If sentiment towards Chinese stocks remains super depressed, the same also applies to domestic Hong Kong stocks.

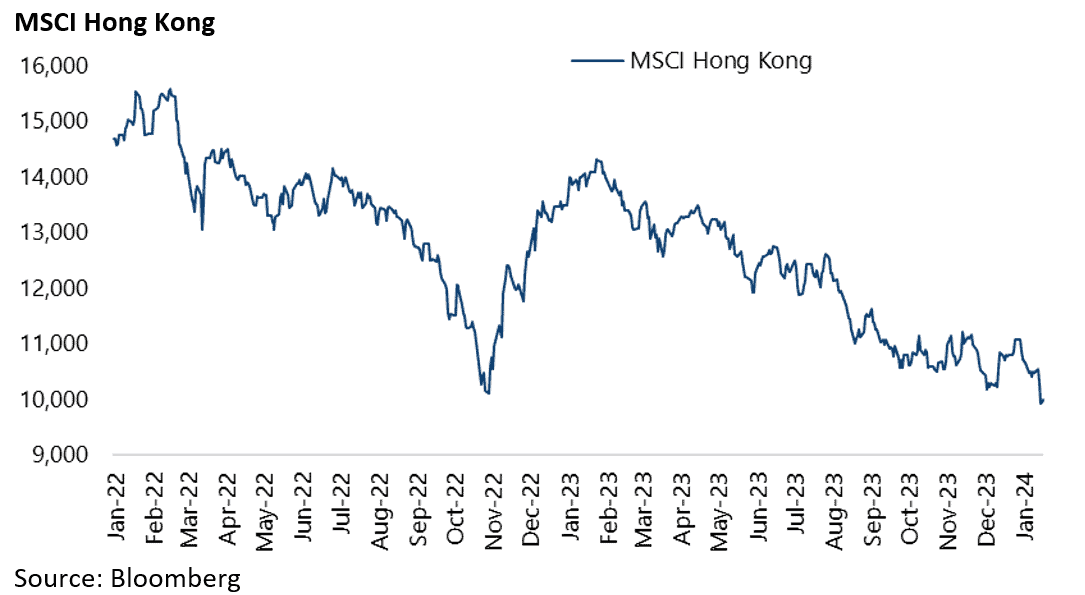

It remains incredible that Hong Kong-focused stocks are trading at levels lower than where they were before the economy re-opened post-Covid.

Indeed the MSCI Hong Kong is now below its pandemic low reached at the end of October 2022.

One reason for this is that re-opening has served as a catalyst for locals to do their weekend shopping and recreation in much cheaper Shenzhen across the border.

It has been estimated that this could be reducing Hong Kong retail sales by around 4% on a monthly basis.

The other problem for Hong Kong is that global investors are undoubtedly treating Hong Kong as part of China.

While this is in one sense true, in another sense it is not in that Hong Kong is in many respects still very different from mainland China if only because it still has an open capital account.

