The preference here continues to favour cyclical stocks for the “back to normal” trade.

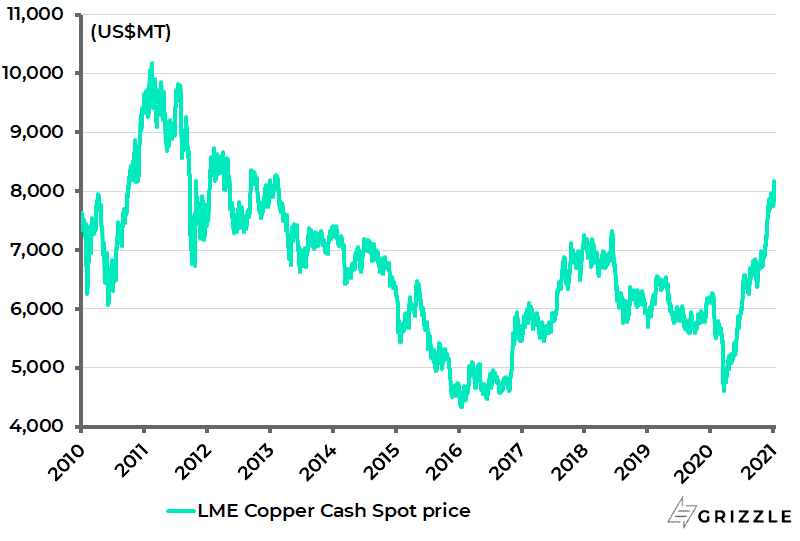

That means the likes of auto-related, industrial metal-related (witness copper’s renewed 73% surge since late March 2020), and, of course, energy stocks.

Copper Price

What about financial stocks?

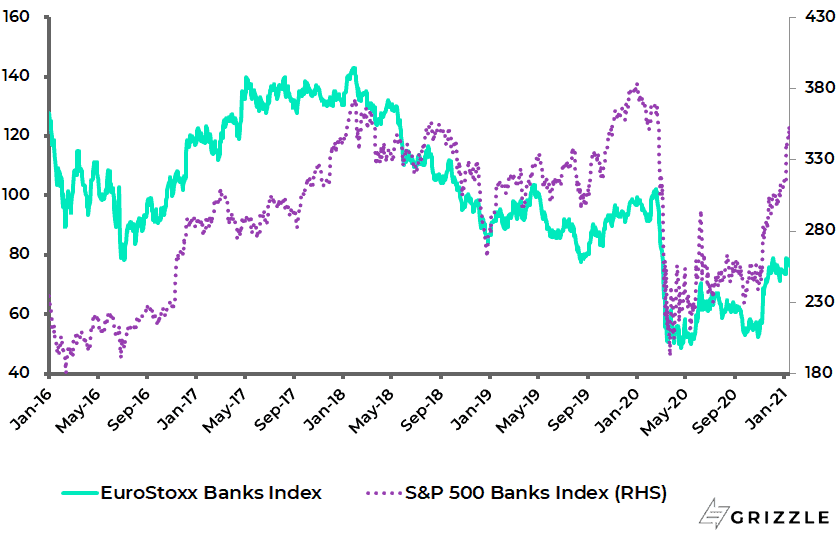

Clearly, bank stocks will participate in any cyclical rally triggered by yield curve steepening, as has happened of late.

The EuroStoxx Banks Index has, for example, risen by 46% since late October, while the S&P500 Banks Index is up 43% over the same period.

