If an inflation scare is coming, it did not come with the March CPI inflation report which was a non-event in terms of market impact.

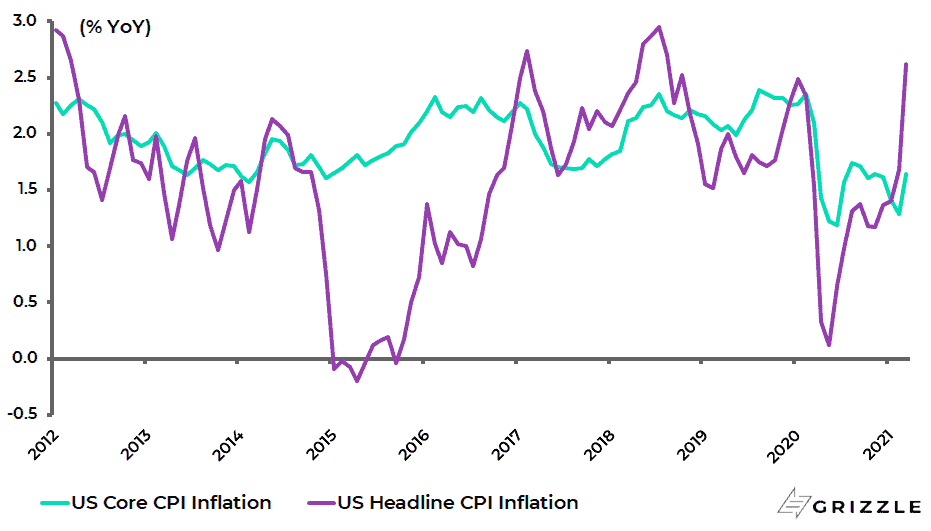

US CPI came at slightly above consensus at 2.6% YoY.

It was also the highest reading since August 2018. But the base effect had been fully signaled by a chorus of Fed speakers in recent weeks and indeed months.

US Headline and Core CPI inflation

In fact, the number of speeches by Fed governors has been growing on a daily basis as they seek to make the case in public for their new approach to monetary policy as a result of the American central bank’s strategic review completed last year.

This new approach includes not only the licence to overshoot 2% and the jettisoning of the Phillips curve but also a recently conceived obsession with targeting the ‘inclusive’ nature of employment.

Meanwhile, it is worth highlighting that US headline and core CPI have risen by an annualised 5% and 1.9%, respectively, over the past three months.

The base effect means that, even assuming a flat MoM change in the next two months, headline and core CPI will rise to 3.5% YoY and 2.1% YoY in May.

Still, the inflation numbers will become very important when the base effect, on a year-on-year basis, moves out of the data.

This should be from the month of June and that number will be reported in mid-July.

During the interim investors should continue to keep a close eye on market-driven inflation expectations, as previously discussed here on several occasions.

The new Fed approach, and the obvious desire of the American central bank to see a pickup in inflation, is also why it remains beyond this writer why anybody should want to own a G7 government bond anymore.

Unless, of course, they believe the vaccines will prove totally ineffective against Covid, in which case Treasuries will have a monster rally.

But that is not the base case here.