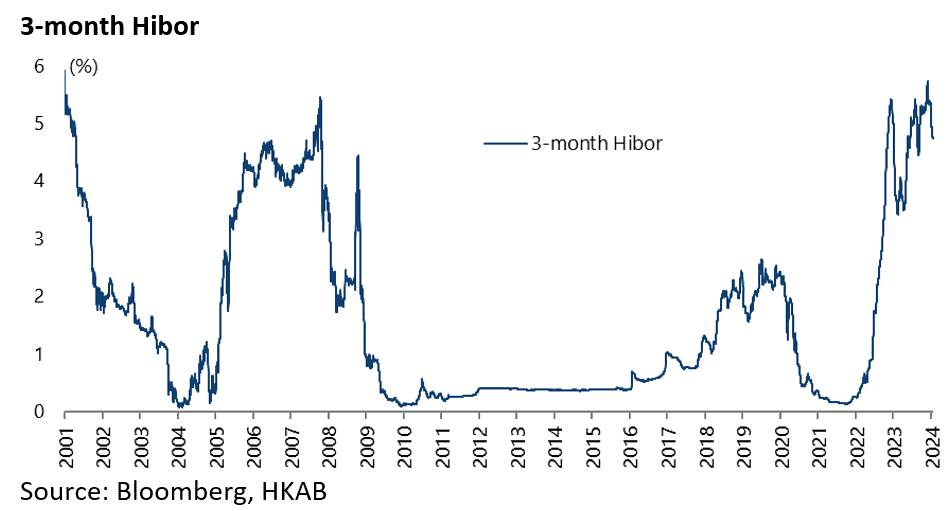

The other point, unlike mainland China, is that the Hong Kong dollar is still pegged to the US dollar and therefore will be acutely sensitive to the kind of Fed easing this year currently being anticipated by US money markets whereas stocks geared to mainland China, be they quoted in Shanghai, Hong Kong or New York, will be much less sensitive.

On this point, the negative action in MSCI Hong Kong stocks, down 9.8% year to date following a 17.8% decline in 2023, also reflects the pain from higher interest rates with three-month Hibor currently at 4.76%, though down from a recent peak of 5.73% reached in late November, which was the highest level since January 2001.

The extent of prevailing negative sentiment was best reflected in the failure of Hong Kong developer stocks to rally at all when Chief Executive John Lee announced a cut in foreign buyers’ stamp duty from 30% to 15% in his annual policy address in October.

Rather the prevailing sentiment is that, sooner or later, the government will be forced to remove the stamp duty completely so why bother buying now.

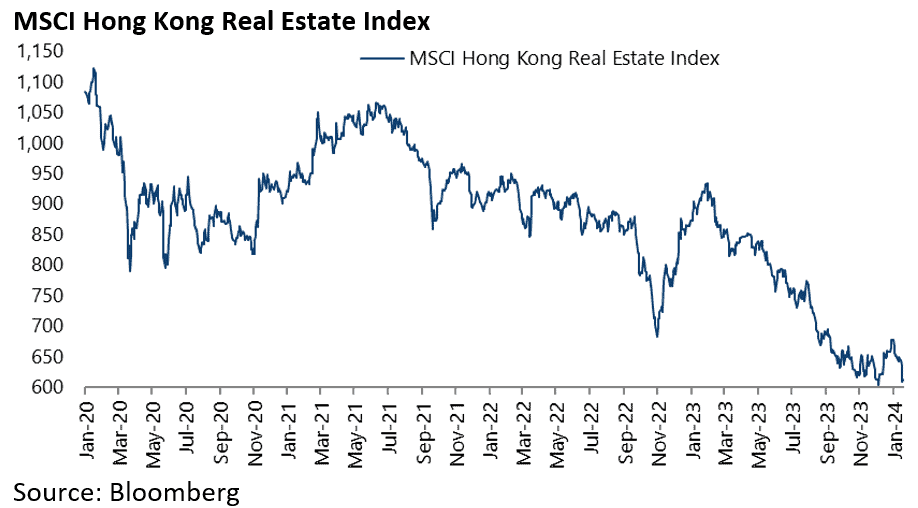

The MSCI Hong Kong Real Estate Index is now down 34% from the recent high reached in late January 2023.

Hong Kong Housing Stimulus Could Come Any Day

This seems a growing possibility, with the most likely timing around the budget which is due to be announced on 28 February.