EuroStoxx Banks Index and S&P500 Banks Index

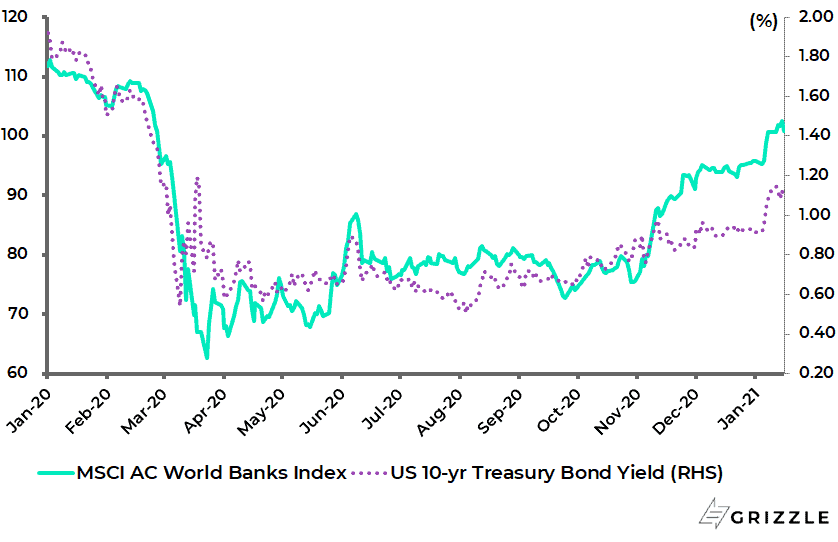

The sensitivity to long-term bond yields is shown from the fact that there has been an 88% correlation between the MSCI AC World Banks Index and the US 10-year Treasury bond yield since the start of last year.

MSCI AC World Banks Index and US 10-year Treasury Bond Yield

This is why bank stocks will be a natural beneficiary if the extreme fiscal and monetary policy response to Covid-19 in the G7 world triggers the peaking out of the nearly 40-year-long deflationary era and the return of inflation – in line with the base case previously argued here.

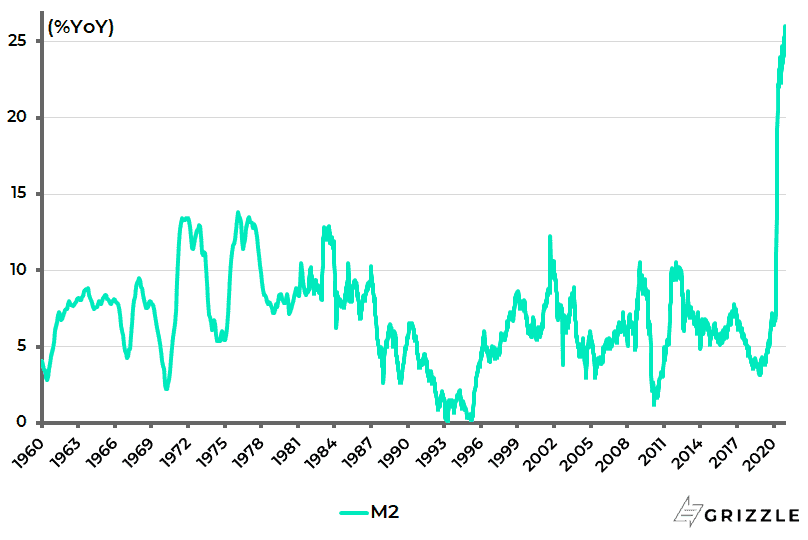

A Key Inflation Signal is Money Supply Growth

As also discussed here previously, a key signal that regime change may be afoot in the G7 world, in terms of a move from a disinflationary era to an inflationary one, has been the continuing surge in broad money supply growth in the G7 world which has in turn been driven significantly by guaranteed lending schemes.

US M2 growth has surged from 6.7% YoY in December 2019 to a record 26% YoY in mid-December 2020 and 25% YoY in early January.

US M2 Growth

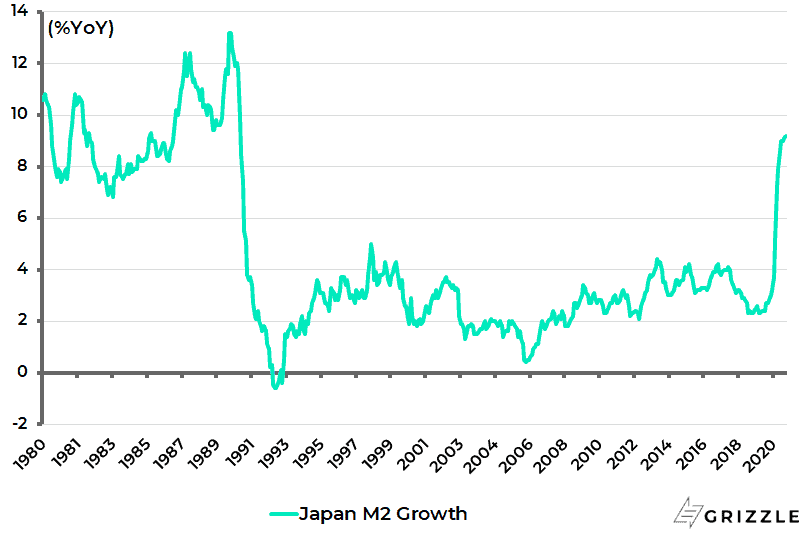

While in Japan, M2 growth rose from 2.7% YoY in December 2019 to 9.2% YoY in December 2020, the highest level since November 1990.

