To most people’s surprise, Peloton has turned into one of the best performing COVID-19 driven stocks in 2020.

Up 313% since the March market lows, outperforming even stock market darling Zoom Video.

With the company now worth over $23 billion we thought it was time to revisit the thesis and help investor’s understand the future that is baked into Peloton at $80/sh.

https://youtu.be/hN7Pc2pJkMc

The COVID-19 Effect is No Joke

Peloton had another great quarter and is benefitting mightily from the Coronavirus as demonstrated in the company’s Q4 2020 earnings results.

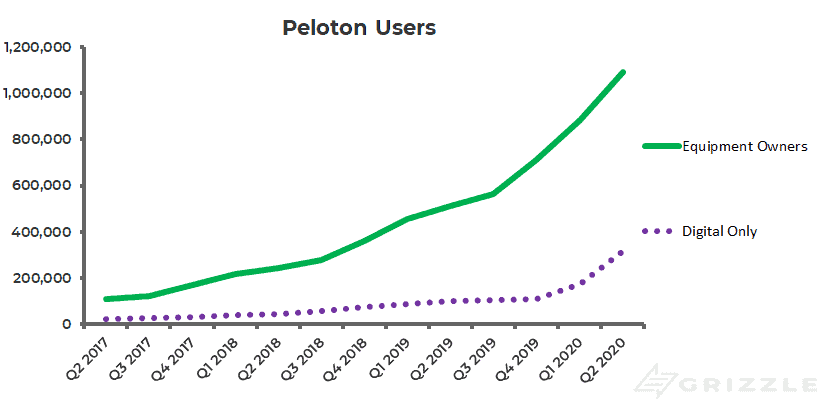

User growth has been reignited, especially with digital-only users.

6 months ago Peloton had to cut the cost of the digital subscription 50% just to keep digital users flat.

Fast forward to this quarter and digital users are up 300% year over year with no further changes in pricing.

Digital User Growth Particularly Impressive

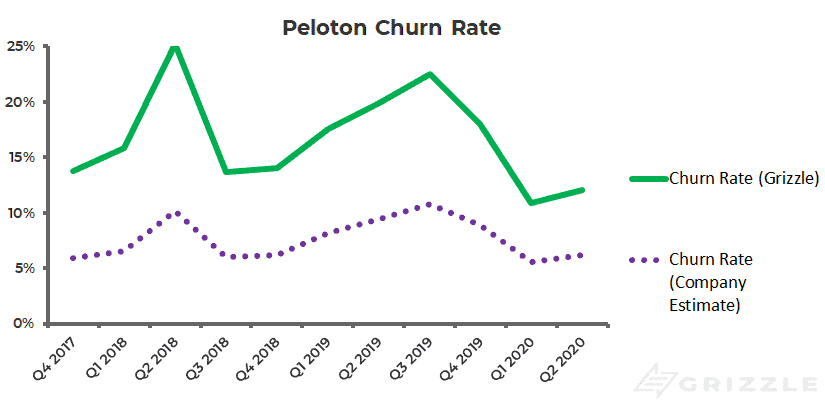

Attrition, (% of customers who quit) is back to all-time lows showing that when people are stuck inside, the last thing they want to give up is their exercise routine and the digital connection to other Peloton enthusiasts.

Peloton Quit Rate Close To All-Time Lows

The quit rate is important as it impacts the amount of money Peloton needs to spend on advertising to replace lost customers.

It also means the lifetime value of a customer goes up as they pay the monthly fee for longer.