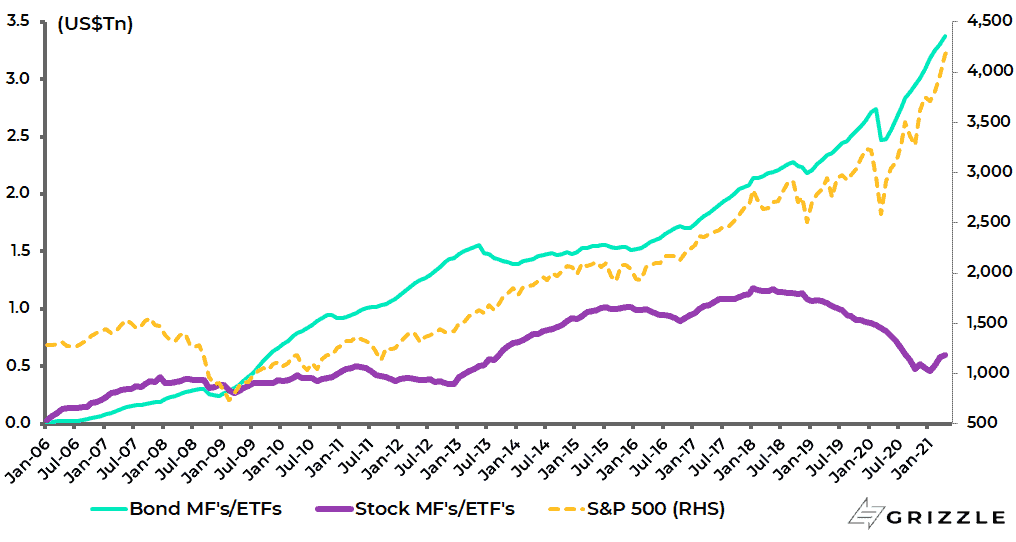

Meanwhile, the chart below serves as a useful historic reminder that, since the S&P500 bottomed in March 2009, flows into equity mutual funds and ETFs in the US have been way below the same flows into bond funds.

This shows the potential for a massive allocation from bonds to equities if inflation does really return on a longer-term basis.

Thus, cumulative net inflows into equity mutual funds and ETFs in the US have totaled US$325bn since April 2009, compared with US$3.1tn of net inflows into bond funds over the same period, according to data from Investment Company Institute.

US mutual funds and ETFs cumulative net inflows since 2006 and S&P500

The Pandemic Scorecard

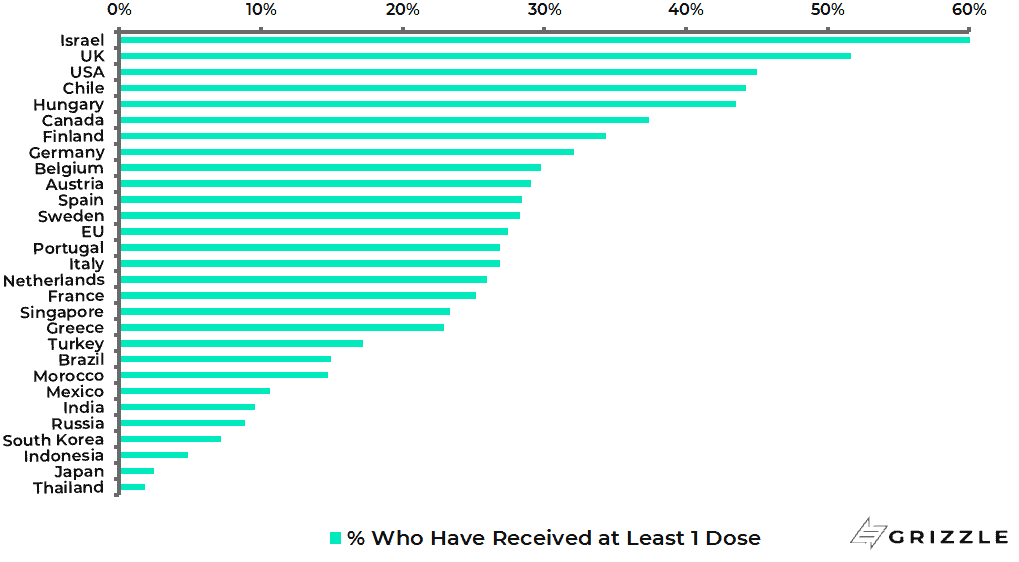

Refocusing on the pandemic, the vaccine rollout continues. But the chart below makes it clear that, in terms of the major economies, America and Britain remain well ahead of the game.

Indeed the success of Operation Warp Speed, conceived in the spring of 2020, is a great example of the American ‘can do’ attitude at work.

Unfortunately, it is also clear that emerging markets are laggards.

There are two problems here.

The first is the availability of vaccines in countries with large populations.

The second is that a lot of ordinary people in developing counties are wary of taking the vaccine.

This problem has become more critical of late as cases in India, for example, have continued to surge indicating the spread of more infectious new variants.

