https://youtu.be/c3sR8giMPZs

Slack (NYSE: WORK) is a company that is truly revolutionizing the way office workers and students communicate.

The market rarely sees a piece of software that basically sells itself and this quality makes Slack a compelling company.

In the infographic below we lay out why Slack offers 3 times upside and will be an $80 stock by 2026.

How Slack’s Direct Listing is Different from an IPO

Slack is one of the very few companies hitting the stock market through a direct listing process instead of the more common initial public offering (IPO).

A direct listing differs from an IPO in a few important ways.

Slack Isn’t Raising Money Through the Direct Listing

A direct listing, unlike an IPO, doesn’t include the sale of new shares to the public to raise money. This is a positive sign to investors as Slack is signaling it isn’t desperate for cash.

As of March, we estimate Slack has over $800 million of cash which should last the company 8 years or more at the current annual burn rate.

This is a solid runway to turn a profit, compared to Uber and Lyft who have only 3-5 years of cash left even though they raised billions from the sale of IPO shares. Slack won’t have to issue new shares anytime soon unless the company decides to make a big acquisition of another competitor.

More Uncertainty Around the Right Price for the Stock

In a typical IPO, bankers and management travel all around the country talking to investors. These conversations help the banks get a handle on what the demand for the stock looks like and where they should price the first shares sold to the public. This “roadshow” as they call it plays a big part in setting expectations for the stock.

In a direct listing, bankers speak with fewer investors, creating more uncertainty around stock pricing and the sentiment of investors towards the company. This uncertainty can create more volatility in the first few days of trading as the true market price is figured out.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]From an investors point of view, the early price chatter you read about in traditional financial media is less representative of where the stock will actually trade on day 1 compared to an already volatile IPO. [/su_panel]There is also no market support from banks in a direct listing. Slack is not selling shares to underwriters (i.e. Goldman Sachs, Morgan Stanley, etc) that can then be used to support the stock if it falls on the first day of trading. This lack of support could mean the stock will go up or down in early trading even more than a typical IPO.

A Direct Listing is Supposed to be Cheaper than an IPO

The largest benefit of a direct listing is the lower costs. Direct listings require only one or two banks to help with the details instead of up to 30 in a typical IPO. In an IPO there are more banks helping to maintain a liquid market in the shares, buying and selling shares in the open market.

Uber, for example, had 30 banks on their IPO, while Slack is only using 10 banks in its direct listing. Surprisingly though, it doesn’t look like Slack is saving any money. Slack is paying ~$27 million to the 10 banks, 0.17% of its potential market cap, which is the same fee rate Uber paid for it’s IPO. We wonder why Slack is going the direct listing route if it won’t be saving any money?

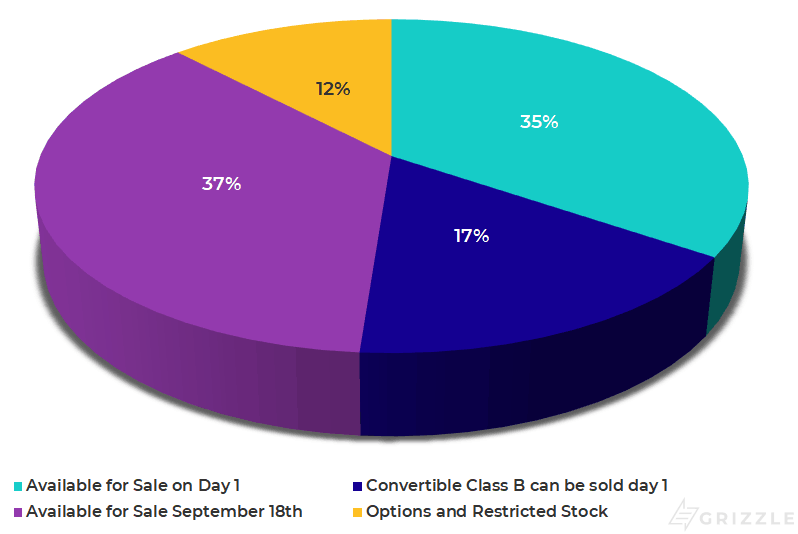

There is No Share Lockup for Current Stockholders

This is absolutely the most important difference between a direct listing and an IPO. In an IPO only a small portion of available shares are sold to the general public, usually 10-15%, while the rest are held by insiders, employees, venture capital firms, top management, and founders. These insiders are typically restricted from selling any of their shares for at least 6 months from the date the company goes public.