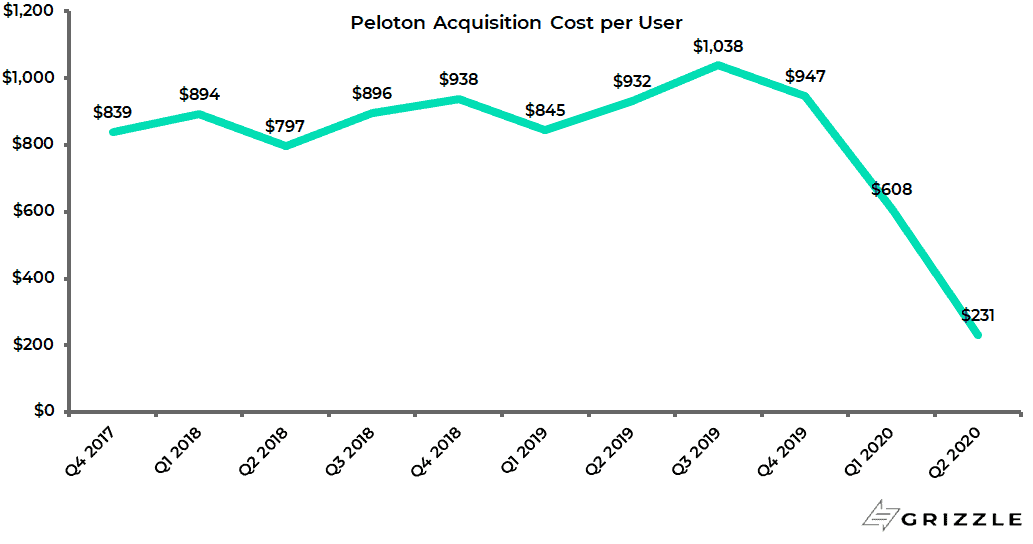

Low attrition has led to a dramatic fall in marketing costs over the last six months.

Peloton is spending only 1/4 as much as they usually do to entice a new customer.

These are massive marketing savings that are falling to the bottom line.

Peloton Marketing Costs Down Dramatically.

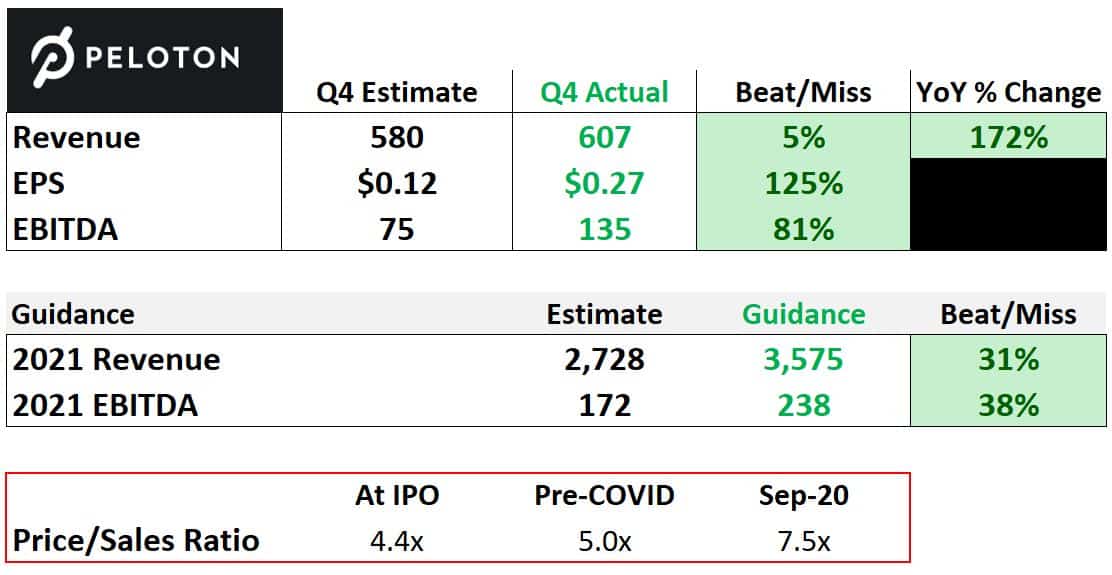

The fall in marketing costs contributed to a big earnings and EBITDA beat in the current quarter.

Peloton also increased revenue guidance for next year (fiscal 2021) by a whopping 30%.

Peloton Beat Earnings Estimates Handily for Q4 2020

Earnings Were Great, but Market Shrugged, Why?

What investors need to be asking themselves is why Peloton is down 17% after earnings even though the company crushed earnings and raised guidance by 30%.

The only explanation is that the market expected an even rosier forecast from management.

Peloton is turning into a cult stock, ala Tesla, with customers loving the equipment, the messaging and just as importantly the stock.

The most important thing investors can do before joining the cult of Peloton is to understand what future is priced into Peloton shares.

Once you know what has to go right to make you money, the upside and the downside should both be in much better focus.

Peloton, What is Priced in at $80-$90/sh

At Peloton’s recent high of $94/sh, or $26 billion, investors are willing to pay $23,000 for each customer.

The problem at this stage is the company only generates $6,600 from each customer before they stop paying for the monthly classes.

Investors are paying $23,000 and receiving only $6,600 in return, a losing investment.

Investors need to keep in mind this $6,600 is with the quit rate at an all-time low.

If the quit rate goes back up as life goes back to normal, this $6,600 number will drift lower.

The numbers above don’t necessarily mean Peloton stock is wildly, overvalued, what they are telling us is that management needs to triple the user base for the business to break even at a $94/sh stock price.

With 1 million paying members and 3 million total members, a tripling of the user base means Peloton would grow to a 9 million member company.

The big question is can the exercise market support 9 million Peloton members?

