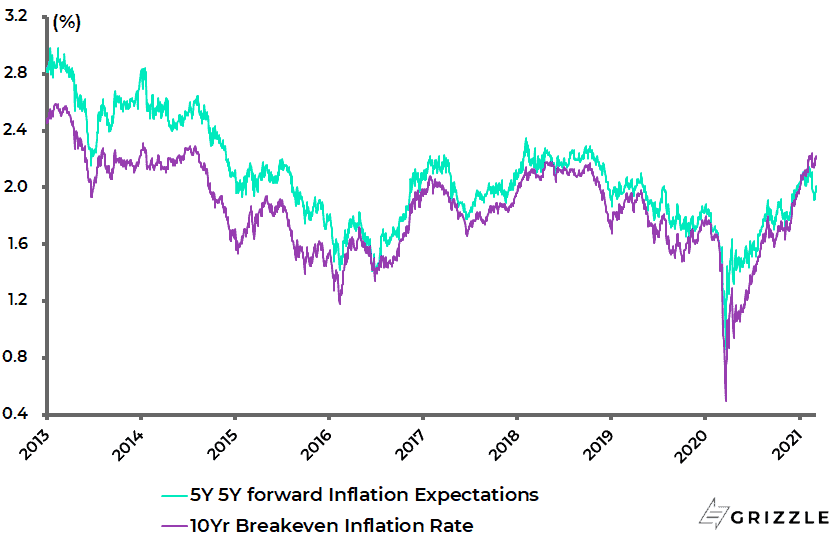

Inflation expectations remain the key variable to monitor.

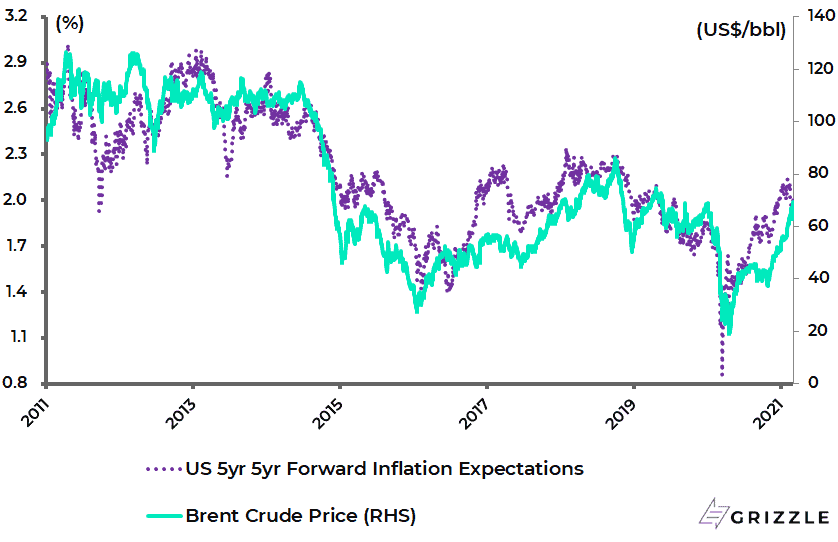

The US 5-year 5-year forward inflation expectations rate and the 10-year breakeven inflation rate have risen by 13bp and 16bp respectively since late January to a recent high of 2.14% and 2.24% on 5 February and 16 February and are now 2.01% and 2.22%.

US 5Y 5Y Forward Inflation Expectations Rate and 10Y Breakeven Inflation Rate

Indeed the 10-year breakeven inflation rate is now at its highest level since August 2014 and has for some time been sending the signal that long-term bond yields are heading higher.