Share of Population Received at Least one Dose of Covid Vaccine

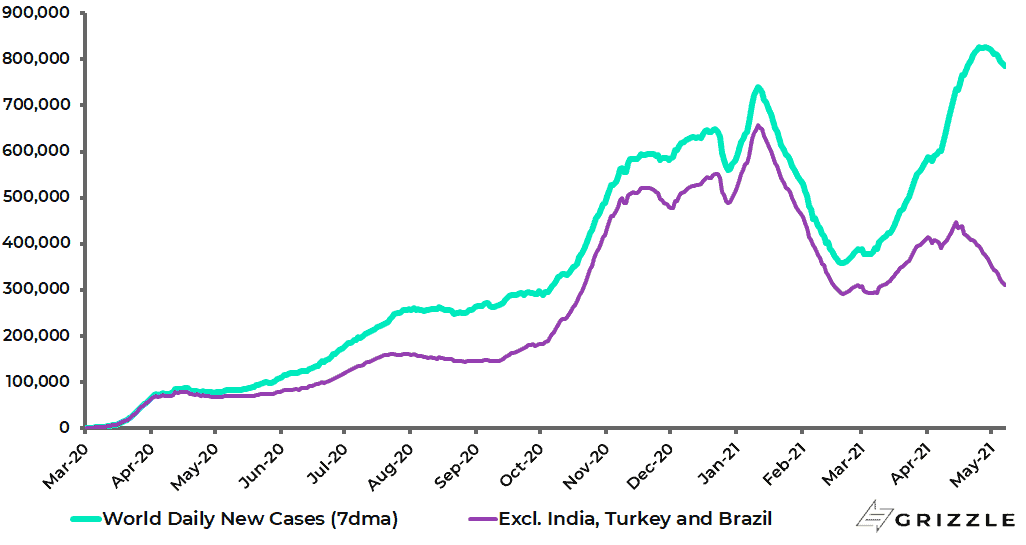

The result is that Covid cases are now rising again on a global basis which was not the case as recently as late February and this pick up is mainly due to India, Turkey and Brazil.

The 7-day average daily Covid case count globally bottomed at 358,583 on 20 February and has since risen by 427,446 or 119% to 786,029.

While the 7-day average daily case counts in India, Turkey and Brazil increased by 377,285, 13,435 and 17,931 respectively over the same period, accounting for a combined 96% of the increase globally.

World 7-day Average Daily New Covid Cases

But the key point for markets which are, first and foremost, US driven is that the vaccine rollout continues in America with 45% of the population having received at least one jab.

Meanwhile, it will also become an issue for emerging markets that the messenger RNA (mRNA) technology vaccines of Moderna and Pfizer are not really affordable or indeed practical for many developing countries given that they require sub-zero temperatures.

Yet these vaccines are far more easily tweaked for the new variants.

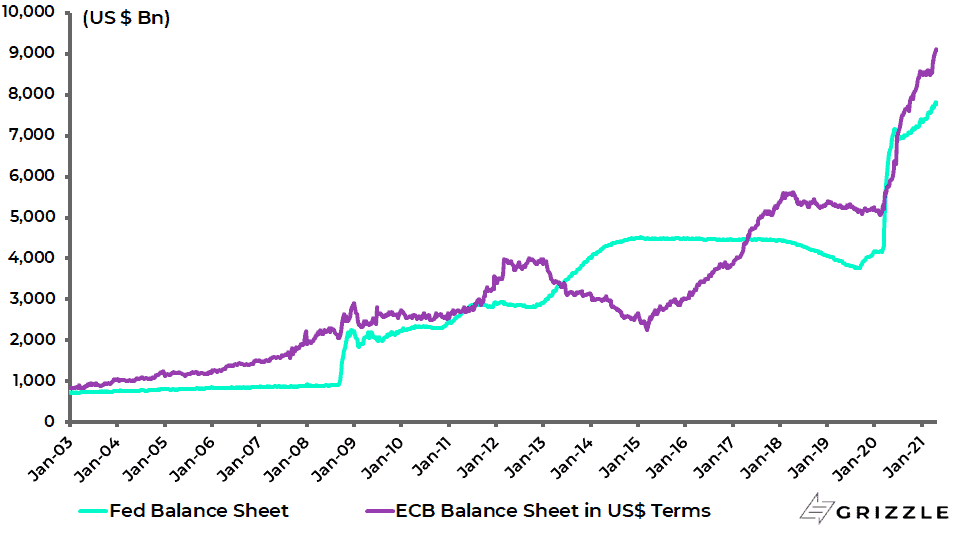

ECB Beating the Fed at the Money Printing Game

Returning to the issue of central banks, the ECB is currently expanding its balance sheet at a significantly faster rate than the Federal Reserve.