Share restrictions often create artificial scarcity of the stock as there is more demand than the small number of unlocked shares can satisfy. This is positive for the stock price and can explain why IPO shares sometimes spike 50% or more on the first day of trading.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]In a direct listing, every person who owns a share of stock can sell it the moment the stock begins trading. All else equal, this is negative for the price of the stock with more sellers than in an IPO. In Slack’s case, 52% of shares can be sold on day 1, compared to 15% in most IPO’s. Slack said in a recent filing that it will definitely sell at least 5% of shares owned by the company just to cover taxes from the listing. [/su_panel]Slack Share Sale Restrictions

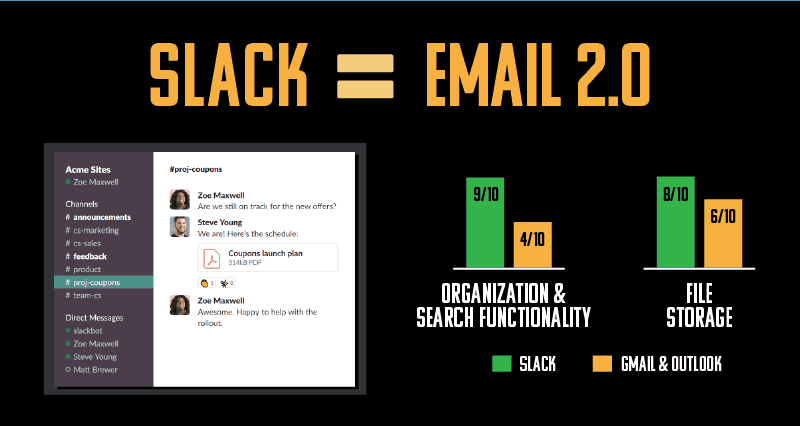

Slack is Truly Email 2.0

Technology pundits often state that even Slack management has trouble defining what Slack is.

In reality, we think Slack’s offering is powerful and simple to understand. Slack is the first evolution of email since it was invented in 1971.

If you work or communicate with a group, Slack is the new, more efficient way to share information.

In Slack, messages are grouped by topic, called a channel, compared to an email inbox which is just a stream of conversations. Google, for example, groups email chains by the subject line, so if you are having a conversation that spills over into email chains with a different subject it will be hard to keep track of the whole conversation. This channel grouping drastically streamlines communication and makes it easy to manage projects with multiple people.

Slack operates like a text chain where it is easy to scroll from the beginning to the end of the conversation to catch up or refresh your memory on what was said. Group members can attach files within the conversation and these files are easily visible in the order they were attached and always available for download. This is a huge improvement over email where attachments are shoved at the bottom of an email or not included at all if the sender of a reply or forward forgets to manually include the attachment.

Probably the biggest time saver when using Slack is the search feature. Users can search for any term or file name throughout all topics in their Slack workspace and from our experience, the search functionality is far superior to Gmail or Outlook. We have been unable to find important emails with Gmail in the past and it leads to lost time and duplicated conversations and work.

We have just scratched the surface when it comes to Slack’s improved functionality. If you understand nothing else about Slack just know it saves teams time and employers money.

Slack Sells Itself with Technology and Pricing

The power of Slack comes from the product itself and the pricing.

The sales strategy that management has in place demonstrates they truly understand it only takes a few hours with Slack before a group of users is hooked.

Slack can be downloaded for free with most of its functionality intact, removing any barriers that would keep interested future customers from sampling the product.

Word of mouth has been one of the most powerful sales tools for Slack, with employees who use Slack becoming unintentional Slack ambassadors when they move to a new employer and tell them about the productivity benefits of the platform. Grizzle switched all of our internal communications to Slack three months ago and we are achieving a very real productivity boost versus business as usual. We are believers in the positive impact Slack can have on an organization.

