As the world attempts to transition away from single-use plastics, Danimer is one of the few company’s offering an alternative.

In recent years, plastic has become a dirty word and now could even become a banned material.

For those of you who missed it, late last year Canada unveiled a long list of single-use plastic products (e.g. straws, grocery bags, etc.) to be banned by the end of the year.

Europe has already followed suit, planning to ban single-use plastic by the end of 2021 as well.

Even with the coming ban, crude oil-based plastics are literally everywhere. Over 800 billion pounds of plastic is produced annually! and 640 billion pounds end up in landfills.

Plastic is big business to the detriment of the planet, but a company called Danimer Scientific (NYSE:DNMR) is going to change that.

Danimer offers a biodegradable alternative to the plastic bags, straws and boxes we throw away every day.

As the world attempts to transition away from single-use plastics, Danimer is one of the few company’s offering an alternative.

Danimer produces Polyhydroxyalkanoates (PHA), a polyester produced in nature through the fermentation of vegetable oils which is then extracted for the production of bioplastics (a type of biopolymer).

In simpler terms, Danimer’s core product, Nodax® PHA, is a 100% biodegradable polymer which can be used as a traditional plastic (non-biodegradable) alternative for water bottles, straws, food containers, etc.

Additionally, Nodax® PHA is the first polymer to be designated as marine degradable.

Degradation of a Danimer PHA Product

THE INVESTMENT OPPORTUNITY

According to management, the company has an opportunity to take share from the 500-billion-pound traditional plastics market.

This market is expected to continue growing at 11% annually, effectively doubling to 1 trillion pounds in 7 years.

Addressable Plastics Market

Most importantly Danimer would still be a small piece of the market even if the company can reach lofty volume goals of 190 million lbs of PHA per year by 2027, up from only 10 million lbs today.

Danimer would only be 0.02% of the global plastics market by 2027 if they hit their production targets.

The plastics market is so big, Danimer could double revenue for a decade or more and still just be scratching the surface.

The company’s current growth is in large part due to trends in consumer preferences, governmental regulations and corporate commitments to reduce plastic waste.

Speaking of corporate commitments.

PepsiCo aims to design 100% of packaging to be recyclable, compostable or biodegradable by 2025. PepsiCo also owns 6% of Danimer’s common equity.

Nestle, another Danimer partner, announced a zero net emission target by 2050.

McDonald’s, Coca-Cola, Walmart, the list goes on and on.

All this name dropping is a way to emphasize that demand from blue-chip customers has allowed for Danimer to establish a revenue model with 100% committed take-or-pay contracts and capacity that is sold out at least through 2024.

Danimer is promising rapid revenue growth, and with capacity largely sold out through 2025, the growth is largely derisked.

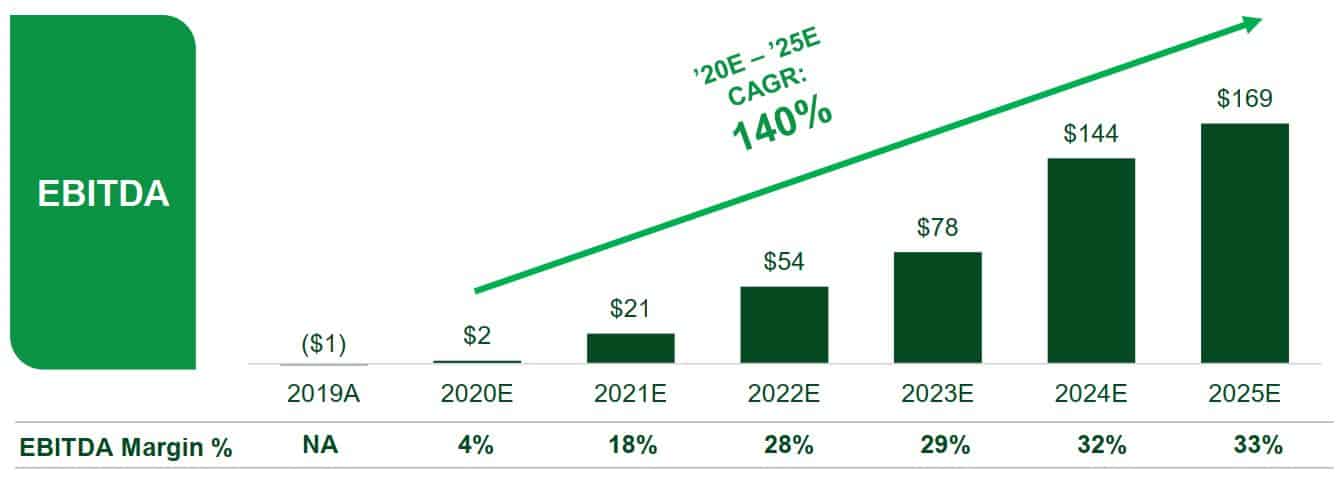

Company management also projects explosive organic growth in EBITDA as well at a ~140% CAGR from 2020E – 2025E with a projected ~685% increase in EBITDA margin to 33%.

