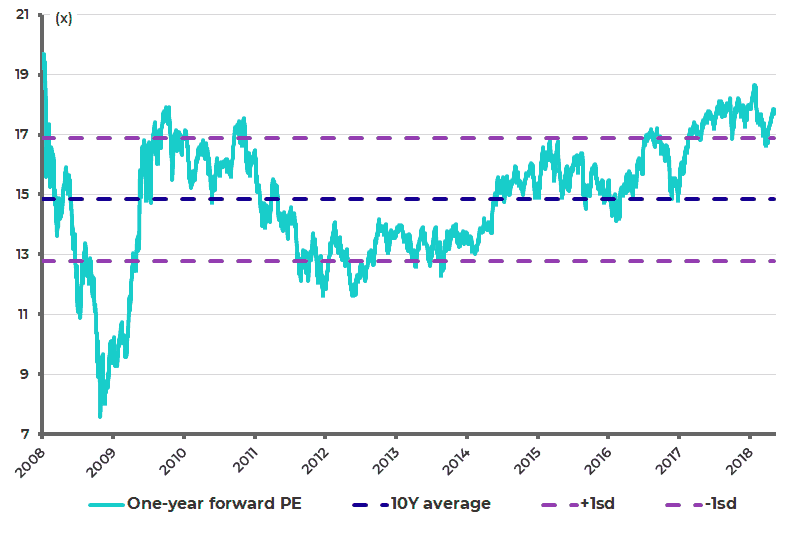

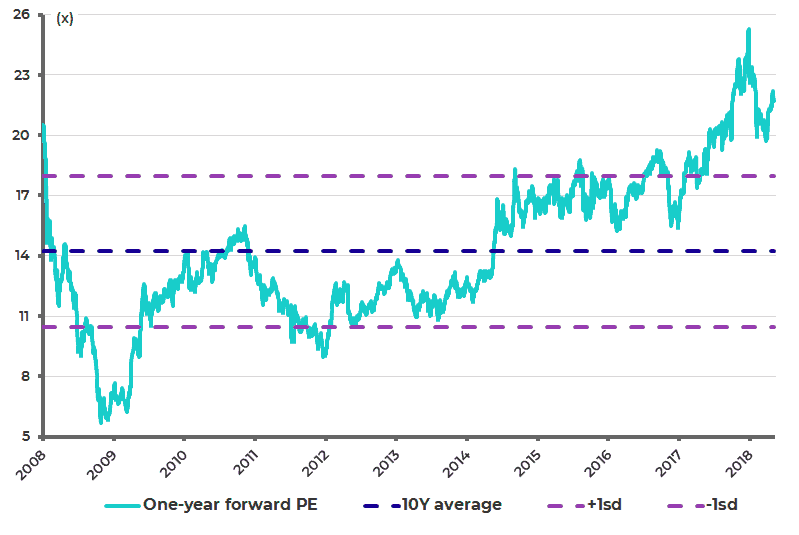

What about the India stock market? Valuations are high, most particularly in the mid-cap space, though not as high as they were at the peak earlier this year. The Nifty Index and the Nifty MidCap 100 Index now trade on 17.7x and 21.7x one-year forward earnings, down from a peak of 18.6x and 25.3x reached in January and late December respectively (see following charts).

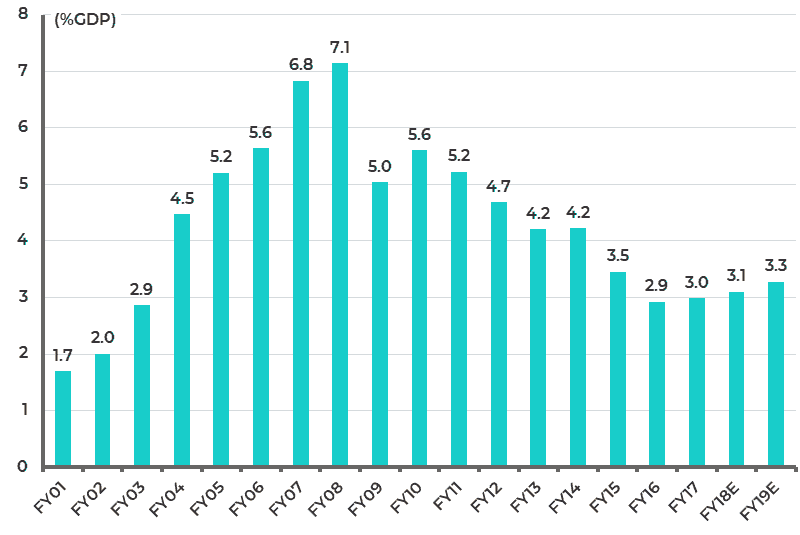

Still, the mitigating factor continues to be that corporate profits as a percentage of nominal GDP remain comparatively depressed, declining from 7.1% in FY08 to 3.0% in FY17 and an estimated 3.1% in FY18 (see following chart). This reflects the lack of a new investment cycle because of problem loans in the banking system. Hence, corporate profits as a percentage of nominal GDP peaked in fiscal 2008, which was the peak of the last investment cycle. But as any visitor to India will quickly understand, a new investment cycle is only a matter of time.

It also remains the case that the commencement of a new investment cycle becomes much more likely if the NPL overhang in the banking system, concentrated on the public sector banks is resolved. This finally seems to be happening.

Nifty Index One-year Forward PE

Nifty MidCap 100 Index one-year forward PE

India Corporate Profits as % of GDP

India Annualized Gross Fixed Capital Formation as % of Nominal GDP

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.