Japan M2 Growth

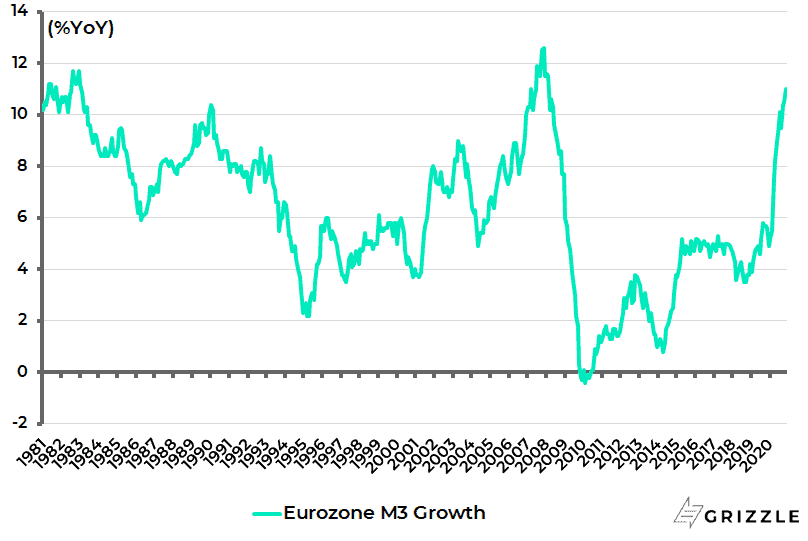

Eurozone M3 growth also rose from 4.9% YoY in December 2019 to 11% YoY in November, the highest level since February 2008.

Eurozone M3 Growth

Government Loan Guarantees Will Outlast the Pandemic

Meanwhile, investors should assume, until proven otherwise, that these loan guarantee schemes remain in place long after the pandemic has passed.

The schemes are also of macro significance since the guaranteed loan schemes in the G7 world cover a significant portion of the workforce.

What about the bank stocks themselves?

The banks probably make more money on these guaranteed lending schemes than by doing what they would normally do in an economic downturn, namely buying government bonds.

After all, they are only acting as servicing agents for the government.

The negative point, of course, is that banks become more and more instruments of the government; with the risk that bank shareholders are forced by political decisions to take the downside risk of guaranteed lending, be it by a ban on dividends or, more painfully, by forcing retrospectively on them loan losses from supposedly guaranteed lending.

Still, these are longer term questions.

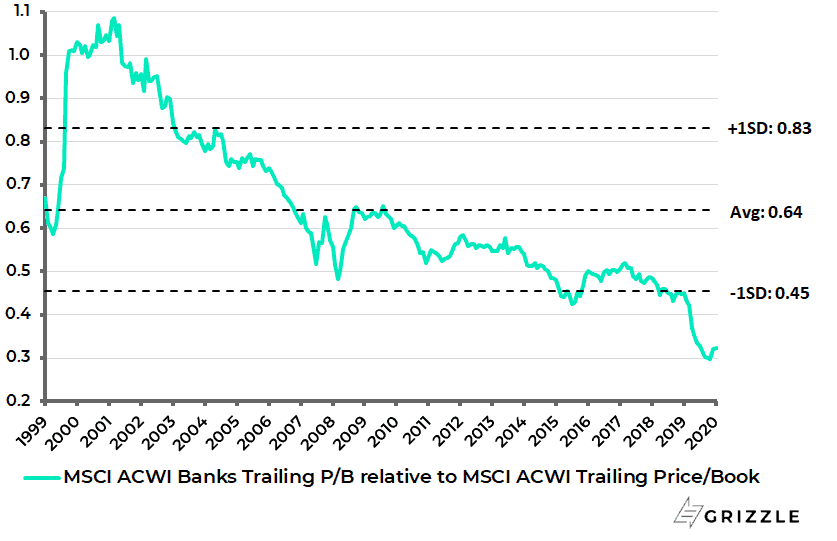

In the short term, banks can outperform on the yield curve steepening that should accompany any further post-pandemic return-to-normal trade, with there being more than 60% upside in global bank stocks for mean-reversion back to a 20-year mean relative to the MSCI AC World Index.