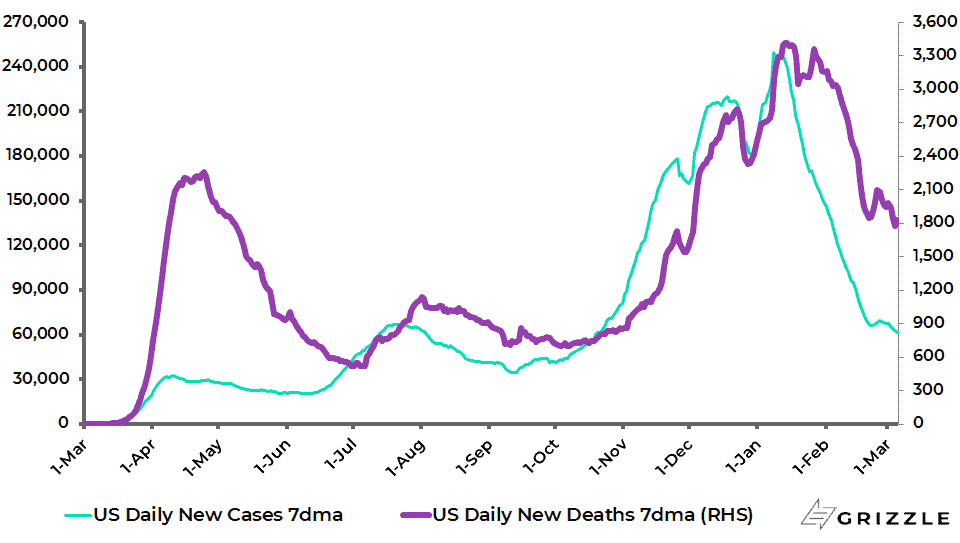

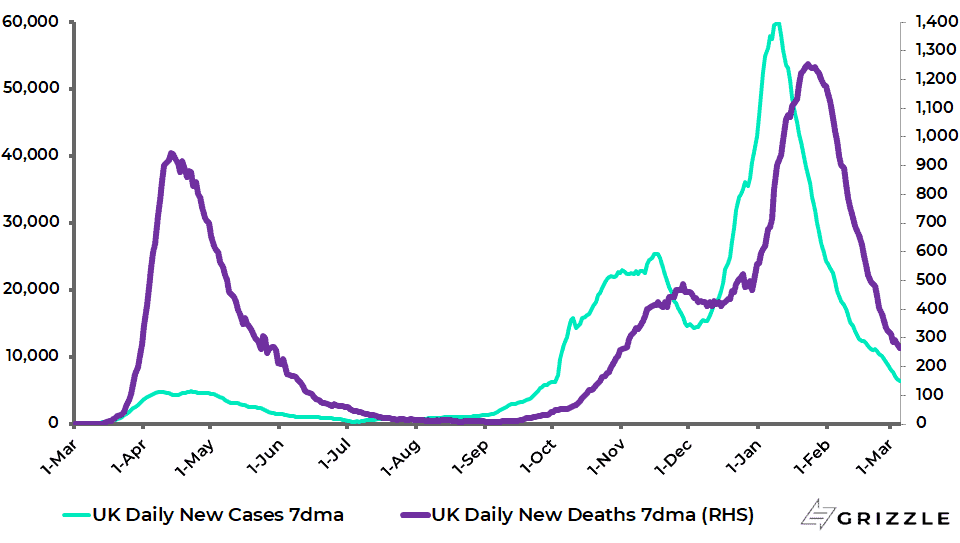

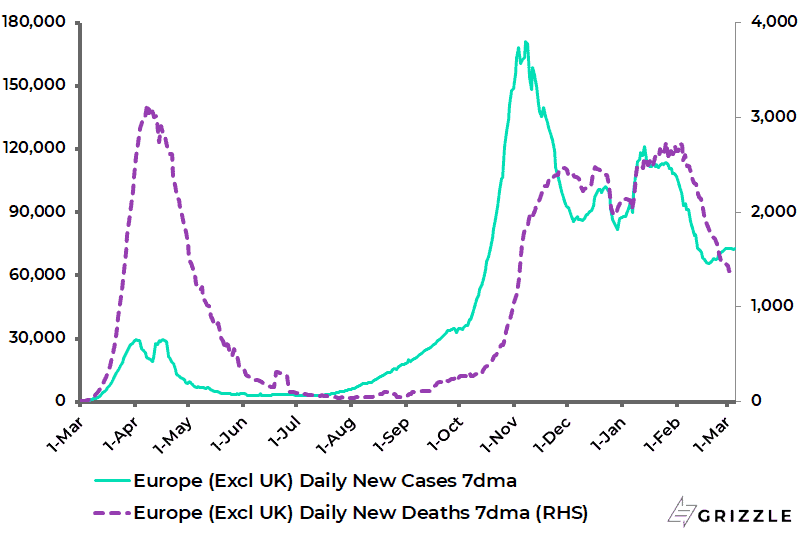

The above action is supportive of the re-opening trade as is, despite the legitimate continuing concerns about new variants, the increasingly evident collapse in new cases in both America and Europe, as well as of course the ongoing rollout in vaccines.

US Covid 7-day Average Daily New Cases and Deaths

The 7-day average daily new Covid case count in America has now declined by 76% from the peak reached on 8 January, while the 7-day average daily case count in the UK is down 89% from its 9 January peak.

UK Covid 7-day average daily new cases and deaths

As for Europe ex-UK, the 7-day average daily case count has declined by 40% from the recent high reached on 13 January and is down 58% from its November 2020 peak.