The ECB balance sheet has risen by 44% in US dollar terms since mid-June 2020, compared with a only 9% increase in the Fed’s balance sheet over the same period.

This is clearly one argument in favour of the US dollar at present in the relative value game of choosing between paper currencies.

Federal Reserve and ECB balance sheets in US dollar terms

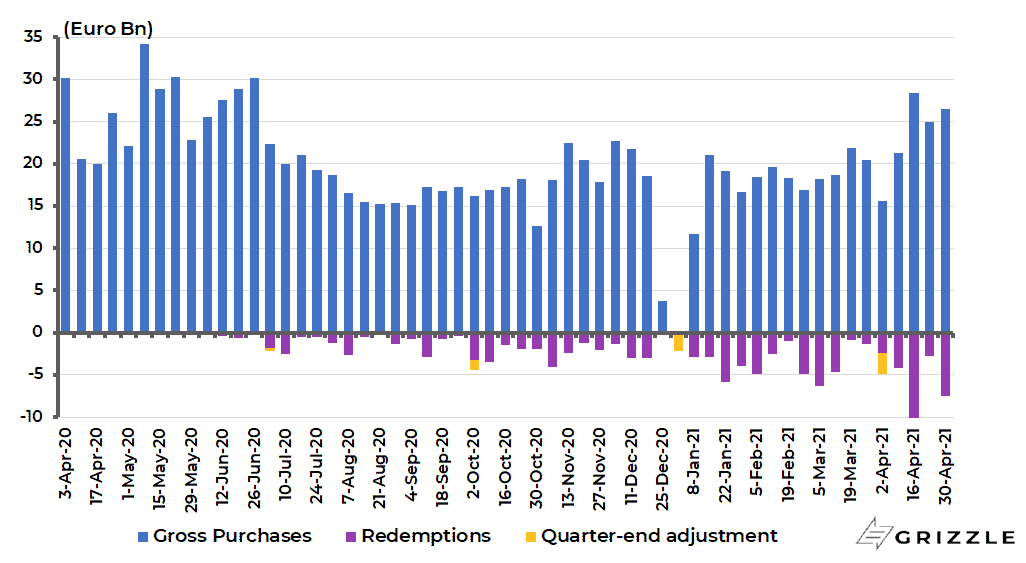

The reason the ECB is expanding faster is the stepped-up purchases of government bonds under its Pandemic Emergency Purchase Programme (PEPP) in what appears to be a policy of closet yield curve control targeting nominal bond yields.

Gross asset purchases under the PEPP rose to €26.5bn in the last week of April and averaged €25.3bn/week in April, compared with an average of €18bn in the year to mid-March.