Both revenue growth and profitability are set to see impressive increases over the medium term.

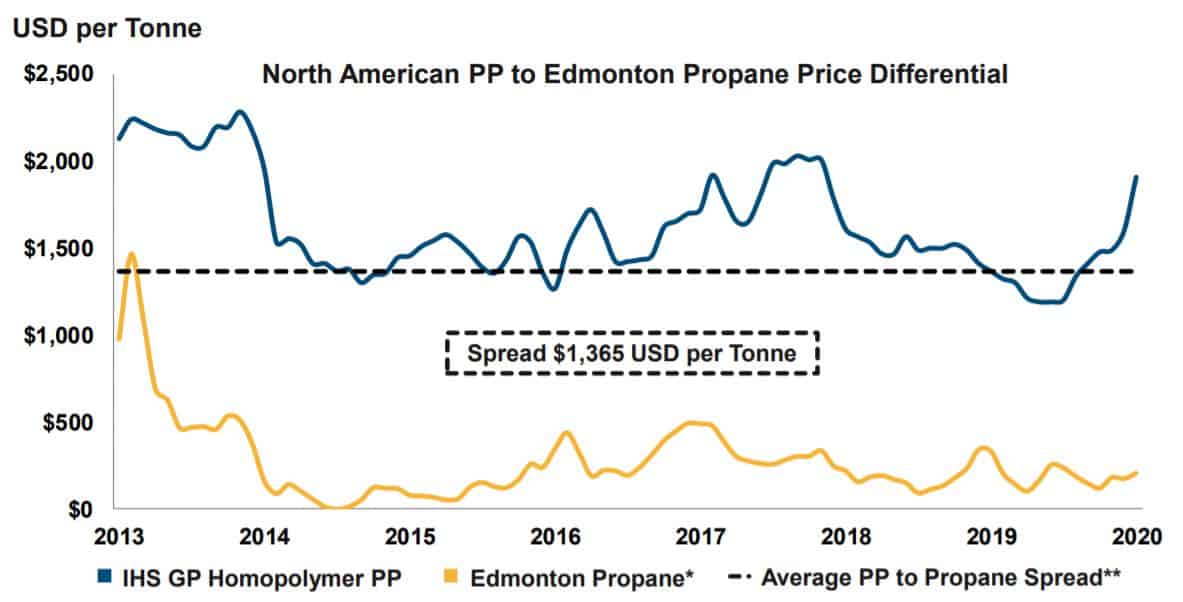

How does the Price of PHA Compare vs Traditional Plastics?

A key risk for us going into this analysis was that Danimer’s plastic is sold for twice the price of plastics made from oil.

Polypropylene, a popular plastic polymer is sold wholesale for around $1/lb according to industry producer Interpipeline and Bloomberg.

Danimer plans to sell its PHA plastic for about $2/lb over the next 5 years.

Wholesale Polypropylene (Plastic) Prices

This price mismatch doesn’t worry us for two reasons.

- Even with a more expensive product, Danimer’s capacity is sold out with customers for years to come. Demand for renewable alternatives to plastic is so great that customers are willing to pay a higher cost to cut their carbon footprint.

- Even if customers weren’t willing to pay a premium, Danimer’s higher prices are a problem that can be solved with economies of scale and R&D investments.

The company is still in the early days of commercializing its technology and we feel confident that future growth projects will have much lower production costs than current projects.

On top of economies of scale, Danimer plans to generate substantial cashflow, 30% EBITDA margins by 2024.

Danimer Expects 30% EBITDA Margins

Putting free-market competition aside, given impending government plastic bans (Canada, Europe, China), increased ESG investment and continued investments by multinational corporations into corporate, social responsibility initiatives, we believe Danimer will be able to take significant share from the pollution riddled world of hydrocarbon-based plastics even before they reach price parity.

Danimer is Years Ahead of Competitors

While Danimer claims to have the largest current PHA production capacity, other publicly traded producers do exist including Kaneka (TYO:4118), Yield 10 Bioscience (NASDAQ:YTEN) and Cardia Bioplastics (ASX:SCGRF).