Europe ex-UK Covid 7-day average daily new cases and deaths

Note: Europe excl. UK includes Italy, Spain, Germany, France, Switzerland, Netherlands, Austria, Belgium, Norway, Sweden, Denmark, Portugal, Ireland, Luxembourg, Finland and Greece. Source: Johns Hopkins University

$1.9Tn Stimulus Not the End of Government Subsidies

Then, in a further support to the cyclical trade, the Democrats look increasingly likely to push their US$1.9tn fiscal stimulus through Congress via the so-called reconciliation process by 14 March at the latest (Update: The bill was approved on March 12th), which is when the latest set of emergency unemployment benefits expire.

That is not the end of the anticipated coming fiscal stimulus from the Biden administration.

Remember the proposed US$1.9tn package is narrowly focused on Covid relief. Then there is talk of an up to US$2tn infrastructure stimulus later this year which is likely, in part, to be financed by stock market unfriendly tax hikes.

Meanwhile, with projected fiscal stimulus soaring, the Fed chatter continues to follow the dovish playbook even though Fed officials have conceded of late that inflation is likely to surpass the 2% level in March and April because of the base effect, though it still is assumed that this will prove transitory.

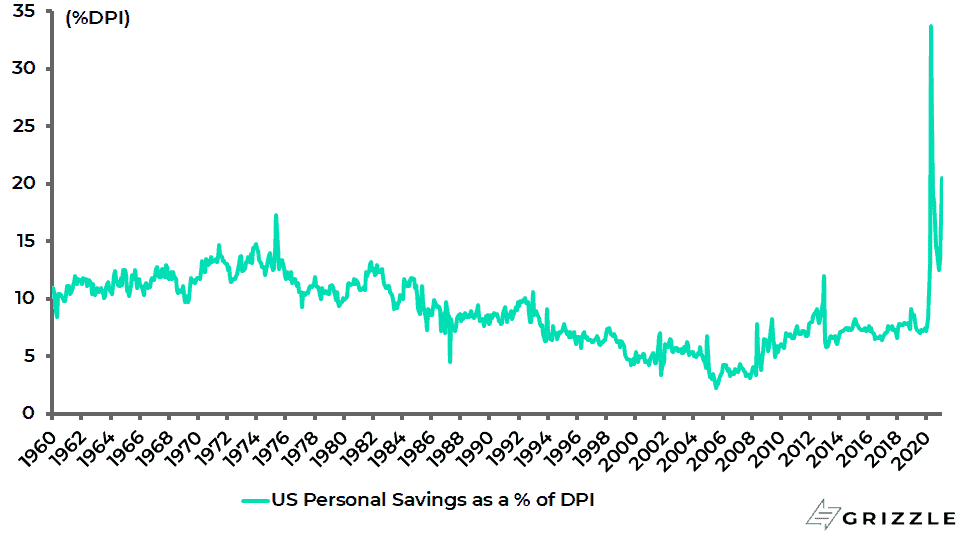

That said, there is in this writer’s view every potential for a surprising large pop in prices on an economic reopening in the context of a US personal savings rate of 20.5% in January, ongoing massive monetary and fiscal stimulus and a resulting likely explosion in pent-up demand.

US Personal Savings Rate

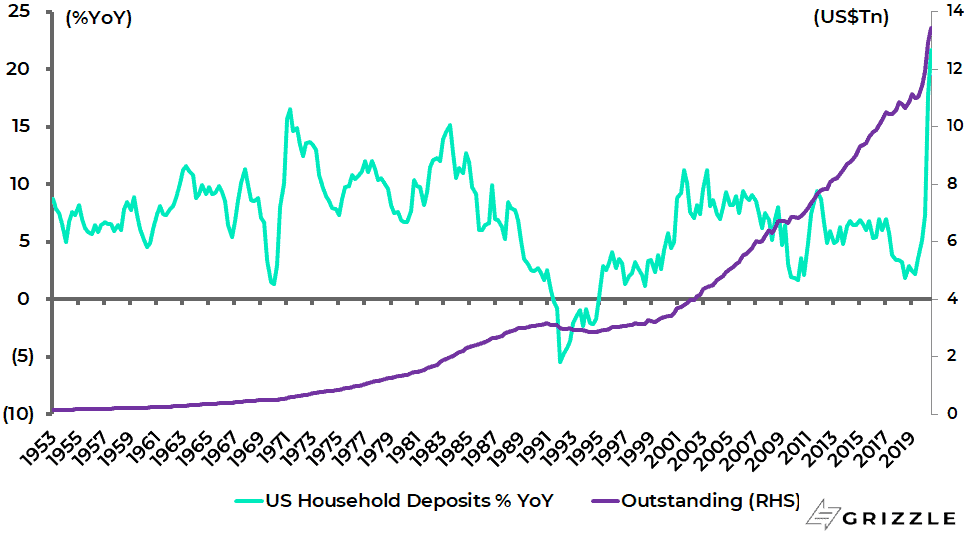

In this respect, as good a gauge as any for a pickup in demand is the surge in household deposits courtesy of higher savings rates and increased transfer payments.