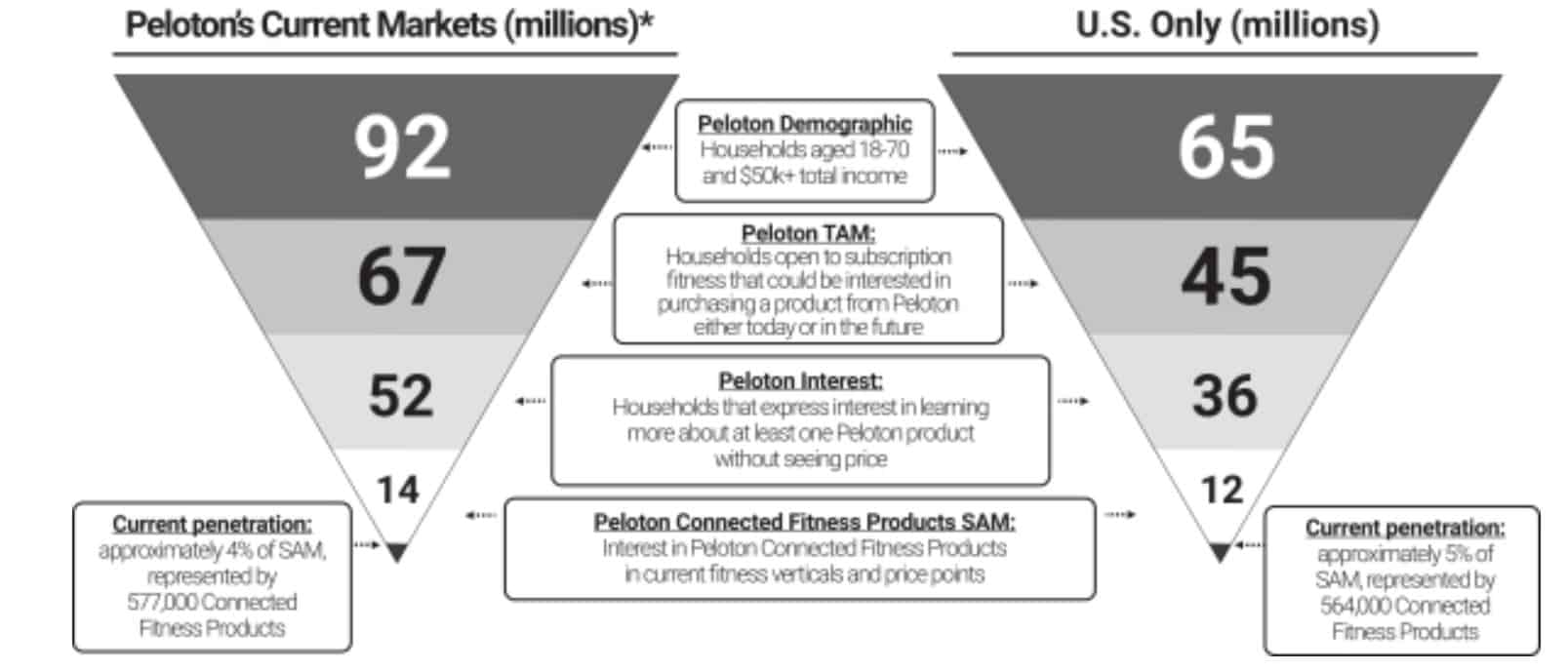

According to Peloton’s IPO filing, the immediately addressable market is 14 million members in North America and Europe.

So a tripling of the member base would mean Peloton achieves 65% penetration of the market.

A penetration rate this high means Peloton must remain the far and away market leader in connected fitness equipment.

Peloton’s Market Size Estimate is 14M Members

Let’s look at what 9 million members mean one other way.

In the context of U.S. gym memberships.

According to the International Health, Racquet and Sportsclub Association there are about 60 million Americans with a gym membership.

Now while there may be multiple people with memberships in one house, in the case of Peloton you only need one bike as the company allows multiple user profiles.

Doing some simple math:

60 million gym memberships

÷ 2.6 people per household (on average)

= 23 million potential peloton owners

So if Peloton reached 9 million members it would represent about 40% market share of all U.S. citizens with a gym membership.

It’s possible but just like our other estimate above, it requires Peloton to become an absolute juggernaut in the North American fitness equipment market.

Margin of Safety Investing This is Not

Buying an investment with a margin of safety provides you a buffer against things not going exactly as planned.

With Peloton there is no margin.

The stock is already priced for at least a doubling of the membership, which means the stock could potentially be flat for the next 12 months even if management is successful.

The company is on a roll and with the newly released Peloton Bike+ and cheaper treadmill, they have a fighting chance of reaching their goals.

Investors just need to know they are already paying for 100% success.

Anything less and they will have wished they bought the bike instead of the stock.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.