However, the industry has been riddled with corporate failures lately.

Several producers have either filed for bankruptcy (Bio-on and Green Bio) or are undergoing restructurings to survive (Yield 10 Bioscience).

The industry weakness gives Danimer a leg up with the company fully funded for capacity out to 2027.

The financial weakness of peers means Danimer will have the market essentially to themselves for far longer than if competitors had money to burn.

If the company is to be believed, total PHA capacity is only 17-27KT/y and Danimer is a full 40%-60% of that capacity.

Danimer’s largest competitor, Kaneka, won’t be at commercial scale until 2025, while other competitors recently went through bankruptcy and are lacking the funds to build new capacity.

Competitors Trailing Far Behind

On top of the field being wide open, Danimer also has a solid revenue model with take-or-pay contracts, meaning customers must pay for purchased products even if they decide not to take delivery of them.

This means Danimer production is essentially sold in advance, limiting the risk that they have to cut prices to sell out inventory.

With capacity essentially sold out for the next four years we see lower than average risk that forecasts fail to materialize.

The customers behind these agreements are blue-chips such as Pepsi and Nestle which makes production and revenue targets look even more achievable.

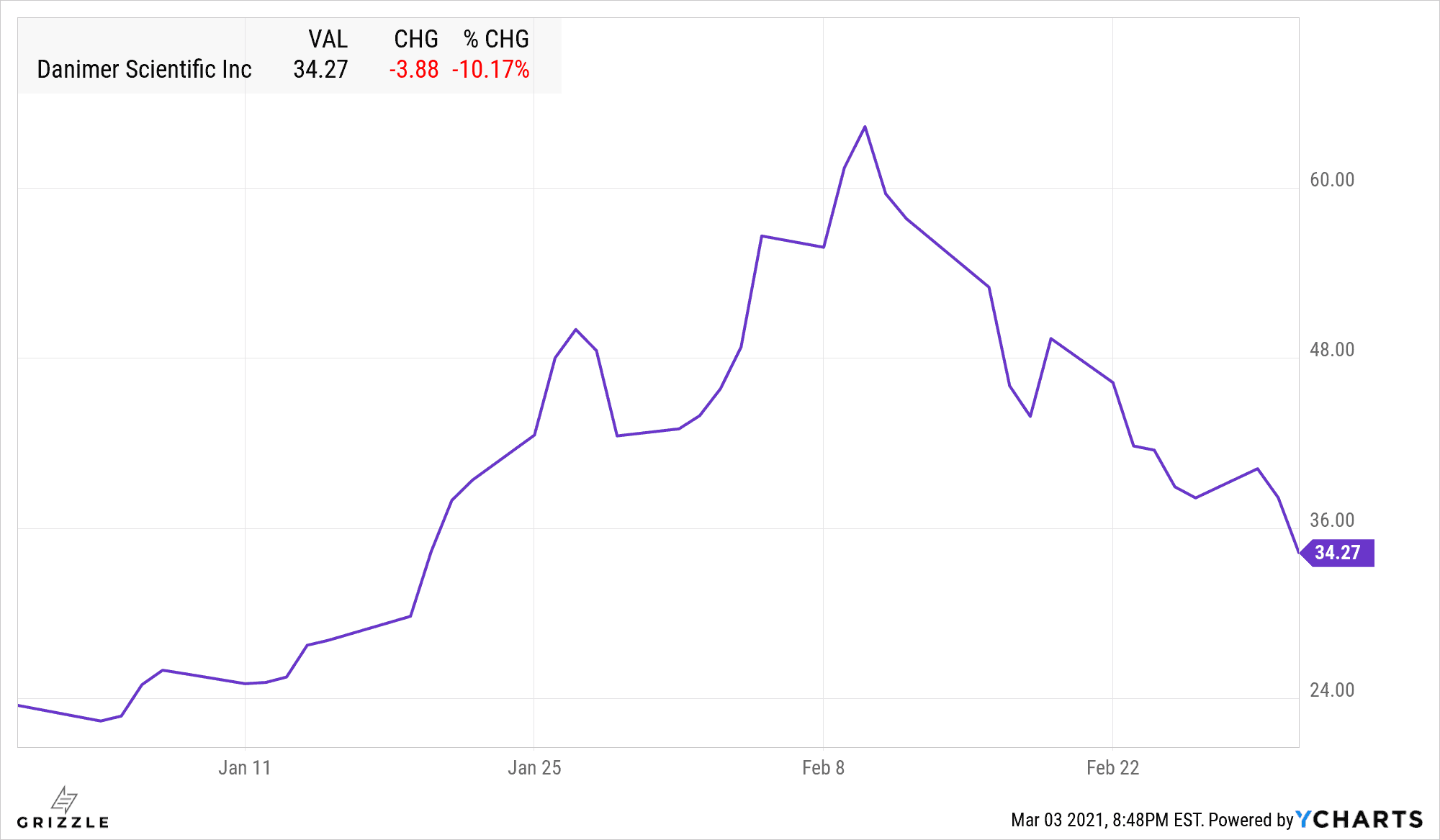

A $600 Stock, Not Impossible

Danimer began trading on the New York Stock Exchange (NYSE) on December 30, 2020 under the ticker symbol “DNMR”.

Danimer Stock Price

Since then, the stock has rallied to a high of $64.29 per share (around the first earnings call) before descending to current levels around ~34/sh.

At a $34/share price point, the company is trading at a price to sales (2021E) multiple of over 25x.

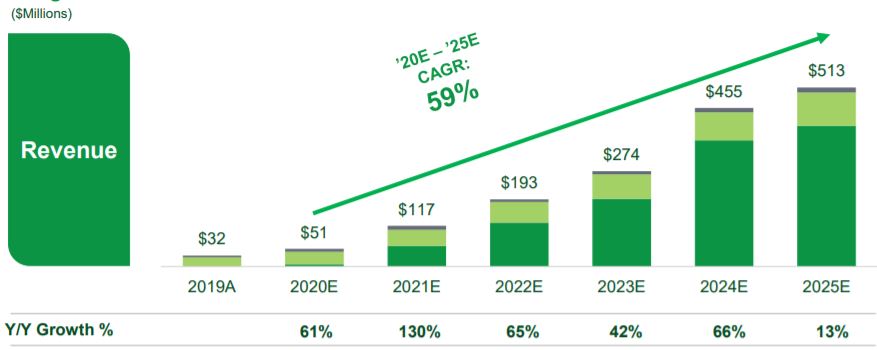

This is an expensive multiple but reflects the companies forecast for rapid growth over the next five to seven years.

Management is expecting revenues to grow at a CAGR of 59% out to 2025 which is in line with some of the best companies out there.

If Danimer achieves this growth the company would trade at a cheap 5.7x sales in 2025.

Revenue Estimate

In the software industry, there is a valuation metric called “the rule of 40” which uses the current one-year revenue growth rate plus EBITDA margin to compare high-growth companies even if they are currently losing money.