US household deposits rose by 21.7% YoY to US$13.4tn at the end of 3Q20, the latest data available.

US Household Deposits

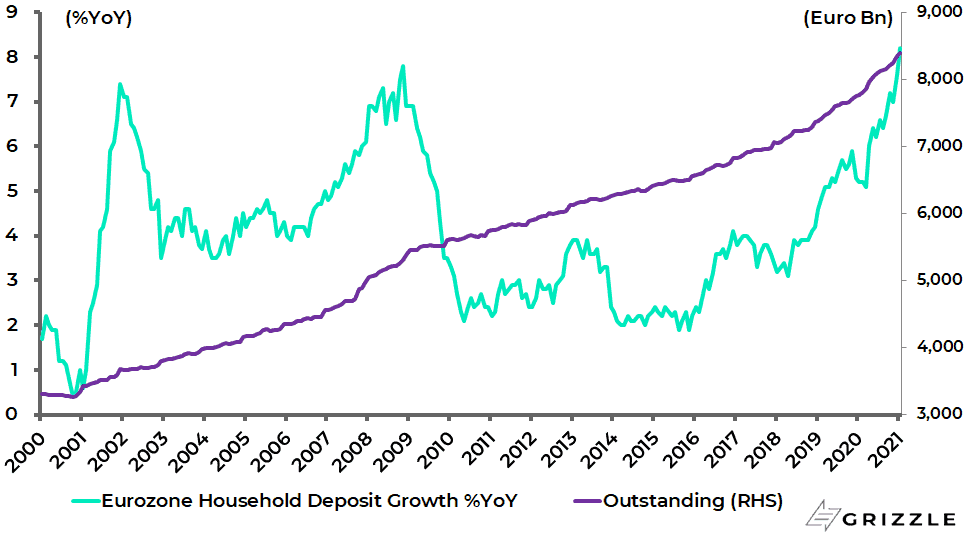

While Eurozone household deposits rose by 8.2% YoY to €8.39tn at the end of January.

Eurozone household deposits

This is why the key issue for financial markets in 2021 remains how Federal Reserve chairman Jerome Powell reacts when all this becomes self-evident, as it will sooner rather than later.

Certainly, if inflation expectations reach the 2.5% level there is going to be more pressure on the Fed to make clear exactly what is the tolerable level of overshoot above the 2% inflation target; though this may also be precisely the moment when the deflation obsessed doves on the Fed will want to implement yield curve control.

In the meantime, it is interesting that former Treasury Secretary Larry Summers last month raised the overheating risk for the American economy from the proposed US$1.9tn package (see Washington Post op-ed: “The Biden stimulus is admirably ambitious. But it brings some big risks, too”, 4 February 2021).

Among several other points made, Summers stated that “there is the risk of inflation expectations rising sharply”.

But current Treasury Secretary Janet Yellen seems less concerned.

Her political orientation was made abundantly clear in a letter she wrote to the 84,000 Treasury Department employees on her taking up office which stated, among other things, that:

If Summers’ concerns about overheating are realised on the economic reopening, the prescription from the progressive wing of the Democrat Party will be to address it with higher taxation not monetary tightening, as advocated by believers in Modern Monetary Theory (MMT).

Energy Stocks and Airlines as Good as Any to Own on Reopening

Meanwhile, as part of the current rotation in cyclical stocks, energy stocks have been rallying as the Brent crude oil price reached nearly US$70 last week (US$69.69/bbl on Friday).

In this respect, it is also noteworthy that there is a long-run correlation between the oil price and US inflation expectations.

To be precise, the correlation between the Brent crude oil price and the US 5-year 5-year forward inflation expectation rate has been 0.90 since 2011.

Brent Crude Oil and US 5Y 5Y Forward Inflation Expectations Rate

This is why a rising oil price is likely to increase the inflationary noise and related pressure on the Fed.