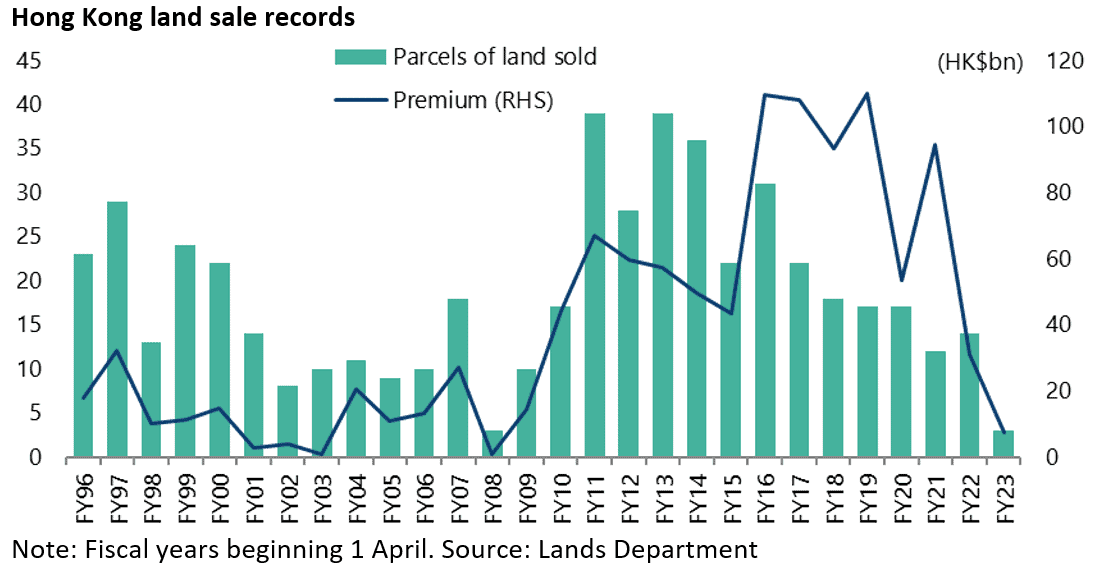

The reason for the government to remove the final anti-speculation measures is the collapse in land sales revenue which is running way below budget.

Land premium traditionally account for up to 30% of government revenue.

The Hong Kong government has so far sold only three parcels of land for HK$7.27bn this fiscal year beginning 1 April 2023 and has rejected bids on another two of the 18 slated for sale this fiscal year.

While another HK$5bn had been generated through other land premium income in the first half of this fiscal year ended 30 September, including income from lease modifications and land exchanges.

As a result, land premium income has totaled only HK$12bn so far this fiscal year or 14% of the annual target of HK$85bn.

The result is that Financial Secretary Paul Chan warned in late October that the government deficit this fiscal year could exceed HK$100bn, nearly double the original budget estimate of HK$54.4bn.