Speaking about international expansion efforts, Slack is in the early days. The company only has a sales footprint in six countries outside of the U.S., but has plans to ramp up sales teams internationally and build offices in more countries, generating better growth outside North America.

We already know this is a product that increases in value the more you use it and we believe the increased visibility as a public company and sales team expansion will both contribute to better adoption of Slack’s free and paid tiers.

Slack’s Pricing is Cheap

The top tier pricing of Slack at $12.50 per month per user is cheap compared to the potential labour costs savings for businesses who integrate the technology into daily communications.

For example, an employee paid the U.S. median wage of $32,000 a year would only need to work 0.5% faster for Slack to pay for itself. Put another way, a 40 hour a week employee would need to save only 10 minutes a week with Slack for the employer to justify the $12.50 monthly payment.

Ten minutes of efficiency is not much when you consider many email clients automatically fetch email only once to twice an hour compared to Slack messages which are instantaneous. This 30-60 minute difference alone would make Slack a high return investment for any small to medium-sized business.

The efficiency potential of Slack for team projects coupled with the low price of the service makes Slack an easy sell to any IT manager. As the sales team demonstrates the power of Slack to more and more IT managers, we expect to see accelerating adoption among global corporations and higher learning institutions.

Wall Street Analyst Target Prices Will be Irrelevant for Slack

Grizzle has been very vocal about the view that Wall Street target prices for high growth stocks are generally completely irrelevant.

Wall Street sell-side analysts have a very dismal track record calling the long-term upside of growth stocks, frankly they are challenged accurately predicting share prices for all stocks in general.

There is an anti-risk taking culture on Wall Street, analysts aren’t compensated on how ‘right’ their forecasts are — therefore analysts set target prices that are very ‘reasonable’ — usually in the range of +/- 20% of the current share price. This optimizes their career longevity, why take a risk when you don’t have to.

Put bluntly, analyst target prices generally always follow the movement of the share price. The market dictates what analysts will forecast and write about.

Career risk explains why a stock that goes from $20/sh to $200/sh likely had dozens of share price targets and neutral or underweight ratings on the way there. Investors who followed these target prices would have sold at $25 then $35, then $100 as the stock blew through analysts short-sighted target prices, missing much of the long term upside on the march to $200/sh.

To help us avoid near term thinking, Grizzle uses an Internal Rate of Return (IRR) approach to trade any stock. The process has three steps:

- Figure out what the stock is worth longer term (5-10 years away) using fundamental analysis

- Calculate the annual rate of return from now until then.

- Establish a minimum and maximum IRR and buy or sell the stock depending on if the IRR hits your min or max on its way to the target price.

The next section will explain this strategy in more detail.

Slack (NYSE: WORK) is Worth $80/sh by 2026

We think it is reasonable to expect 10% of the global pool of office workers and students will be using Slack by 2026. Currently 1% use Slack so this would be a 10x increase in a little over seven years, but would still be only 7% of the people who use Microsoft Office worldwide.

50% of Slack users already live outside of North America and the company hasn’t ramped up international sales teams yet which could easily energize international user growth and revenue.

Revenue is expected to hit ~$600 million in 2019 so Slack is just scratching the surface of a potential user base worth at least $35 billion. We expect revenue to grow to $8 billion by 2026 mostly driven by continued user growth. $8 billion is only 1% of the total value of global IT budgets for enterprise software by 2026 according to a recent Gartner study. If Slack is able to convert free users to a paid plan faster than we are expecting, revenue could beat our estimates.

