On Thursday Intuit (NASDAQ: INTU) announced earnings which comfortably beat Wall Street estimates, though some analysts expressed disappointment with the company’s third-quarter guidance. Intuit provides payroll and accounting solutions including TurboTax, QuickBooks, and Mint.

Intuit’s Earnings Showed a Strong 2018 Performance

The company announced earnings per share of $1 on sales of $1.5 billion, ahead of the street’s estimate of $0.86 on revenue of $1.47 billion. The stock price which closed at $235.03, initially dipped $1.53 in after-hours trade, before rising to close just $0.08 off the normal session close.

Intuit’s mid-market products showed strong growth and impressive online subscription growth. The small business and self-employed segment reported revenue of $833 million, up 17% over the previous quarter.

The consumer segment reported revenue of $461 million, while the strategic partner segment’s revenue lagged, coming in below estimates at $208 million. The strategic partner segment is only expected to grow 2 to 4% for the year but represents a relatively small segment.

QuickBooks managed to grow online subscribers 7.7% from the previous quarter to 3.88 million, which represents a very strong annual growth of 38%.

The company is estimating third-quarter revenue growth of 10 to 12%, which is in line with revenue growth over the last 12 months, but down substantially from the previous year. Third quarter earnings are expected to be between $5.35 and $5.40 which is broadly in line with the consensus estimate of $5.38. The earnings and revenue guidance ranges for the full year (2019) were both marginally below consensus.

Intuit’s Stock Price Indicates Company Looking Fully Valued

While the results and forward guidance are solid, the full year earnings guidance range puts the stock on a forward PE of over 36, with earnings growth of 14%, which now appears to be slowing. This could suggest a fully-valued stock.

Wall Street’s analysts have price targets ranging between $200 and $250 and averaging $234. This set of results is unlikely to see those targets being raised in the immediate future, in which case upside would be limited.

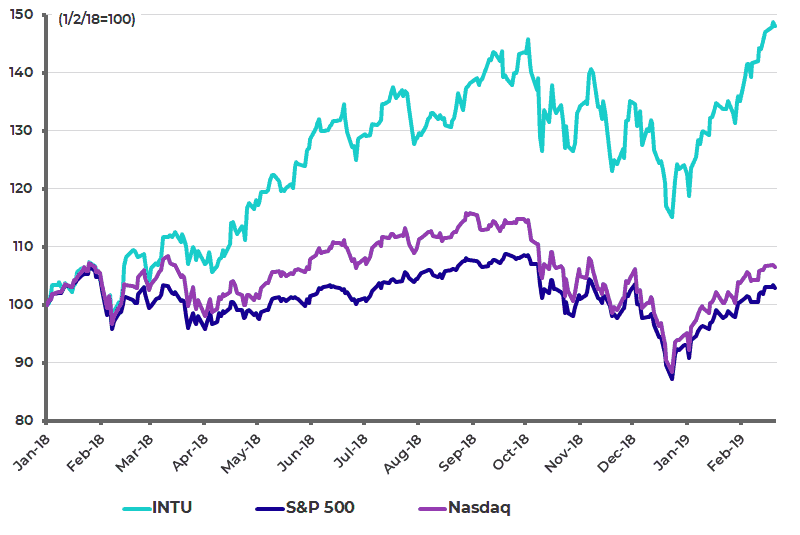

The share price has rallied 28.5% since the market’s December low, well ahead of the Nasdaq’s 19.25% and the S&P500’s 18%. It has also gained 48% since the beginning of 2018, well ahead of the benchmark indices.

Intuit Performance to Indexes

The question is whether or not the market was expecting more optimistic guidance for the third quarter? The stock has seen increased buying volume since late January, so in the short-term profit taking is likely.

While the short-term outlook may be depressed, the longer-term picture remains positive. The company is growing market share and its customer base among small businesses like Intuit’s products. The strong subscriber growth shown by the Online Ecosystem proves that the company is succeeding in its core area of focus. Margins are also showing modest but steady growth, and revenues should be relatively resilient to a downturn in the economy.

Longer-term investors like the stock and may well be looking for weakness as a buying opportunity. For this reason, any weakness in the stock price may be short-lived.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.