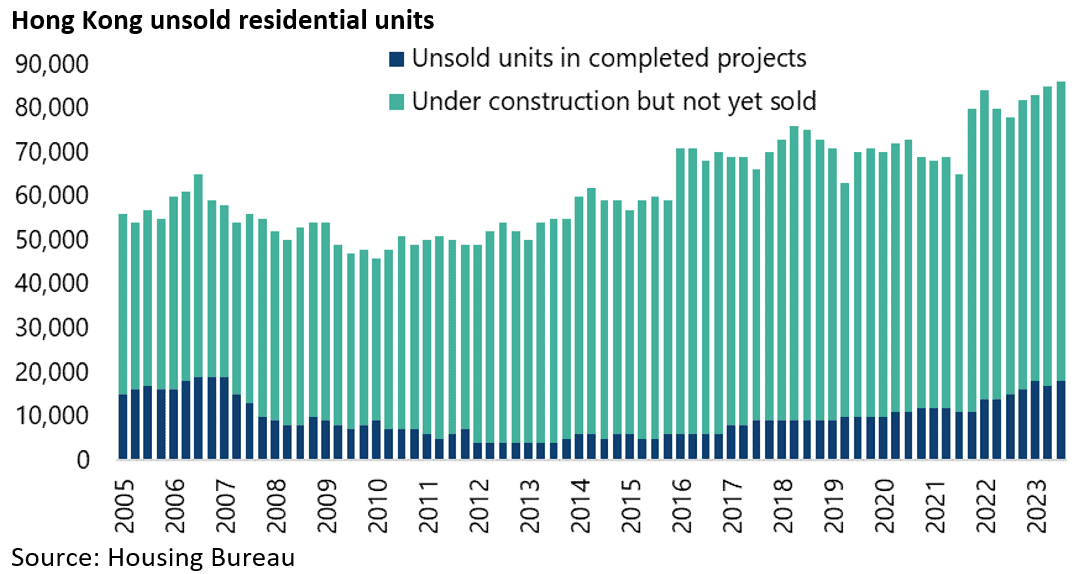

With 18,000 unsold residential units in completed projects, and another 68,000 units under construction but not yet sold, there is a near-term excess supply issue.

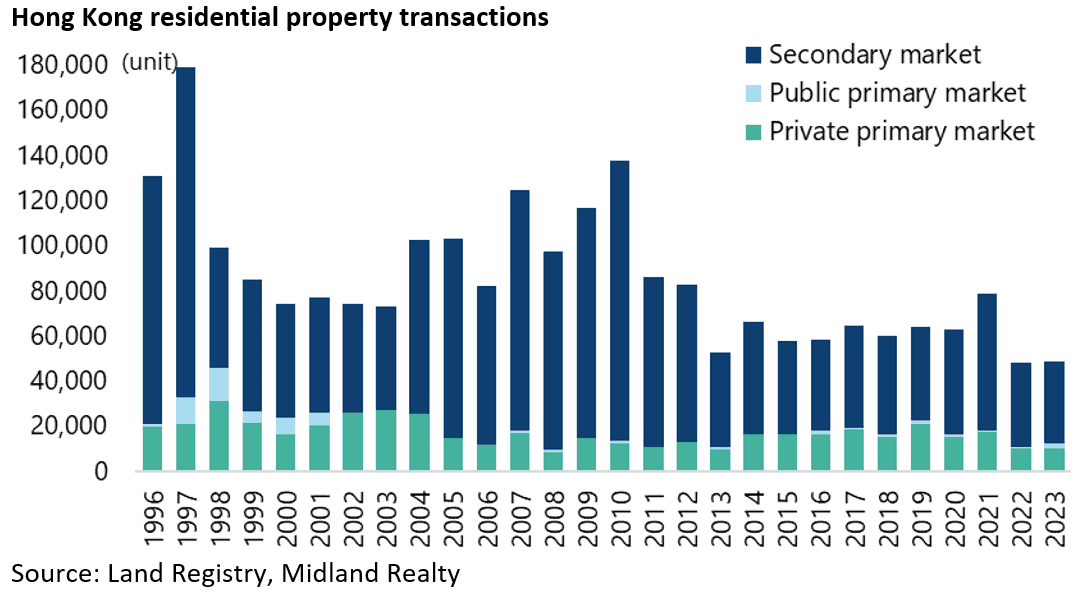

Hong Kong Housing and Stock Market Activity Remain Close to Multi-Decade Lows

For now the extent of negative sentiment is reflected in residential property transactions running at a near record low of 48,764 units last year following a record low of 48,161 in 2022.