Slack Market Opportunity Worth $36 Billion

| People in millions | U.S. | Euro | ROW ex-CHINA | Total |

| Civilian Labour Force | 157 | 235 | 2,288 | 2,680 |

| Office Jobs | 97 | 118 | 229 | 443 |

| Students 15-24 | 43 | 35 | 418 | 496 |

| Revenue Potential (Bn) | 11 | 13 | 12 | 36 |

| Rev/User/ Month | $6.50 | $7.25 | $1.53 | $3.19 |

Source: Bureau of Labor Statistics, Gartner, Grizzle Estimates, https://ec.europa.eu/eurostat/web/lfs/data/database, https://fred.stlouisfed.org/series/LFWA24TTEUQ647N,

How to Trade Slack From Now to 2026

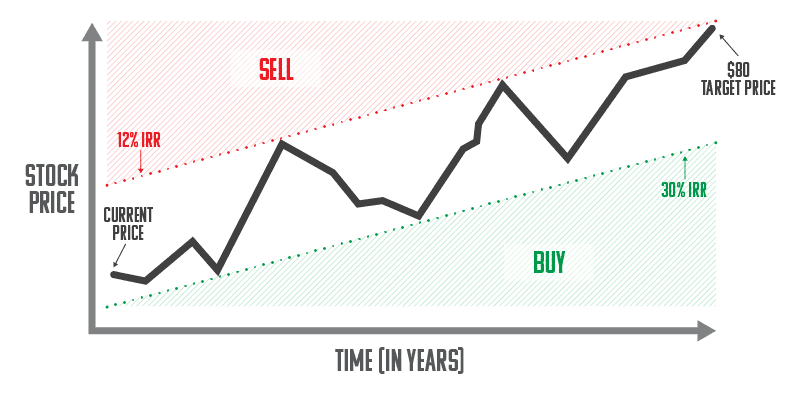

Our target price of $80/sh offers an internal rate of return (IRR) of 18%. This means on average the stock should increase 18% in any given year. However, we know stocks go up and stocks go down, so we use an IRR band to decide if the stock has run too hard or if it is trading at a bargain.

The way an IRR band works is as the stock price moves closer to our target, the rate of return falls. There is less return between the current price and the target. As the stock falls the opposite happens and the potential return increases. The stock price is farther from the target price.

In the case of Slack, we think a 12% IRR is the minimum return needed to compensate for the risks of owning a high growth but unproven tech stock.

On the other side, if Slack were to trade down to where the IRR increased to 30% we would be buyers of the stock all day. Looking at the stock price with an IRR lens helps us escape the inflexibility of target prices and keep focused on the long term potential.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]The graphic below explains how to judge if Slack stock is overvalued or undervalued from now until 2026. Using 2019 as an example if Slack goes above $44-$46/sh, we would sell it and wait for a better entry point. If the stock falls to $13/sh or below we would be buying shares hand over fist as the risk-return would be very favourable. [/su_panel]Grizzle’s Preferred Way to Set a Price Target

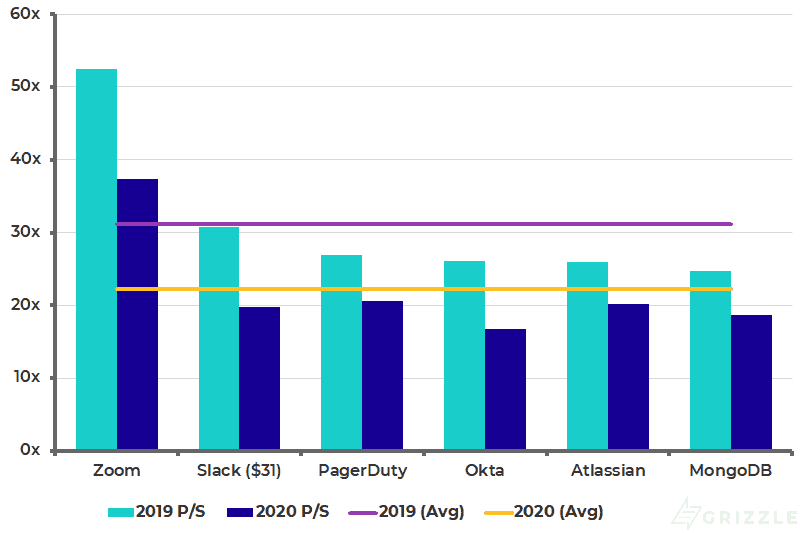

Looking at Slack’s private valuation compared to similar enterprise software peers, the company is fairly priced. However, this chart uses $31/sh, the highest price a share of Slack has gone for privately. If the stock debuts strongly on public markets it will likely trade at a premium to all peers except Zoom.