MSCI ACWI Banks Trailing PB Relative to MSCI AC World Trailing PB

This is why it is so important if the G7 central banks try to interrupt that natural process by pegging bond yields in line with the base case here.

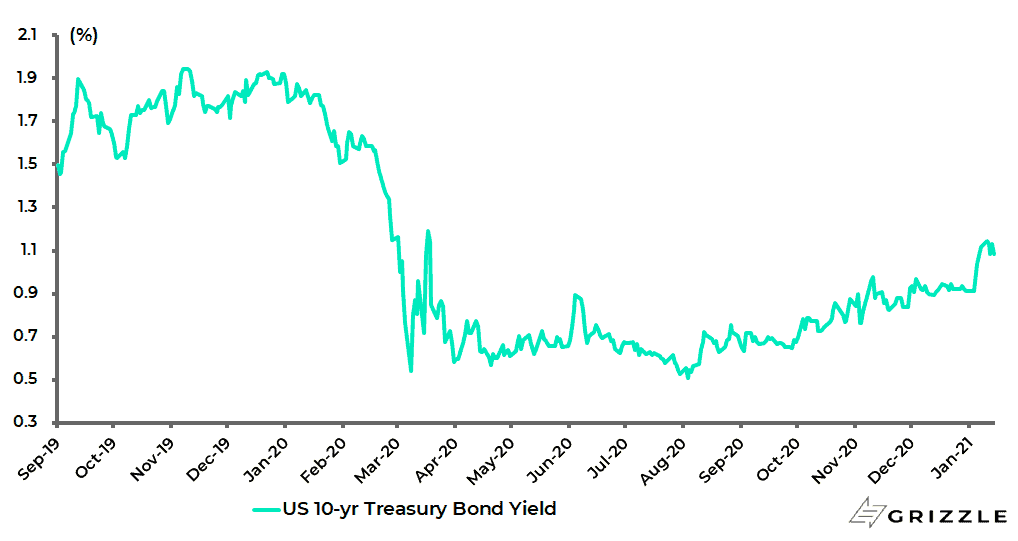

This has now become a real issue, and not just an academic one, with the recent sell-off of the Treasury bond market triggered by the Georgia Senate election result.

The US 10-year Treasury bond yield rose from 0.91% on 4 January to an intraday high of 1.19% on 12 January and is now 1.08%.

US 10-year Treasury Bond Yield

Yield Curve Control a Risk to a Bank Stock Rebound

Remember that the stated reason for pegging bond yields, if it happens, will be not to jeopardize the Fed’s 2% inflation target by allowing higher long-term interest rates to jeopardize economic recovery.

The real reason, of course, will be the understanding that the system cannot afford higher interest rates given the massive fiscal burden taken on by G7 governments in their Gadarene-swine like panicky policy response to the pandemic.

Interestingly, there was recently an implicit acknowledgment of this reality from a former central bank chief who is now in the private sector.

Philipp Hildebrand, Vice Chairman of BlackRock and a former head of the Swiss Central Bank, noted in a speech in Vienna late last year that, with public debt soaring to record high levels during the pandemic, “the decision to start with the tightening of monetary conditions will be more politicised”, with new central bank regimes trying to produce “overshooting” inflation scenarios.

This writer also agrees with a statement attributed to Hildebrand, who is the Swiss candidate to become the Secretary-General of the OECD, that he did not share the widely-held view that “inflation is dead”.

Remember, in financial markets, what everybody knows is seldom worth knowing.

Meanwhile, in a theoretical world where G7 central banks allow interest rates to normalise along the yield curve, and there is no yield curve control, bank stocks would still look very attractive.

That is until their business models are disrupted by the mass adoption of cryptocurrencies and blockchain technologies. But that existential crisis is probably still ten years away.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.