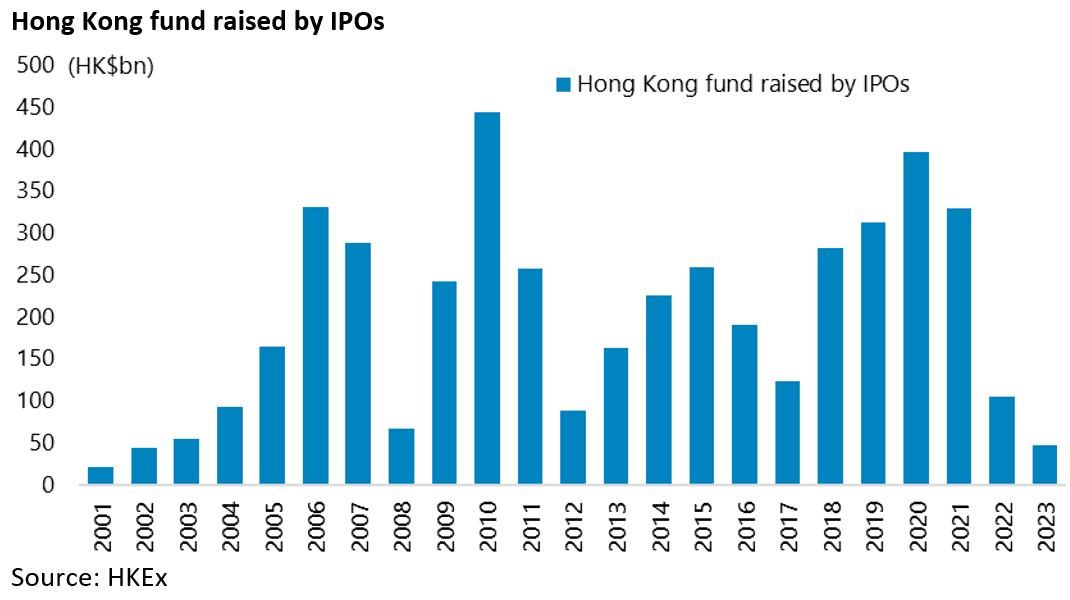

Similarly, Hong Kong IPOs were at a 21-year low in 2023. Funds raised by IPOs declined by 56% YoY to a 21-year low of HK$46.3bn in 2023.

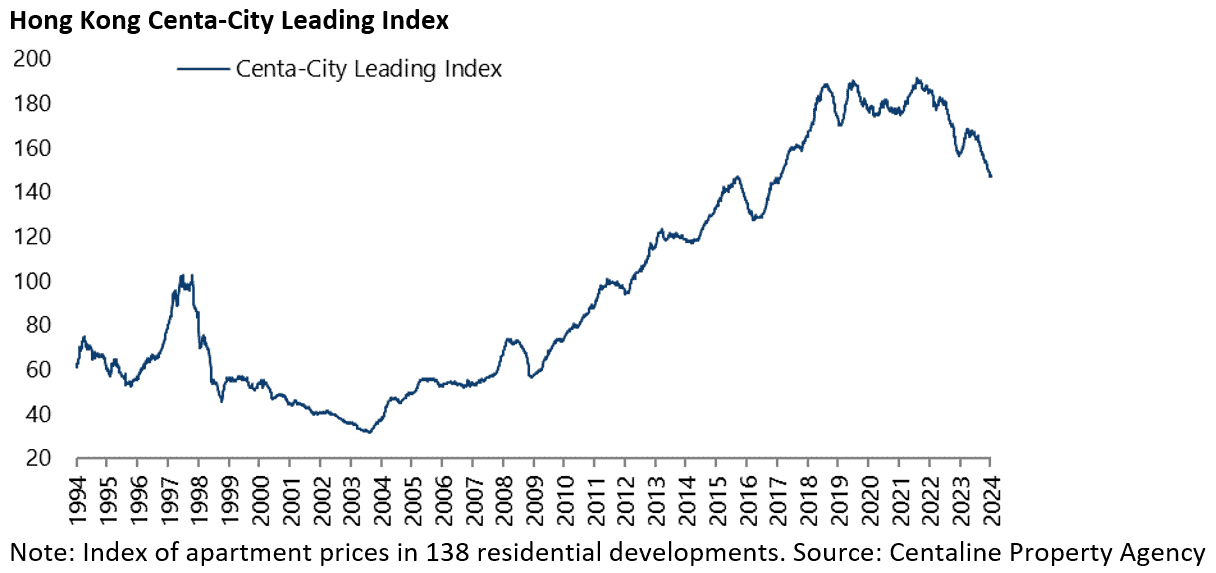

Meanwhile, residential property prices are now down 23.3% from the peak level reached in August 2021.