It is also interesting to ask where oil will be if the world really re-opens, given that it has almost reached the US$70 level with global travel still all but locked down, with the major driver for higher prices so far being reduced supply rather than rising demand.

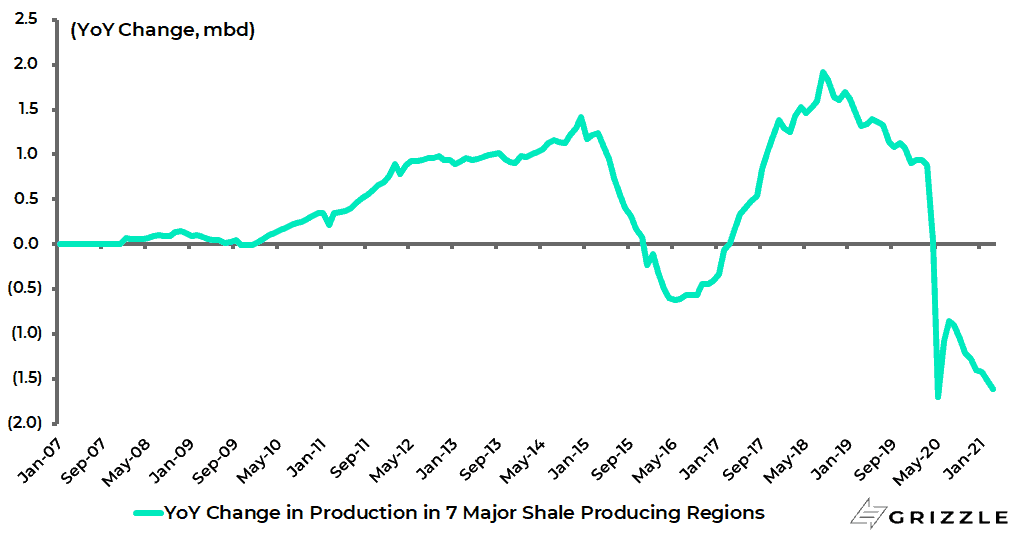

In addition to the Saudi trigged OPEC supply curbs announced in January, US shale production continues to decline.

The Energy Information Administration’s latest Monthly Drilling Productivity Report shows that US shale oil production fell by 1.43m barrels/day in the 12 months to January and is projected to decline by 1.62m barrels/day in the 12 months to March.

YoY Change in US Oil Production in 7 Major Shale Regions

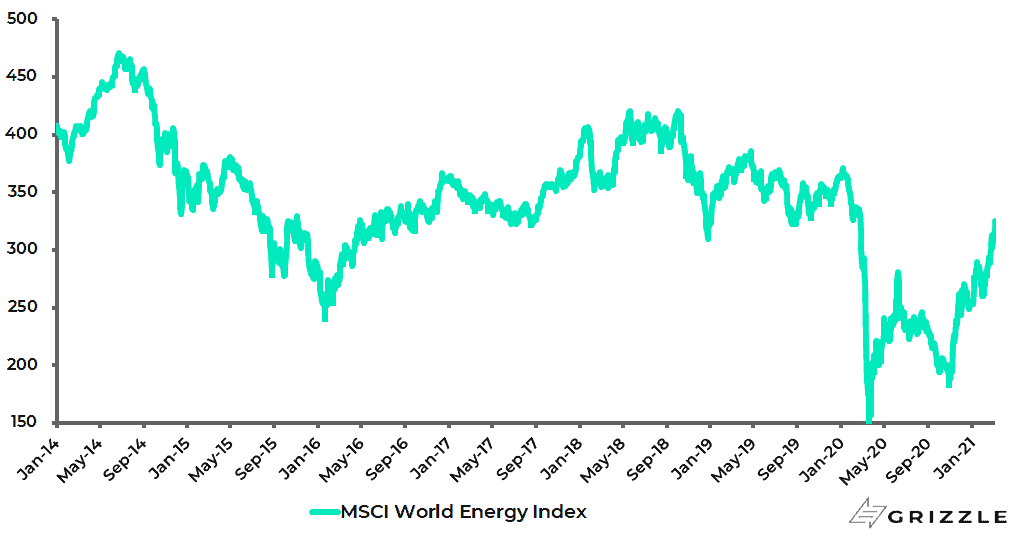

As for energy stocks, they have rallied dramatically from their late October lows.

The MSCI World Energy Index has risen by 77% in US dollar terms on a total-return basis from its recent low in late October.

MSCI World Energy Index (total-return basis)

Energy stocks, along with airlines, remain as good as stocks to own as any on the back-to-normal trade.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.