Relative value is only useful to help you judge if the stock has gone too high too fast, not if it is good long term investment. Given that animal spirits, aka risk appetite, is high and investors are hungry for big gains, if the stock trades through $46/sh in 2019, we would be sellers as the long term value is no longer there, offering less than an 8% rate of return, far too low for a young, money-losing business.

Slack’s Multiple at $31 is in Line with Peers

How to Play Slack on the First Day of Trading

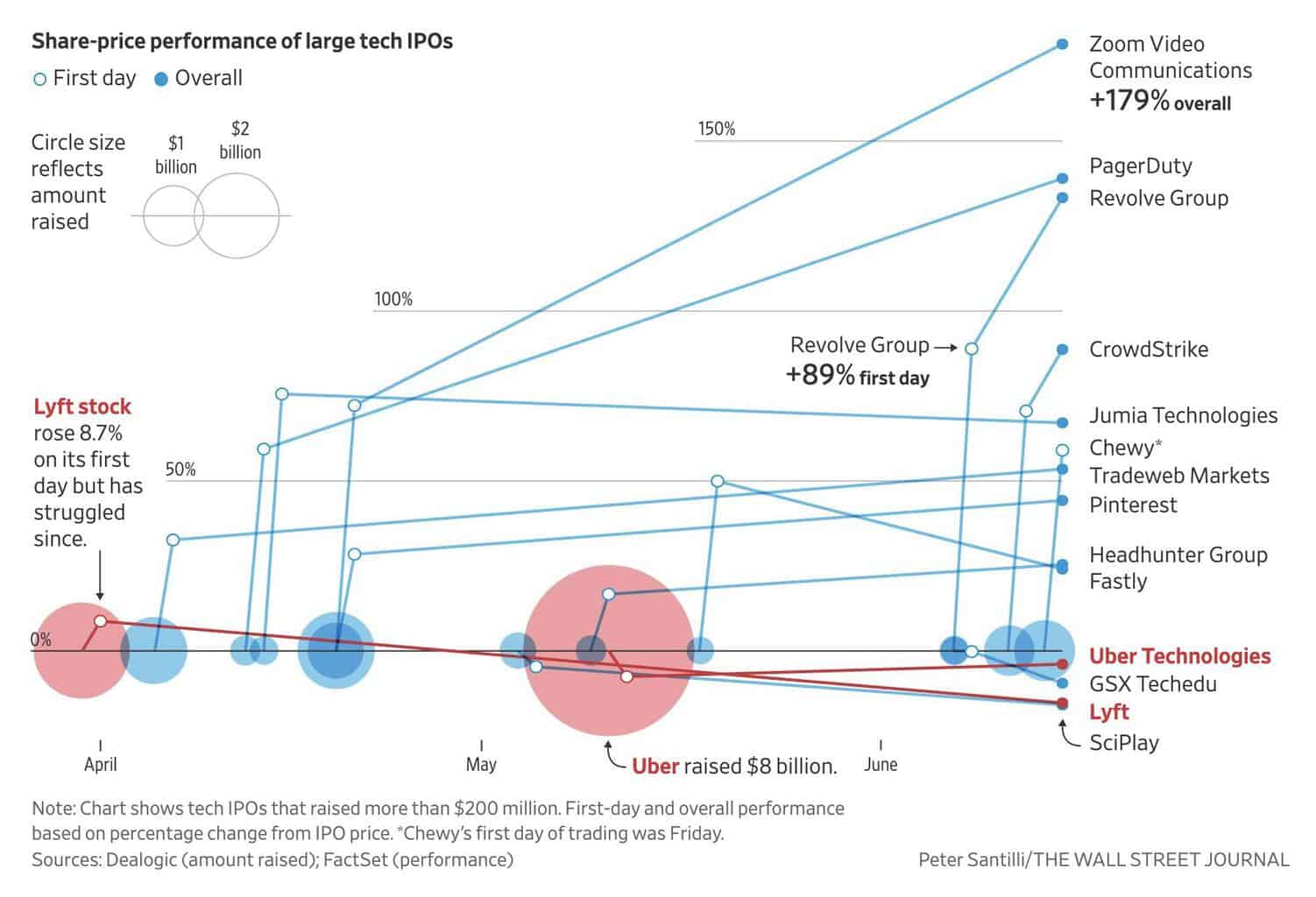

Grizzle has closely followed all the major IPOs in 2019 and we’ve noticed one technical trend that consistently generates positive returns for investors.