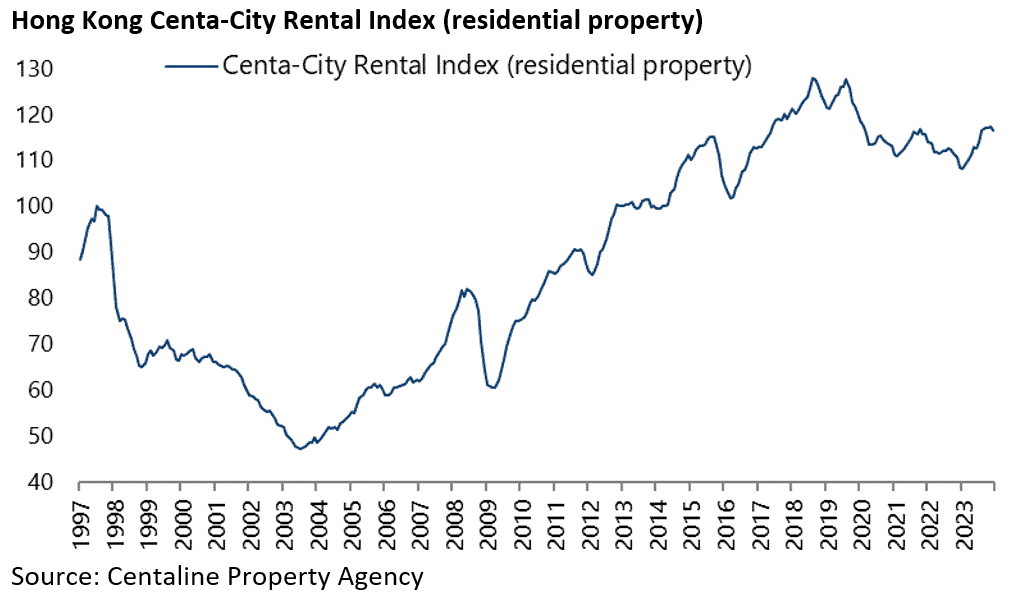

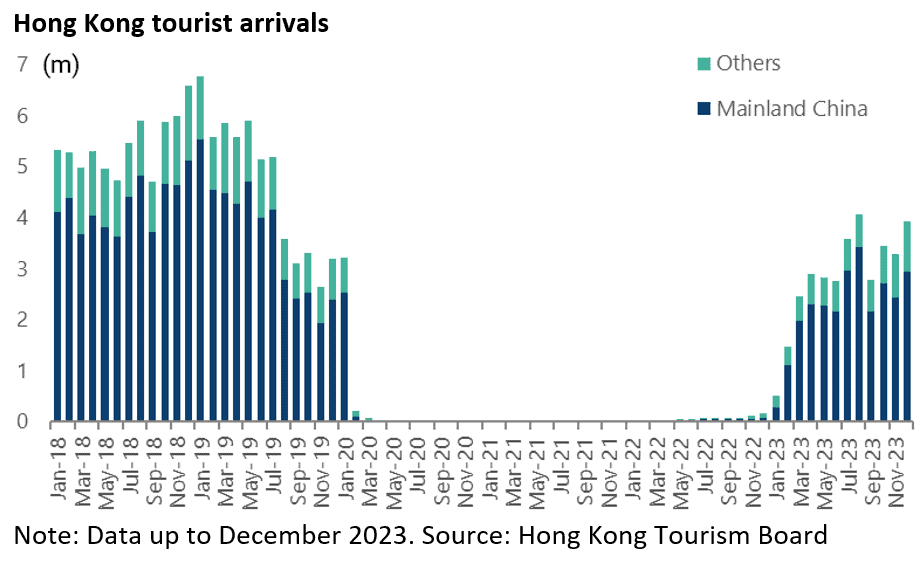

Amidst all the negatives, the one positive is that residential rents were up 7.4% last year due to increased arrivals from the mainland

Mainland visitor arrivals rose from 280,525 in January 2023 to 3.4m in August and 2.9m in December.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.