ECB Weekly Asset Purchases Under the PEPP

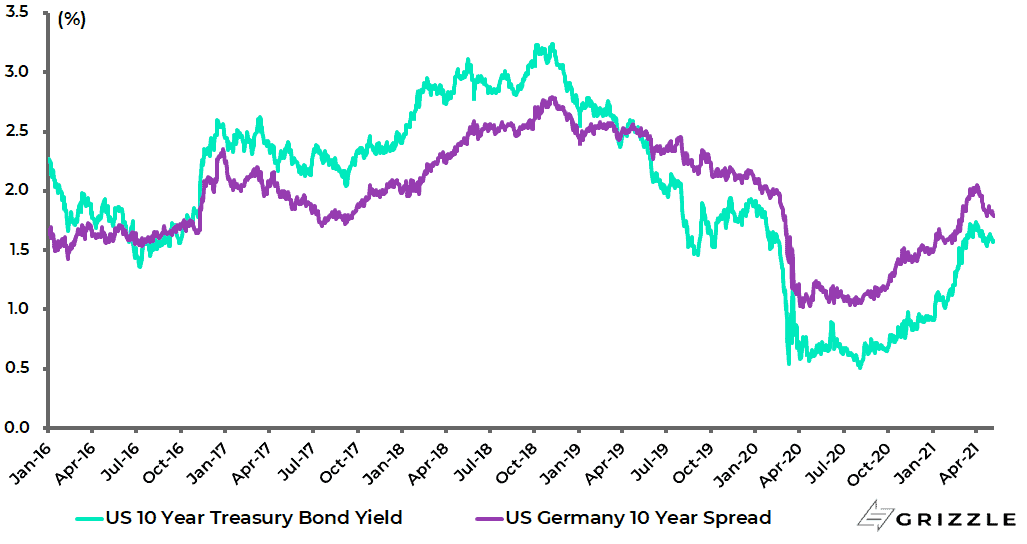

This closet targeting of nominal bond yields in the Eurozone, and no longer just yield spreads between say Italy and Germany, is also euro bearish in the sense that it makes Treasury bonds look more attractive to Eurozone investors given the 66bp back up in the 10-year Treasury bond yield so far this year.

US 10-year Treasury Bond Yield and Spread over German Bund Yield

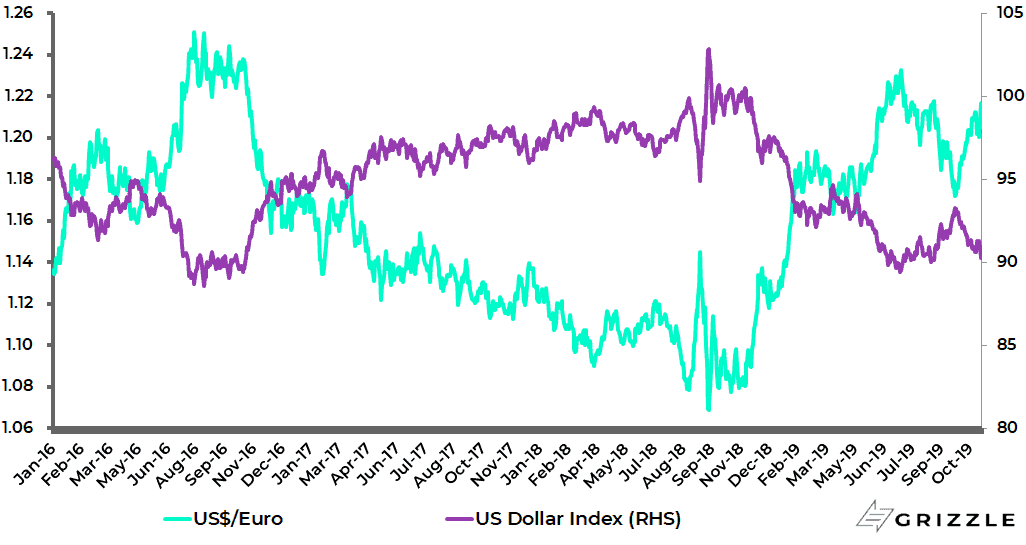

In this respect, it is perhaps a surprise that the euro has not sold off more against the US dollar, especially given the far more successful vaccine rollout in America.

That the euro has not sold off more makes this writer think the dollar remains fundamentally in a longer-term weakening trend.

US$/Euro and US Dollar Index

First, it is the case that the Europeans will surely get their act together in the current quarter on the vaccine rollout.

Indeed there are already signs of this.