Using the Rule of 40 for Danimer, the company is way ahead of the competition. Danimer’s rule of 40 will be 134% in 2021 (130% revenue growth + 4% EBITDA margin) and 46% in 2025 once full capacity has been reached, still a solid number.

Looking at competitors, Novozymes’ Rule of 40 metric was negative in 2020, while Croda’s 2020 metric was 28.6% (7.4% organic growth and 21.2% EBITDA margin).

Kaneka’s rule of 40 is even worse at -3% in 2020 and only slightly better at 19% by 2022.

Danimer may be more expensive than these comps but this is completely justified by significantly higher growth (both revenue and EBITDA).

Danimer vs Comps (As of Reverse Merger Date)

There is an old adage in the stock market that you pay for quality and Danimer is the perfect example of this.

The multiple may look expensive today, but the company is growing so fast that it will quickly look cheap if the stock doesn’t march higher.

Not to mention the potential past 2027 to continue disrupting the massive plastics market.

Danimer is a $170 stock at a 27x sales multiple in 5 years if they simply execute their current growth plan.

But what gets us up in the morning is the long-term potential of this company.

If Danimer can capture even 5% of the global plastics market they will be pumping out a massive $52 billion of revenue.

If we apply a 2x revenue multiple to the $52 billion, assuming Danimer is now a mature company and will trade in line with peers, Danimer would be worth $600/sh up 15 times from today.

Danimer Ticks all the Boxes

From a sustainability and ESG standpoint alone, this company is a home run.

Throw in the fact that management has strong credentials, the revenue model is 100% take or pay with blue-chip customers and near-term expansion plans are fully funded, well now you have yourself a real contender.

Investors rarely get an opportunity to buy a market leader in an industry that is months away from hitting escape velocity.

Danimer is that opportunity.

The world is desperate to transition away from plastics and with few ways to do it sustainably, Danimer’s products are going to be in high demand for years to come.

Disclosure: At the time of publishing the author has a position in shares and warrants of Danimer Scientific. Employees of Grizzle may own shares in Danimer.

Full disclaimers can be found HERE

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.