On the day of the IPO if a stock ends the day higher than the first trade of the day, in most cases it will continue to go up. The only true exception has been Lyft, which kicked off the 2019 IPO boom and priced the stock too high out of the gate.

Grizzle’s “Animal Spirits” Gauge is Red Hot

Slack is a Silicon Valley darling and is also well known by the general public, making us think the stock will perform well on the day it goes public. Investor’s risk appetite commonly referred to as ‘Animal Spirits’, is running hot right now judging by the performance of the two most recent IPOs. Chewy and Fiverr increased more than 50% on the first day of trading showing investors are hungry for growth regardless of risk.

Another indicator of strong demand is the big increase in the private value of Slack this year. Slack traded privately for $12 in September but rocketed to $21 in January and peaked at $31 in May.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Most importantly 51% of shares are free to be sold on day 1, compared to at most 15% in a typical IPO. With this much potential selling pressure, if Slack ends the first day of trading higher than where it started we know there is serious investor demand for the stock and future performance should be solid. If the stock goes down on day 1, we would be buyers anywhere below $20/sh.[/su_panel]

Who Owns Slack Stock and at What Price

Understanding who the holders of Slack stock are and what their potential motivations may be is critical when figuring out the right time to buy or sell.

To start let’s look at the history of capital raises. Slack did 15 financing rounds prior to the IPO at prices between $0.09 and $11.91.

Since the last official raise in August of 2018, the stock price has spiked in private trades among investors leading up to the direct. Some shares sold for $31/sh in May of 2019 and this will likely serve as the market’s anchor price when they figure out what the stock is worth on day 1 of trading.

History of the Stock Price

On average, pre-IPO shareholders have a cost basis of $3.73 compared to the expected initial trading price between $26.00-$31.00/sh. They are sitting on big gains and some of the employees will be looking to lock in these gains on day 1.

| Funding Round | Shares | Share Price |

| Series A | 84,751,000 | $0.09 |

| Series B | 43,320,000 | $0.25 |

| Series C | 64,805,000 | $0.66 |

| Series D | 42,490,000 | $2.55 |

| Series D-1 | 1,235,000 | $2.07 |

| Series E | 22,602,000 | $5.97 |

| Series E-1 | 6,047,000 | $6.27 |

| Series F | 19,866,694 | $7.80 |

| Series F-1 | 6,793,130 | $7.80 |

| Series G | 24,717,887 | $9.31 |

| Series G-1 | 2,149,382 | $9.31 |

| Series G-2 | 17,241,379 | $8.70 |

| Series G-3 | 1,464,680 | $8.70 |

| Series H | 33,469,795 | $11.91 |

| Series H-1 | 2,418,922 | $11.91 |

| Total Shares | 373,371,869 | $3.73 |

Source: Slack S-1/A

Slack is a Legit Technology Contender for your Portfolio

Slack is one of the few ‘IPOs’ this year selling a truly killer app. The product is cheap, drives positive results and doesn’t require much use before the benefits of the technology are apparent.

So far Slack is just scratching the surface of a collaboration market worth at least $35 billion. Slack is also fighting for a piece of the $400 billion spent every year on enterprise software, telling us the market opportunity could be even bigger than we are expecting.

Slack’s only real competitor is the Microsoft Teams app and so far this offering from Big M is an afterthought, bundled and overshadowed by Outlook, Word, Powerpoint, and Excel as part of the Office 365 offering.

As an investor, it’s rare to find a company with great fundamentals that is also selling a product you personally use and love. Our in-depth knowledge of the product and the potential size of the market give us the conviction to say Slack is shaping up to be both a great stock and a great company.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.