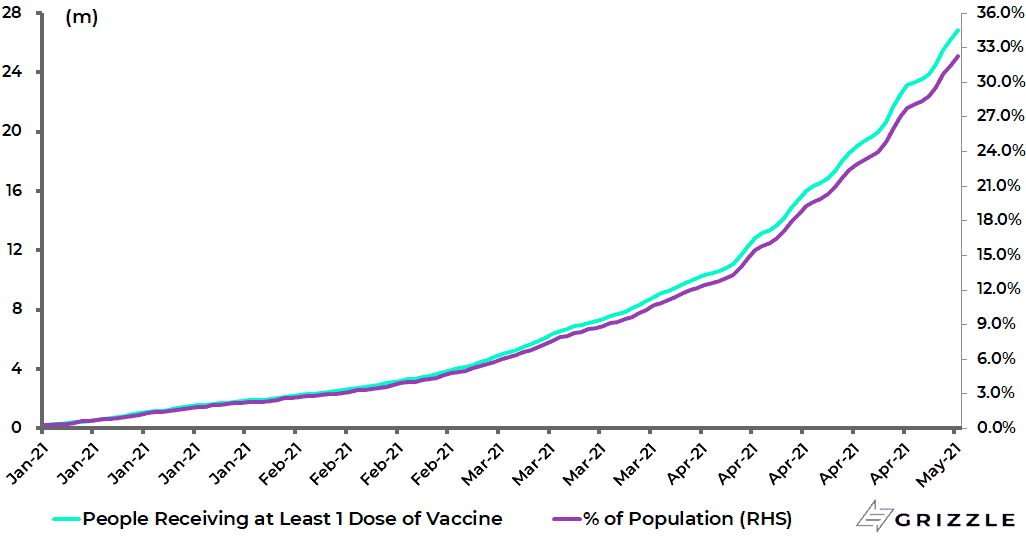

In Germany, the number of people who received their first jab has risen by 130% over the past month to 26.85m or 32.3% of the population as of 7 May.

Number of People in Germany Received at Least One Dose of Covid Vaccine

But the other reason for not giving up entirely on the euro is the road to fiscal union suggested by the €750bn EU Recovery Fund agreed to last year where northern Europe will give both grants and loans to southern Europe.

For fiscal union implies Germany underwriting the rest of the Eurozone, which implies higher government debt levels can be sustained for that much longer given that net government debt is only 50% of GDP in Germany compared with, say, 142% in Italy.

On this point, there were reports last month that Italian Prime Minister Mario Draghi is seeking to borrow another €40bn.

Meanwhile, it is assumed for now that the next German federal government will remain in favour of the path towards fiscal union which was enabled by Angela Merkel’s support of ECB bond-buying during the Eurozone Crisis in 2012 and her support last year for the Recovery Fund.

This will almost definitely be the case if the Greens are part of the next Federal Government following September’s federal election, as is likely.

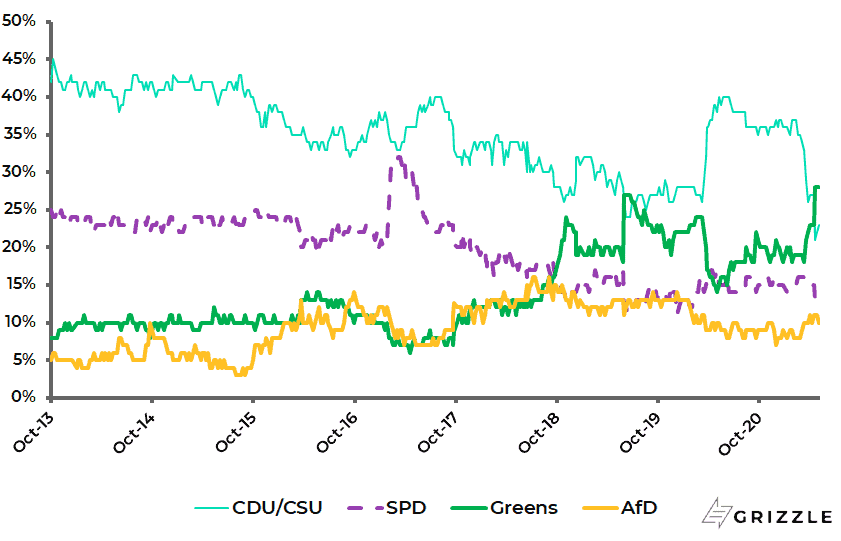

In this respect, German politics is about to become interesting again with the election marking the end of Merkel’s 16 years as Chancellor.

The Green party has a 28% support rating in the latest opinion polls ahead of the 23% support for Merkel’s CDU.

So, there is a possibility that the CDU ends up in opposition in the post-Merkel era and a coalition is formed comprising primarily the Green Party and the left of centre SPD.

Germany Opinion Polls – Political Party Support

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.